The recent Netflix series, Senna, got our friends at Hagerty thinking about movie cars that—often for practical reasons—aren’t exactly what they seem. This story originally ran on their site in 2013, and we’ve freshened it up a bit to provide some helpful and entertaining context for today’s movie-car choices.

Hollywood loves to incorporate hot classic cars into movies and television shows. Producers and insurers are also notoriously risk-averse, preferring to use replicas rather than the hyper-valuable real deal whenever possible. Here are some of our favorite big- and small-screen fakes.

Nash Bridges

1971 Plymouth Hemi ‘Cuda: The ’90s San Francisco cop show revived Don Johnson’s career, pairing him with Cheech Marin (half of the stoner comedy team of Cheech and Chong). The yellow car that appeared to be an ultra-rare Hemi ‘Cuda convertible was actually what is known as a “clone,” or a car that started out as a lesser model but was restored to appear as a top shelf ‘Cuda. The difference in price is staggering—around $180,000 usd/ $259,000 cad for a convertible with the 383, more than $3M usd/ $4.25M cad for the real deal (both prices reflect #2 condition).

Ferris Bueller’s Day Off (1985)

1960 Ferrari 250 GT California Spyder: The Ferris Bueller Ferrari is probably the best-known big screen fake and that’s why we choose it for this article’s feature image. From a distance, it appears reasonably accurate, but Ferrari aficionados can spot the differences in their sleep, from the Triumph-sourced gauges to the MGB taillights. And don’t get them talking about the bogus Italian Borrani wire wheels. A real California Spyder in #2, or Excellent, condition is nearly $20 million usd/ $28.3 million cad today.

Miami Vice (1984)

1972 Ferrari 365 GTS/4 Daytona: Don Johnson appears to be a bit of a magnet for fake cars. His black Daytona Spyder was actually a fake built on a Corvette chassis, and few Ferrari fans shed tears when the car was blown up in sight of Johnson’s character, Sonny Crockett, and his pet alligator, Elvis. Afterward, Crockett took to driving a white Ferrari Testarossa—a real one, this time.

Top Gun (1986)

1958 Porsche Speedster: Kelly McGillis’ character drove this one around San Diego in the classic ’80s movie. Porsche Speedsters are among the most replicated cars ever—most are convincing fiberglass bodies slapped on top of a VW Beetle platform.

The replica featured in Top Gun appears to have been one of the good ones, built by longtime Speedster replica-maker Intermeccanica. They’re still in business in British Columbia, Canada, turning out extremely high-quality vintage Porsche replicas.

Indiana Jones and the Temple of Doom (1984)

1935 Auburn 851 Boattail Speedster: Indy’s sidekick Short Round still holds the record for the best automotive chase involving a pre-teen driver. With blocks tied to the pedals, Short Round takes Jones and a lounge singer Willie Scott on a wild ride through prewar Shanghai. The car was, of course, a complete fake, and not a particularly convincing one at that. For the Silo, Rob Sass/Hagerty.

Did we miss any? Let us know in the comments below.

Discover the exceptional collaboration between Golden Concept, the Swiss master of ultra-luxurious Apple Watch Cases, and Blvck Paris, renowned for its ‘All Black’ luxury lifestyle apparel and accessories. Together they unveil a groundbreaking line that merges Parisian chic with Swedish sophistication, redefining the realm of high-end tech fashion. The limited-edition styles are now live and range from $899usd / $1,234cad to $1299usd / $1,783cad. The collaboration features two of Golden Concept’s top-selling pieces that have been expertly modified into exclusive black editions. This unique transformation combines the signature luxury and craftsmanship of Golden Concept with the distinct, all-black aesthetic of Blvck Paris. The pieces come in two sizes; one compatible with the Apple Watch 45 mm and the other one compatible with the Apple Watch 49 mm. These reimagined pieces perfectly represent both brands’ renowned styles, offering an unparalleled luxury experience for Apple Watch enthusiasts.

“We are super excited about this collaboration with the exquisite brand of Blvck Paris. My passion has always been in the design and creation process and to embark on this together with Julian and his team has been a real treat. We hope the customers love it as much as we do,” says Puia Shamsossadati, CEO and Creative Director of Golden Concept. “At Blvck Paris, we’re excited to team up with Golden Concept. Both brands have a deep appreciation for aesthetics and luxury, making this collaboration a natural fit. Our shared vision is to create designs that are both elegant and contemporary, offering something truly special for our customers.” – Julian O’hayon, Founder & CEO of Blvck Paris. For the Silo, Melissa Nicholls.

About Golden Concept

Golden Concept is the premier brand of luxurious tech accessories where design and style take center stage. Founded by Puia Shamsossadati in 2014, we are now celebrating a decade in the market. Our product range also includes mobile cases, accessories, and apparel with prices ranging from $1,000usd / $1,373 to $250,000usd/ $343,125cad. Golden Concept is available at over 150 premium retail locations worldwide, as well as flagship stores in Tokyo, Taipei, Singapore, Bangkok, and Shanghai, with worldwide shipping from Golden Concept. About Blvck Blvck Paris is a luxury lifestyle brand founded in 2017 by French designer Julian O’hayon. Blvck is known for its ‘All Black’ clothing, accessories, and digital goods. Blvck strives to pioneer an aspirational lifestyle from visual content to merchandise, pursuing quality and design. To date, the brand opened stores worldwide in California, Tokyo, Taipei, Taichung, Hong Kong and Macau.

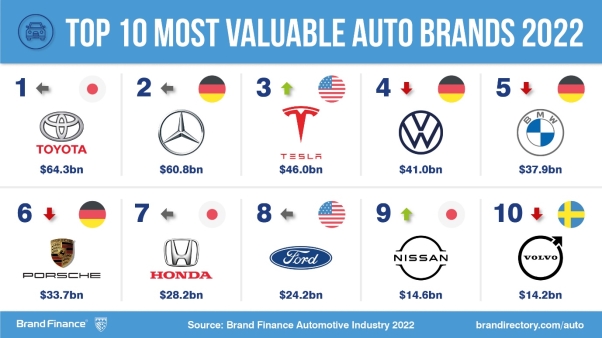

Tesla has been the fastest growing automobile brand over the course of the pandemic with astounding brand value growth of 271% in the last two years, according to the latest report by leading brand valuation consultancy Brand Finance. Tesla’s impressive growth continued this year with its brand value up by 44% to US$46.0 billion ( CAD$58.55 billion) which saw it move from 6th to 3rd in the Brand Finance Automobile 100 2022 ranking.

Tesla was the only brand in the Top 10 of the ranking to see significant growth this year.

Every year, Brand Finance puts 5,000 of the biggest brands to the test, and publishes nearly 100 reports, ranking brands across all sectors and countries. The report ranks the world’s top 100 most valuable and strongest automobile brands, the top 20 auto component brands, the top 15 tire brands and the top 10 car rental service brands.

Musk at Tesla event in China.

Tesla’s CEO, Elon Musk, has played a huge part in the growth of the brand with his charismatic, and at times controversial, behaviour keeping it firmly in the limelight. Tesla’s transformation into a household name has seen other brands try to connect themselves to the brand to benefit from the Tesla effect.

