About 14 percent of Canadians aged 12 and older – approximately 4.6 million people – did not have a regular health-care provider in 2022, according to Statistics Canada. Even more alarming, about 6.6 million Canadians rely on family doctors aged 65 and over, meaning that even more people could soon find themselves adrift as their physician retires.

Canada has the highest number of general practitioners per capita among comparator countries, yet ranks worst in terms of having a doctor or a regular place for medical care (only 86.2 percent of surveyed Canadians had one in 2023).

What is happening?

Several factors are at play.

First, it’s no secret that the physician workforce, much like the rest of our population, is aging. There aren’t enough new graduates to replace retiring physicians and meet the needs of a growing population. [Canada currently has one of the highest Immigration rates in the world with rates growing steadily and currently sit at around 1.2% population increase each year. CP]

Moreover, physicians have been spending fewer hours on direct patient care. Administrative