2021 saw Tesla increase its footprint in China, to ensure it continues to compete in the booming Chinese market.

It opened a new research and development centre, its first outside of America, in addition to a data centre at its Gigafactory in Shanghai. The brand also built a second delivery centre in the city, which incorporates sales, test driving and delivery of Tesla vehicles. Looking to this year 2022, Tesla announced it would launch no new models this year due to the global chip shortage, as doing so would reduce its overall output. Instead, the brand will focus on its full self-driving software as well as scaling up its production capabilities.

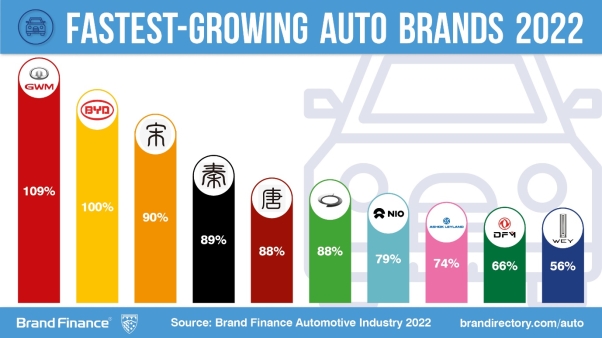

Electric revolution sees Chinese brands surge

Chinese brands account for eight of the top 10 fastest-growing brands in the ranking . The increasing popularity and adoption of electric vehicles in China has been a key driver behind the impressive growth for these brands, with China accounting for most electric vehicles sold globally. Several Chinese brands are looking to capitalise on the momentum by expanding their global footprints, with several of these brands launching in Europe in 2021.

While Tesla has seen the fastest growth over the past two years of the COVID-19 pandemic, Great Wall is the fastest-growing brand in the ranking this year, with its brand value increasing by an impressive 109% to US$2.6 billion (CAD$3.3 billion). As well as launching in Europe last year, Great Wall announced it will be launching nine electric vehicle models in Thailand over the next three years, where demand is expected to grow considerably. Great Wall plans to use Thailand as a base to launch its expansion into the ASEAN region. The auto marque’s CEO, Jianjun Wei, was also the top ranked automobile CEO in the Brand index, which ranks the world’s top 250 Chief Executives according to how well they manage and grow their company’s brand, and placed 3rd overall across all industries.

The BYD EA1 Dolphin.

BYD was the second fastest-growing brand in the automotive ranking with its brand value doubling to US$6.4 billion (CAD$8.15 billion), an increase which saw it overtake Haval (brand value up 55% to US$6.1 billion or CAD$7.76 billion) to become China’s most valuable car brand. BYD, which specialises in electric vehicles, saw sales accelerating 232% in 2021 with 603,783 models sold – making it the best-selling new energy vehicle manufacturer in China for the ninth year.

Joining Great Wall and BYD in the Top 10 fastest-growing brands is Song (brand value up 90% to US$1.7 billion or CAD$2.16 billion), Qin (up 89% to US$475 million or CAD$604 million), Tang (up 88% to US$630 million or CAD$802 million), NIO (up 79% to US$2.6 billion or CAD$3.3 billion), Dongfeng (up 67% to US$1.4 billion or CAN$1.78 billion), and WEY (up 56% to US$613 million or CAN$780 million).

Toyota holds on to pole position as most valuable automobile brand

Although Chinese auto brands have seen impressive growth, Japan’s Toyota has held on to the top spot in the Brand ranking with a brand value of US$64.3 billion (CAN$81.9 billion).

Whilst the Japanese brand wasn’t immune to the global chip shortage that ravaged the industry, Toyota was better placed than most to weather the storm thanks to its contingency stockpiling.

The foresight allowed the brand to keep production levels high when others faltered and resulted in Toyota outselling General Motors in North America in Q1 2021 – the first time any brand has outsold General Motors in the region since 1998. Toyota remains the world’s top-selling automaker, the only manufacturer selling over 10 million vehicles globally.

Toyota was one of the early adopters of hybrid technology, with its Prius model dominating the hybrid segment for years, but it has fallen behind in the increasingly competitive electric vehicle arena in recent years. To regain ground, last year it announced it would be investing US$35 billion (CAD$44.6 billion) in electric vehicles, focusing on both battery technology and car development. The investment forms part of Toyota’s ambition to sell 3.5 million electric vehicles a year by 2030.

Fellow Japanese brands Honda (brand value US$28.2 billion or CAD$35.9 billion)and Nissan (US$14.6 billion or CAD$18.6 billion) join Toyota in the Top 10 of the ranking, though both brands saw a 10% decrease in brand value this year. Honda held onto its position in 7th, and despite the loss in brand value Nissan actually climbed two spots from 11th to 9th, as it fared better than Sweden’s Volvo (down 20% to US$14.2 billion or CAD$18 billion) and Germany’s Audi (down 20% to US$13.8 billion or CAD$17.6 billion).

Mercedes-Benz remains most valuable European brand

Sitting behind Toyota, Mercedes-Benz remains the second most valuable brand in the ranking, and the most valuable European brand, with a 4% increase in brand value year-on-year to US$60.7 billion (CAD$77.3 billion). Amid challenging market conditions due to the pandemic and an industrywide semiconductor shortage, the brand prioritized electromobility and has seen great results from it. The German automobile giant confirmed that their electric vehicles sales saw a 90% increase this year.

In 2021, Mercedes-Benz launched the sixth generation of the C-class series with a new interior design and is planning to implement autonomous driving features. At the same time, an industry-wide trend to make a transition to electric vehicles and a sustainable approach to production and distribution is on the rise.

2022 Mercedes C class.

A key development to strengthen the Mercedes-Benz brand is the rebrand of Daimler AG to Mercedes-Benz Group AG. The focus of the rebrand is to enhance passenger cars and vans in the luxury segment. The strategic move to rebrand was to fulfil the brand’s objective to focus on financial and mobility services by offering insurance and rental subscriptions and digital fleet management systems.

Other German brands did not fare so well in the ranking this year, with Volkswagen (brand value down 13% to US$41.0 billion or CAD$52 billion), BMW (brand value down 6% to US$37.9 billion or CAD$48.2 billion), and Audi (brand value down 20% to US$13.8 billion or CAD$17.6 billion) all seeing losses in brand value. With lockdowns, network contractions in production and the ongoing semiconductor shortage, the industry has been faced with many challenges. Apart from sector wide disruptions, the German automakers who were reliant on diesel-powered vehicles have had to deal with regulatory challenges and the transition to electric mobility and electric production methods, resulting in rolling back on production to meet industry trends.

Porsche most valuable among luxury and premium, but Ferrari strongest across the whole table

Porsche is the most valuable luxury and premium automobile brand in the world with a brand value of US$33.7 billion (CAD$42.9 billion). The automobile giant celebrated the 50th anniversary of the iconic Porsche Design with a limited-edition sale of 750 cars to pay tribute to the iconic design by Ferdinand Alexander Porsche.

The brand’s aim to transform into an agile company has led to leveraging digital transformation by enhancing online sales. To adapt to new formats of sale in the automobile sector, Porsche has invested in e-commerce for 100 markets globally to adopt an omnichannel strategy to connect digital services and retail sales.

While Porsche is the most valuable brand in the luxury and premium segment, Ferrari was named the strongest automobile brand in the world with a Brand Strength Index (BSI) score of 90.9 out of 100 and a corresponding AAA+ rating. Apart from calculating brand value, Brand Finance also determines the relative strength of brands through a balanced scorecard of metrics evaluating marketing investment, stakeholder equity, and business performance. Certified by ISO 20671, Brand Finance’s assessment of stakeholder equity incorporates original market research data from over 100,000 respondents in more than 35 countries and across nearly 30 sectors.

2021 was Ferrari’s best-ever year in terms of sales, with the company paying bonuses to all employees as a result, and the projected growth for 2022 remains high. The automotive brand’s historic pursuit of controlled growth has helped to preserve its exclusivity within its sector, however, last year Ferrari expanded its target market to a younger demographic by launching a new high-end fashion line. The aim of creating a brand that can cater to Italian luxury lifestyle in the high-end category will help expand and strengthen its brand portfolio into new avenues, whilst enhancing brand awareness amongst the younger generation.

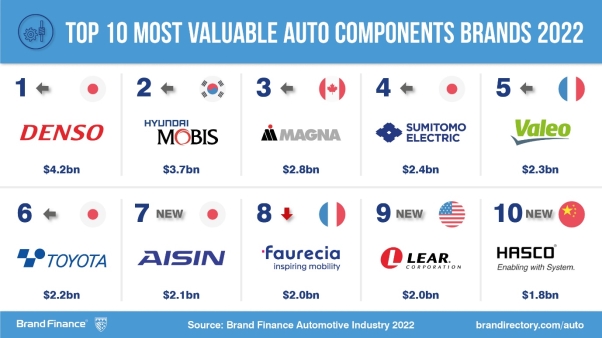

Denso most valuable auto components brand

Car sales picked up following the loosening of lockdown restrictions, and auto component brands saw demand rise in turn. It has been far from clear sailing for the industry with the global chip shortage disrupting production, but the overall outlook is positive, evidenced by the vast majority of brands seeing good growth.

Denso has retained the title of most valuable auto components brand in the world for the 5th consecutive year, with brand value up 12% to US$4.2 billion (CAD$5.4 billion). The brand continued to play its part in combatting the COVID-19 pandemic, creating respirator components in collaboration with Ford, as well as hosting over 50 vaccination clinics for employees across North America. Looking forward, the ever-increasing adoption of hybrid and electric vehicles is good news for Denso, which has over two decades worth of experience in the manufacturing of hybrid car parts.

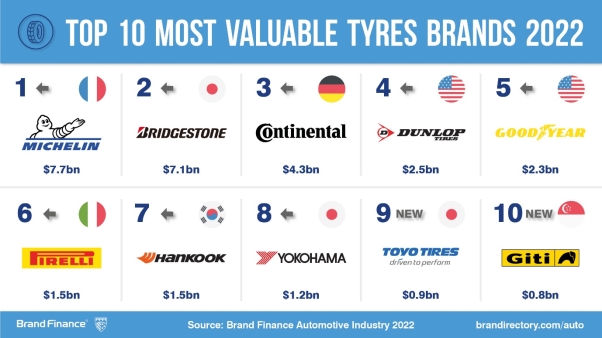

Michelin most valuable and strongest tyres brand

As the world opened back up and travel increased throughout 2021 the tyre sector regained traction, with almost every brand in the ranking now more valuable than they were pre-pandemic.

Michelin has retained the title of the world’s most valuable and strongest tires brand, with a brand value of US$7.7 billion (CAD$9.8 billion) and a brand strength index score of 85.8 out of 100.

Despite continued disruption within the industry, Michelin saw a 15.6% year-on-year increase in consolidated sales in the first nine months of 2021 and exceeded expectations in the third quarter of the year thanks to a rebound in demand for tires for agricultural machinery. The brand also announced an extension of its partnership with the MotoGP World Championship, remaining the exclusive tire supplier for the competition until 2026.

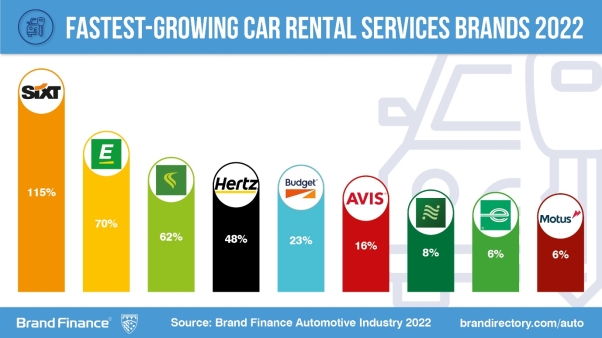

SIXT is fastest-growing car rental services brand

The car rental brands have gained momentum in 2021 after a steep decline in brand value at the start of the pandemic. As the demand for vehicle hires increases, brands in this industry are presented with the opportunity to innovate and capture a high market share.

SIXT is the world’s fastest-growing car rental brand of 2022 with a 115% increase in brand value over the year to US$1.3 billion (CAN$1.7 billion), according to the Brand Finance ranking. This year’s increase is the continuation of an impressive growth trend for SIXT, which has seen its brand value increase 265% over the past five years. The brand has built a strong international growth strategy, expanding rapidly in the United States and entering new markets, such as Australia.

Enterprise has retained the position of the world’s most valuable car rental brand with a brand value of US$7.1 billion (CAN$9 billion) with a 6% increase in brand value over the year. Despite COVID-induced travel restrictions, the brand has performed well by launching new mobility hubs and undertaking fleet electrification, but it remains below its pre-pandemic brand value of US$7.4 billion (CAD$9.4 billion). For the Silo, James Haggis.

Featured image: Great Wall Ora Concept Electric Car Made In China

2018 Weed Index Study reveals the cost of marijuana and highlights the number of grow and head shops in 120 cities around the world:

With a total of 156, Los Angeles, USA has the most headshops.

Madrid, Spain has the largest amount of growshops, with a total of 68.

Tokyo, Japan has the most expensive cannabis, at 32.66 USD per gram, while Quito, Ecuador has the least expensive marijuana, at 1.34 USD per gram.

Based on the average US marijuana tax rates currently implemented, New York City could generate the highest potential tax revenue by legalising weed, with 156.40 million USD per year. New York City also has the highest consumption rate of cannabis, at 77.44 metric tons per year.

Berlin, Germany, 20/04/2018 – ABCD, a data-driven media campaign outlet, has released new data which reveals the number of marijuana head and growshops in 120 cities around the world. This research, which builds on the 2018 Cannabis Price Index released earlier this year, reveals which locations around the world are ready to embrace cannabis legalisation. The aim of the study is to illustrate the continuous need for legislative reform on cannabis use around the world, and to determine if there are any lessons to be learned from those cities at the forefront of marijuana legalization. By including extra data on the number of head and growshops in each city, this new research can be utilized to indicate which cities are prepared for an imminent cannabis reform, while also highlighting which cities are in opposition of marijuana legalisation.

The initial study began by selecting 120 cities across the world, including locations where cannabis is currently legal, illegal and partially legal, and where marijuana consumption data is available. Then, they looked into the price of weed per gram in each city. To calculate how much potential tax a city could make by legalising weed, ABCD investigated how much tax is paid on the most popular brand of cigarettes, as this offers the closest comparison. They then looked at what percentage marijuana is currently taxed in cities where it’s already legalised in the US.

ABCD decided to conduct the extra research in order to to further the discussion around the medical and recreational use of cannabis, and the potential industry and business opportunities that would follow legalisation. By identifying the number of headshops as well as growshops, this study serves as an indicator to a city’s existing cannabis infrastructure and willingness to accept such reform on a larger scale. As an indicating factor, the more head shops and grow shops a city has, the more positive their state’s and general public’s attitude towards the cannabis-related industry is likely to be.

The table below reveals a sample of the results for the 13 US cities featured in the study:

#

City

Legality

Price per gram, US$

Total possible tax collection, if taxed at cigarette level, mil US$

Total possible tax collection, if taxed at average US marijuana taxes, mil US$

Total consumption in metric tons

Headshops

Growshops

1

Washington, DC

Partial

18.08

47.51

20.96

6.18

20

8

2

Chicago

Partial

11.46

119.61

52.77

24.54

91

10

3

Philadelphia

Partial

11.30

68.37

30.16

14.22

41

3

4

Boston

Legal

11.01

28.59

12.61

6.10

49

4

5

New York

Partial

10.76

354.48

156.40

77.44

59

7

6

Dallas

Partial

10.03

51.01

22.5

11.95

80

6

7

Houston

Partial

10.03

89.13

39.32

20.89

125

14

8

Phoenix

Partial

9.35

58.26

25.71

14.65

72

9

9

Miami

Partial

9.27

16.24

7.16

4.12

67

25

10

San Francisco

Legal

9.27

30.94

13.65

7.85

61

3

11

Los Angeles

Legal

8.14

124.88

55.10

36.06

153

46

12

Denver

Legal

7.79

20.53

9.06

6.20

61

21

13

Seattle

Legal

7.58

20.59

9.08

6.39

46

10

The table below shows the top 10 most and least expensive cities for cannabis:

Top 10 Most Expensive Cities

Top 10 Least Expensive Cities

#

City

Country

Legality

Price per gram, US$

#

City

Country

Legality

Price per gram, US$

1

Tokyo

Japan

Illegal

32.66

1

Quito

Ecuador

Partial

1.34

2

Seoul

South Korea

Illegal

32.44

2

Bogota

Colombia

Partial

2.20

3

Kyoto

Japan

Illegal

29.65

3

Asuncion

Paraguay

Partial

2.22

4

Hong Kong

China

Illegal

27.48

4

Jakarta

Indonesia

Illegal

3.79

5

Bangkok

Thailand

Partial

24.81

5

Panama City

Panama

Illegal

3.85

6

Dublin

Ireland

Illegal

21.63

6

Johannesburg

South Africa

Illegal

4.01

7

Tallinn

Estonia

Partial

20.98

7

Montevideo

Uruguay

Legal

4.15

8

Shanghai

China

Illegal

20.82

8

Astana

Kazakhstan

Illegal

4.22

9

Beijing

China

Illegal

20.52

9

Antwerp

Belgium

Partial

4.29

10

Oslo

Norway

Partial

19.14

10

New Delhi

India

Partial

4.38

The table Below shows the top 10 cities with the most growshops:

#

City

Country

Legality

Growshops

1

Madrid

Spain

Partial

68

2

Buenos Aires

Argentina

Partial

48

3

Los Angeles

USA

Legal

46

4

Toronto

Canada

Partial

37

5

Melbourne

Australia

Partial

31

6

Miami

USA

Partial

25

7

London

UK

Illegal

23

8

Barcelona

Spain

Partial

23

9

Denver

USA

Legal

21

10

Berlin

Germany

Partial

20

The table Below shows the top 10 cities with the most headshops:

#

City

Country

Legality

Headshops

1

Los Angeles

USA

Legal

156

2

Houston

USA

Partial

125

3

Chicago

USA

Partial

91

4

Dallas

USA

Partial

80

5

Phoenix

USA

Partial

72

6

Miami

USA

Partial

67

7

San Francisco

USA

Legal

61

8

Denver

USA

Legal

61

9

New York

USA

Partial

59

10

Boston

USA

Legal

49

The table below shows the top 10 cities who could generate the most potential tax by legalising cannabis, if taxed at the same rate as the most popular cigarette brand:

#

City

Country

Legality

Price per gram, US$

% of cigarette tax

Possible tax revenue, mil US$

1

Cairo

Egypt

Illegal

16.15

73.13

384.87

2

New York

USA

Partial

10.76

42.54

354.48

3

London

UK

Illegal

9.20

82.16

237.35

4

Sydney

Australia

Partial

10.79

56.76

138.36

5

Karachi

Pakistan

Illegal

5.32

60.7

135.48

6

Melbourne

Australia

Partial

10.84

56.76

132.75

7

Moscow

Russia

Partial

11.84

47.63

128.97

8

Toronto

Canada

Partial

7.82

69.8

124.15

9

Chicago

USA

Partial

11.46

42.54

119.61

10

Berlin

Germany

Partial

13.53

72.9

114.77

N.B. % of cigarette tax refers to the tax percentage on the most popular brand. Possible tax revenue refers to the total possible tax collection per year, if taxed at cigarette level. For a full explanation of how the study was conducted, please see the methodology at the bottom of the press release.

The table below shows the top 10 cities who could generate the most potential tax by legalising cannabis, if taxed at the average US marijuana tax rate:

#

City

Country

Legality

Price per gram, US$

Possible tax revenue, mil US$

1

New York

USA

Partial

10.76

156.4

2

Cairo

Egypt

Illegal

16.15

98.78

3

London

UK

Illegal

9.20

54.22

4

Chicago

USA

Partial

11.46

52.77

5

Moscow

Russia

Partial

11.84

50.82

6

Sydney

Australia

Partial

10.79

45.75

7

Melbourne

Australia

Partial

10.84

43.9

8

Karachi

Pakistan

Illegal

5.32

41.89

9

Houston

USA

Partial

10.03

39.32

10

Toronto

Canada

Partial

7.82

33.38

N.B. Possible tax revenue refers to the total possible tax collection per year, if taxed at average US marijuana tax rate.

The table below shows the top 10 cities with the highest and lowest consumption of cannabis, per year:

Highest Consumers of Cannabis

Lowest Consumers of Cannabis

#

City

Country

Legality

Price per gram, US$

Total consumption, metric tons

#

City

Country

Legality

Price per gram, US$

Total consumption, metric tons

1

New York

USA

Partial

10.76

77.44

1

Singapore

Singapore

Illegal

14.01

0.02

2

Karachi

Pakistan

Illegal

5.32

41.95

2

Santo Domingo

Dominican Rep.

Illegal

6.93

0.16

3

New Delhi

India

Partial

4.38

38.26

3

Kyoto

Japan

Illegal

29.65

0.24

4

Los Angeles

USA

Legal

8.14

36.06

4

Thessaloniki

Greece

Partial

13.49

0.29

5

Cairo

Egypt

Illegal

16.15

32.59

5

Luxembourg City

Luxembourg

Partial

7.26

0.32

6

Mumbai

India

Partial

4.57

32.38

6

Panama City

Panama

Illegal

3.85

0.37

7

London

UK

Illegal

9.20

31.4

7

Reykjavik

Iceland

Illegal

15.92

0.44

8

Chicago

USA

Partial

11.46

24.54

8

Asuncion

Paraguay

Partial

2.22

0.46

9

Moscow

Russia

Partial

11.84

22.87

9

Colombo

Sri Lanka

Illegal

9.12

0.59

10

Toronto

Canada

Partial

7.82

22.75

10

Manila

Philippines

Illegal

5.24

0.6

N.B. Total consumption is calculated per annum.

Further findings:

Shanghai, China has a large population of 24.15 million, has however no headshops or growshops in the city, underlining a resistance against cannabis reform.

On average, the status of legality (e.g. Legal, Partial or Illegal) coincides with the amount of headshops and growshops found in each city. The favourable the laws, the better the cannabis infrastructure

New York City, USA has the highest consumption rate of cannabis, at 77.44 metric tons per year.

Boston, USA has the most expensive cannabis of all the cities where it’s legal, at 11.01 USD, while Montevideo, Uruguay has the least expensive at 4.15 USD.

While Tokyo, Japan has the most expensive cannabis of all cities where it’s illegal, at 32.66 USD, Jakarta, Indonesia has the least expensive at 3.79 USD, despite being classed as a Group 1 drug with harsh sentences such as life imprisonment and the death penalty.

For cities where cannabis is partially legal, Bangkok, Thailand has the most expensive at 24.81 USD, while Quito, Ecuador has the least expensive at 1.34 USD.

Bulgaria has the highest tax rates for the most popular brand of cigarettes, at 82.65%, while Paraguay has the lowest, with rates of 16%.

Cairo, Egypt would gain the most revenue in tax if they were to legalise cannabis and tax it as the same rate as cigarettes, at 384.87 million USD. Singapore, Singapore would gain the least, at 0.14 million USD, due in part to the city’s low consumption of marijuana at 0.02 metric tons per annum.

Based on the average US marijuana tax rates currently implemented, New York City could generate the highest potential tax revenue by legalising weed, with 156.4 million USD per year. Singapore, Singapore would gain the least, at 0.04 million USD.

The full results of the 2018 Cannabis Price Index:

#

City

Country

Legality

Price per gram, US$

Taxes of cigarettes, % of the most sold brand

Total possible tax collection, if taxed at cigarette level, mil US$

Total possible tax collection, if taxed at average US marijuana taxes, mil US$

Total Consumption in metric tons

1

Tokyo

Japan

Illegal

32.66

64.36

32.14

9.37

1.53

2

Seoul

South Korea

Illegal

32.44

61.99

31.61

9.57

1.57

3

Kyoto

Japan

Illegal

29.65

64.36

4.64

1.35

0.24

4

Hong Kong

China

Illegal

27.48

44.43

19.72

8.33

1.62

5

Bangkok

Thailand

Partial

24.81

73.13

99.11

25.44

5.46

6

Dublin

Ireland

Illegal

21.63

77.80

29.31

7.07

1.74

7

Tallinn

Estonia

Partial

20.98

77.24

22.13

5.38

1.37

8

Shanghai

China

Illegal

20.82

44.43

49.12

20.75

5.31

9

Beijing

China

Illegal

20.52

44.43

43.10

18.21

4.73

10

Oslo

Norway

Partial

19.14

68.83

19.28

5.26

1.46

11

Washington, DC

USA

Partial

18.08

42.54

47.51

20.96

6.18

12

Cairo

Egypt

Illegal

16.15

73.13

384.87

98.78

32.59

13

Reykjavik

Iceland

Illegal

15.92

56.40

3.97

1.32

0.44

14

Belfast

Ireland

Illegal

15.81

77.80

13.55

3.27

1.10

15

Minsk

Belarus

Illegal

15.80

51.15

9.08

3.33

1.12

16

Athens

Greece

Partial

14.95

79.95

7.42

1.74

0.62

17

Auckland

New Zealand

Partial

14.77

77.34

106.03

25.73

9.28

18

Munich

Germany

Partial

14.56

72.90

50.90

13.10

4.80

19

Helsinki

Finland

Partial

14.42

81.53

27.12

6.24

2.31

20

Singapore

Singapore

Illegal

14.01

66.23

0.14

0.04

0.02

21

Berlin

Germany

Partial

13.53

72.90

114.77

29.55

11.64

22

Stuttgart

Germany

Partial

13.50

72.90

20.20

5.20

2.05

23

Thessaloniki

Greece

Partial

13.49

79.95

3.17

0.75

0.29

24

Stockholm

Sweden

Illegal

13.20

68.84

15.06

4.11

1.66

25

Vienna

Austria

Partial

12.87

74.00

59.21

15.02

6.22

26

Copenhagen

Denmark

Partial

12.47

74.75

20.65

5.18

2.22

27

Moscow

Russia

Partial

11.84

47.63

128.97

50.82

22.87

28

Hamburg

Germany

Partial

11.64

72.90

50.16

12.92

5.91

29

Chicago

USA

Partial

11.46

42.54

119.61

52.77

24.54

30

Philadelphia

USA

Partial

11.30

42.54

68.37

30.16

14.22

31

Bucharest

Romania

Partial

11.18

75.41

17.23

4.29

2.04

32

Cologne

Germany

Partial

11.14

72.90

28.51

7.34

3.51

33

Geneva

Switzerland

Partial

11.12

61.20

5.90

1.81

0.87

34

Boston

USA

Legal

11.01

42.54

28.59

12.61

6.10

35

Adelaide

Australia

Partial

10.91

56.76

41.60

13.75

6.72

36

Istanbul

Turkey

Partial

10.87

82.13

21.79

4.98

2.44

37

Melbourne

Australia

Partial

10.84

56.76

132.75

43.90

21.58

38

Sydney

Australia

Partial

10.79

56.76

138.36

45.75

22.59

39

New York

USA

Partial

10.76

42.54

354.48

156.40

77.44

40

Düsseldorf

Germany

Partial

10.70

72.90

15.82

4.07

2.03

41

Brisbane

Australia

Partial

10.63

56.76

66.88

22.12

11.09

42

Hanover

Germany

Partial

10.51

72.90

13.46

3.47

1.76

43

Prague

Czech Rep.

Partial

10.47

77.42

63.95

15.50

7.89

44

Frankfurt

Germany

Partial

10.29

72.90

18.06

4.65

2.41

45

Wellington

New Zealand

Partial

10.11

77.34

19.53

4.74

2.50

46

Dallas

USA

Partial

10.03

42.54

51.01

22.50

11.95

47

Houston

USA

Partial

10.03

42.54

89.13

39.32

20.89

48

Vilnius

Lithuania

Illegal

10.00

75.76

5.20

1.29

0.69

49

Zurich

Switzerland

Partial

9.71

61.20

10.33

3.17

1.74

50

Montpellier

France

Illegal

9.70

80.30

12.21

2.85

1.57

51

Canberra

Australia

Partial

9.65

56.76

10.96

3.63

2.00

52

Zagreb

Croatia

Partial

9.43

75.26

24.35

6.07

3.43

53

Nice

France

Illegal

9.40

80.30

15.80

3.69

2.09

54

Phoenix

USA

Partial

9.35

42.54

58.26

25.71

14.65

55

Paris

France

Illegal

9.30

80.30

102.25

23.90

13.69

56

Miami

USA

Partial

9.27

42.54

16.24

7.16

4.12

57

San Francisco

USA

Legal

9.27

42.54

30.94

13.65

7.85

58

London

UK

Illegal

9.20

82.16

237.35

54.22

31.40

59

Colombo

Sri Lanka

Illegal

9.12

73.78

3.98

1.01

0.59

60

Riga

Latvia

Illegal

9.00

76.89

10.23

2.50

1.48

61

Bratislava

Slovakia

Illegal

8.92

81.54

7.24

1.67

1.00

62

Milan

Italy

Partial

8.85

75.68

46.06

11.42

6.88

63

Varna

Bulgaria

Illegal

8.83

82.65

4.84

1.10

0.66

64

Marseille

France

Illegal

8.69

80.30

36.23

8.47

5.19

65

Glasgow

UK

Illegal

8.65

82.16

15.21

3.47

2.14

66

Toulouse

France

Illegal

8.62

80.30

18.67

4.36

2.70

67

Birmingham

UK

Illegal

8.58

82.16

27.73

6.34

3.93

68

Kuala Lumpur

Malaysia

Illegal

8.54

55.36

6.61

2.24

1.40

69

Monterrey

Mexico

Partial

8.45

65.87

4.17

1.19

0.75

70

Edinburgh

UK

Illegal

8.41

82.16

12.22

2.79

1.77

71

Lisbon

Portugal

Partial

8.36

74.51

4.69

1.18

0.75

72

Strasbourg

France

Illegal

8.35

80.30

11.13

2.60

1.66

73

Warsaw

Poland

Partial

8.31

80.29

29.27

6.84

4.39

74

Lyon

France

Illegal

8.20

80.30

19.45

4.55

2.95

75

Los Angeles

USA

Legal

8.14

42.54

124.88

55.10

36.06

76

Liverpool

UK

Illegal

7.94

82.16

10.86

2.48

1.67

77

Amsterdam

Netherlands

Partial

7.89

73.40

20.94

5.35

3.61

78

Manchester

UK

Illegal

7.88

82.16

58.99

13.48

9.11

79

Rome

Italy

Partial

7.86

75.68

88.16

21.86

14.82

80

Toronto

Canada

Partial

7.82

69.80

124.15

33.38

22.75

81

Denver

USA

Legal

7.79

42.54

20.53

9.06

6.20

82

Naples

Italy

Partial

7.75

75.68

29.82

7.40

5.08

83

Leeds

UK

Illegal

7.67

82.16

16.93

3.87

2.69

84

Seattle

USA

Legal

7.58

42.54

20.59

9.08

6.39

85

Madrid

Spain

Partial

7.47

78.09

93.40

22.45

16.01

86

Calgary

Canada

Partial

7.30

69.80

52.23

14.05

10.25

87

Luxembourg City

Luxembourg

Partial

7.26

70.24

1.62

0.43

0.32

88

San Jose

Costa Rica

Partial

7.23

69.76

7.84

2.11

1.56

89

Buenos Aires

Argentina

Partial

7.13

69.84

25.32

6.81

5.09

90

Brussels

Belgium

Partial

7.09

75.92

15.50

3.83

2.88

91

Santo Domingo

Dominican Rep.

Illegal

6.93

58.87

0.67

0.21

0.16

92

Graz

Austria

Partial

6.84

74.00

4.81

1.22

0.95

93

Budapest

Hungary

Illegal

6.74

77.26

7.70

1.87

1.48

94

Sofia

Bulgaria

Illegal

6.66

82.65

12.83

2.91

2.33

95

Ottawa

Canada

Partial

6.62

69.80

35.43

9.53

7.67

96

Vancouver

Canada

Partial

6.40

69.80

23.44

6.30

5.25

97

Sao Paulo

Brazil

Partial

6.38

64.94

68.55

19.81

16.55

98

Rotterdam

Netherlands

Partial

6.33

73.40

12.75

3.26

2.74

99

Ljubljana

Slovenia

Partial

6.32

80.41

3.43

0.80

0.67

100

Barcelona

Spain

Partial

6.23

78.09

39.59

9.51

8.14

101

Montreal

Canada

Partial

6.15

69.80

60.52

16.27

14.10

102

Kiev

Ukraine

Partial

6.00

74.78

14.73

3.70

3.28

103

Abuja

Nigeria

Illegal

5.88

20.63

7.40

6.73

6.10

104

Lima

Peru

Partial

5.88

37.83

12.28

6.09

5.52

105

Mexico City

Mexico

Partial

5.87

65.87

22.58

6.43

5.84

106

Cape Town

South Africa

Illegal

5.82

48.80

2.47

0.95

0.87

107

Karachi

Pakistan

Illegal

5.32

60.70

135.48

41.89

41.95

108

Manila

Philippines

Illegal

5.24

74.27

2.32

0.59

0.60

109

Rio de Janeiro

Brazil

Partial

5.11

64.94

28.82

8.33

8.69

110

Mumbai

India

Partial

4.57

60.39

89.38

27.78

32.38

111

New Delhi

India

Partial

4.38

60.39

101.20

31.45

38.26

112

Antwerp

Belgium

Partial

4.29

75.92

4.10

1.01

1.26

113

Astana

Kazakhstan

Illegal

4.22

39.29

1.78

0.85

1.07

114

Montevideo

Uruguay

Legal

4.15

66.75

19.54

5.50

7.06

115

Johannesburg

South Africa

Illegal

4.01

48.80

3.76

1.45

1.92

116

Panama City

Panama

Illegal

3.85

56.52

0.81

0.27

0.37

117

Jakarta

Indonesia

Illegal

3.79

53.40

1.92

0.68

0.95

118

Asuncion

Paraguay

Partial

2.22

16.00

0.16

0.19

0.46

119

Bogota

Colombia

Partial

2.20

49.44

15.80

6.00

14.53

120

Quito

Ecuador

Partial

1.34

70.39

0.56

0.15

0.60

Methodology

Selection of the cities:

To select the cities for the study, Seedo first looked at the top and bottom cannabis consuming countries around the world. Then they analysed nations where marijuana is partially or completely legal, as well as illegal, and selected the final list of 120 cities in order to best offer a representative comparison of the global cannabis price.

Data:

Price per gram, US$ – Crowdsourced city-level surveys adjusted to World Drug Report 2017 of the United Nations Office on Drugs and Crime.

Taxes on Cigarettes, % of the most sold brand – Taxes as a percentage of the retail price of the most sold brand (total tax). Source: Appendix 2 of the WHO report on the global tobacco epidemic, 2015.

Annual possible tax collection is calculated in the following way:

Population: latest available local population data sources.

Annual Prevalence (percentage of population, having used weed in the year). Source: World Drug Report 2017 of the United Nations Office on Drugs and Crime

Average Consumption of weed per year in grams (people who consumed weed at least once in the previous year).

Estimation, with the assumption, that one use of weed on average means one joint.

One joint is assumed to have 0.66 grams of weed as in the paper of Mariani, Brooks, Haney and Levin (2010).

The distribution of use during the year is assumed to be the same as in Zhao and Harris (2004), where the yearly usage varies from once or twice a year to everyday.

Population: latest available local population data sources.

Annual Prevalence (percentage of population, having used weed in the year). Source: World Drug Report 2017 of the United Nations Office on Drugs and Crime

Average Consumption of weed per year in grams (people who consumed weed at least once in the previous year).

Estimation, with the assumption, that one use of weed on average means one joint.

One joint is assumed to have 0.66 grams of weed as in the paper of Mariani, Brooks, Haney and Levin (2010).

The distribution of use during the year is assumed to be the same as in Zhao and Harris (2004), where the yearly usage varies from once or twice a year to everyday.

US tax level – Average tax level in the states of US where weed is legal: Alaska, California, Colorado, Maine, Massachusetts, Nevada, Oregon and Washington. Includes retail sales taxes, state taxes, local taxes and excise taxes.

Growshops – Sourced via Google Maps Listings 2018

Headshops – Sourced via Google Maps Data Listings 2018

Legality

Legal, if possession and selling for recreational and medical use is legal.

Illegal, if possession and selling for recreational and medical use is illegal.

Partial, if

Possession of small amounts is decriminalised (criminal penalties lessened, fines and regulated permits may still apply)

OR medicinal use legal

OR possession is legal, selling illegal

OR scientific use legal

OR usage allowed in restricted areas (e.g. homes or coffee shops)

OR local laws may apply to legality (e.g. illegal at federal level, legal at state level)

First quote: Based on New York City Council’s free lunch initiative which began in September 2017, with 1.1 million public school children, at a cost of $1.75 per child per day.

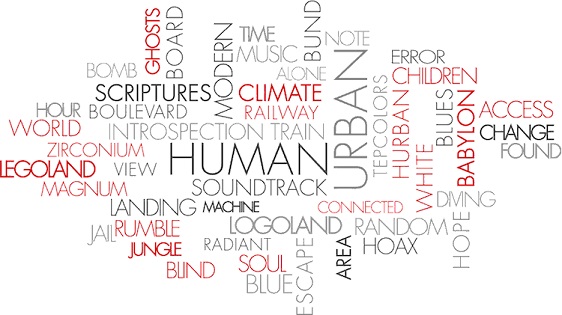

If you could choose just one photo exhibit to see all year, it would have to be Hurban Vortex in Cannes.

Often, photography is the visual equivalent of telling a one-word story, expressed through an immediately comprehensible image. In contrast, Parisian photographer Boris Wilensky takes you on a journey through time, space, and humanity. His photos are true documentaries which require time to contemplate, and listen to. Yes, listen to, not just look at. Because all of his work tells a powerful, juxtaposing story. A story of humans in cruel, all-consuming urban environments… facing challenges beyond their control… surviving in harsh conditions… A story that is already written but that is reinvented every time you look at the image.

Boris Wilensky’s current exhibition Hurban Vortex at the Suquet des Art(iste)s in Cannes opened on December 9 last year, featuring a selection of 30 of his works. Much has been said and written about it, and him, since, so no further biographical introduction is needed. And what really shaped his life, are locations rather than dates – Israel and Palestine, Tokyo, Fukushima, and Cambodia.

An emotional trip to Israel and Palestine in 2005 left a big impression on the idealistic young man, and he started keeping and publishing travel journals to share his impressions. At some point he began illustrating those with photos. Meanwhile he kept working as a photographer in entertainment and sports.

In 2008, a café in Paris offered him space to display his photos. Thinking to himself, “This is a great opportunity… probably the only one I’ll ever have to exhibit”, he went for it. It was a success, and the impetus to turn his passion into a profession.

A visit to Tokyo in 2009 would prove to be the pathway into that professional career as an art photographer. The swirling, frenzied city of dazzling lights around the clock inspired him to find a way to capture the craziness of the megalopolis and the loneliness of its citizens … and he found a way to do so by superimposing two photos taken in the Tokyo subway, of the train and its travelers. It turned out so well that this type of photography would soon become his signature.

On his next visit to Japan – and in fact to Fukushima, just one month after the 2011 reactor catastrophe there – he found a country that had profoundly changed. The Japanese were beginning to awaken to the consequences of boundless, unchecked use of nuclear energy. As a consequence, the garish lights all over town were dimmed, and the mood had become much more somber and sober.

This was when the Hurban Vortex project started taking shape in the artist’s mind. “Hurban Vortex is an urban adventure with a big H”, he explains, the constant game between the concepts of humanity and urbanity, extending into notions of modernity and identity, future, sustainable development, ecology and economy. The City, symbolizing Progress and Modernity, in constant growth, now become a “megalopolis”, or a “City-world”, a space built by humans to live in but one that eats them up in return.

For this project, and forever drawn to Asia, Boris Wilensky returns to Tokyo, Shanghai and Bangkok to take as many “photographic backgrounds” as possible. Then he tours Cambodia for two months, the stark contrast to the other cities’ modernity. Here he immerses himself fully in the ancient Khmer culture, taking portraits of men, women and children. Many of those faces bear silent witness to the horrors of the Khmer Rouge regime, and yet retain pride and dignity that speaks of inner strength.

Over 15,000 photos later, Hurban Vortex sees the light of day. The ensemble of artistic, esthetic and human adventure are at the core of the triptych that represents his works: Origins corresponds to 2009 (present), the period of an oblivious, profligate, consumerism-driven world. Collapse takes us into 2011 (future)…Fukushima, with its worldwide impact. The glasses and gas masks worn by the humans represent the man-made destruction of a world as we had known it before and which will never be the same. And in Post we find ourselves in an urban landscape filled with waste and shattered ruins. But people are no longer wearing their blinders… Maybe there is hope after all that cities may disappear but humans are still around? Or does the urban jungle always win in the end? You decide, because it is your personal interpretation, after an intense dialogue with the image… exactly what Boris Wilensky wants.

What the viewer sees, is how this artist sees the world – not in the literal but figurative sense. But he does not dictate, he suggests. He considers himself a storytelling portraitist first and foremost, and an urban photographer second. As you look at his large-size pictures (180 x 120 cm), the image in front of you transforms from a flat canvas to a three-dimensional scenography. You are drawn in, pulled onto a stage, you become part of the performance, an actor engaged in a dialogue. You are the person across from the man in the photo, but you also become him, turning outward to the viewer.

The continuous movement – the vortex – pushes and pulls you as the borders between Human and Urban blur and become Hurban. There are violently cold and anonymous city landscapes, consisting of monochromatic and starkly geometric patterns, entirely unlike anything you find in nature. But the human element, superimposed, invariably bestows them with a strangely appealing aesthetic. For the Silo, Natja Igney. This article originates at Riviera-buzz.Banner diptych image Boris Wilensky- concept by Jarrod Barker.

LOS ANGELES – Toei Animation Inc. will debut an English subtitle simulcast of Dragon Ball Super on multiple digital platforms on October 22nd. For the first time, fans in North and Latin America, South Africa, Australia and New Zealand will be able to view Dragon Ball Super simulcast. Since its debut in Japan in July 2015, the hit follow-up to one of the greatest anime series of all time has been eagerly awaited by followers around the world. Through non-exclusive streaming partnerships with Crunchyroll, Daisuki.net and Anime Lab, Dragon Ball Super will finally be available.

Kicking off on Saturday October 22 at 9:00pm EST, viewers of Crunchyroll, Daisuki and Anime Lab can log in for a non-exclusive English-subtitled simulcast of episode 63, “Don’t Define Saiyan Cells! The Curtain Rises on Vegeta’s Intense Battle!!” which leads into the thrilling conclusion of the “Future Trunks Arc.” Audiences will get to join Japan live during the broadcast, and then tune in weekly for future new episodes.

Crunchyroll: USA, Canada, Australia/New Zealand for subscription viewing on demand (SVOD) and advertising video on demand (AVOD). Latin America and South Africa can only be viewed on SVOD.

Daisuki.net: USA, Canada, Australia/New Zealand for SVOD & AVOD

Anime Lab: Australia and New Zealand for SVOD & AVOD

Dragon Ball Super’s fourth arc features the return of Future Trunks. Hunted by a mysterious being bent on destruction, Future Trunks is brought into a fight spanning time and space. Episode 63 follows Future Trunks’ epic battle against Goku Black, and Goku’s acquisition of the powerful “Evil Containment Wave” technique.

To prepare for episode 63’s debut, viewers will also be able to stream the entire Future Trunks arc (the arc begins at episode 47). Then, starting on October 30, the complete series will roll-out, with 10 episodes released a week at a time.

“Patience always pays off, and we’re delighted to finally share Dragon Ball Super with our fans around the world. And believe me when I say there’s more to come. Stay tuned for additional exciting news before the end of the year!” said Masayuki Endo, President of Toei Animation Inc.

About Toei Animation Inc.

Based in Los Angeles, Toei Animation Inc. manages the film distribution of Toei’s top properties, including Dragon Ball all series, Sailor Moon, One Piece, Saint Seiya, and many others to North America, Latin America, South Africa, Australia and New Zealand. Toei Animation Los Angeles office further handles all categories of consumer product licensing based on its film and television brands within these territories. For more information, please visit http:www.toei-animation-usa.com or contact marketingdirector@thesilo.ca.

Do you have Dragonball stuff to share with us? Send us your webcam/smartphone camera feed now (or uplink us with your media files) by clicking here- [vidrack align=”right”]

Toei Animation Co., Ltd

Toei Animation Co., Ltd. (Jasdaq:4816) ranks amongst the world’s most prolific animation production studios. The company’s operations include animation development and production, and worldwide marketing and program licensing with sales offices in Paris, Hong Kong and representative office in Shanghai. Since its founding in 1956, Toei Animation Co., Ltd. has produced more than 11,000 episodes of TV series (more than 200 titles) and more than 215 long feature films. For more information, please visit http://www.toei-anim.co.jp.

About Golden Concept

About Golden Concept

If you could choose just one photo exhibit to see all year, it would have to be

If you could choose just one photo exhibit to see all year, it would have to be

Over 15,000 photos later, Hurban Vortex sees the light of day. The ensemble of artistic, esthetic and human adventure are at the core of the triptych that represents his works: Origins corresponds to 2009 (present), the period of an oblivious, profligate, consumerism-driven world. Collapse takes us into 2011 (future)…Fukushima, with its worldwide impact. The glasses and gas masks worn by the humans represent the man-made destruction of a world as we had known it before and which will never be the same. And in Post we find ourselves in an urban landscape filled with waste and shattered ruins. But people are no longer wearing their blinders… Maybe there is hope after all that cities may disappear but humans are still around? Or does the urban jungle always win in the end? You decide, because it is your personal interpretation, after an intense dialogue with the image… exactly what Boris Wilensky wants.

Over 15,000 photos later, Hurban Vortex sees the light of day. The ensemble of artistic, esthetic and human adventure are at the core of the triptych that represents his works: Origins corresponds to 2009 (present), the period of an oblivious, profligate, consumerism-driven world. Collapse takes us into 2011 (future)…Fukushima, with its worldwide impact. The glasses and gas masks worn by the humans represent the man-made destruction of a world as we had known it before and which will never be the same. And in Post we find ourselves in an urban landscape filled with waste and shattered ruins. But people are no longer wearing their blinders… Maybe there is hope after all that cities may disappear but humans are still around? Or does the urban jungle always win in the end? You decide, because it is your personal interpretation, after an intense dialogue with the image… exactly what Boris Wilensky wants. What the viewer sees, is how this artist sees the world – not in the literal but figurative sense. But he does not dictate, he suggests. He considers himself a storytelling portraitist first and foremost, and an urban photographer second. As you look at his large-size pictures (180 x 120 cm), the image in front of you transforms from a flat canvas to a three-dimensional scenography. You are drawn in, pulled onto a stage, you become part of the performance, an actor engaged in a dialogue. You are the person across from the man in the photo, but you also become him, turning outward to the viewer.

What the viewer sees, is how this artist sees the world – not in the literal but figurative sense. But he does not dictate, he suggests. He considers himself a storytelling portraitist first and foremost, and an urban photographer second. As you look at his large-size pictures (180 x 120 cm), the image in front of you transforms from a flat canvas to a three-dimensional scenography. You are drawn in, pulled onto a stage, you become part of the performance, an actor engaged in a dialogue. You are the person across from the man in the photo, but you also become him, turning outward to the viewer. The continuous movement – the vortex – pushes and pulls you as the borders between Human and Urban blur and become Hurban. There are violently cold and anonymous city landscapes, consisting of monochromatic and starkly geometric patterns, entirely unlike anything you find in nature. But the human element, superimposed, invariably bestows them with a strangely appealing aesthetic. For the Silo,

The continuous movement – the vortex – pushes and pulls you as the borders between Human and Urban blur and become Hurban. There are violently cold and anonymous city landscapes, consisting of monochromatic and starkly geometric patterns, entirely unlike anything you find in nature. But the human element, superimposed, invariably bestows them with a strangely appealing aesthetic. For the Silo,

To prepare for episode 63’s debut, viewers will also be able to stream the entire Future Trunks arc (the arc begins at episode 47). Then, starting on October 30, the complete series will roll-out, with 10 episodes released a week at a time.

To prepare for episode 63’s debut, viewers will also be able to stream the entire Future Trunks arc (the arc begins at episode 47). Then, starting on October 30, the complete series will roll-out, with 10 episodes released a week at a time.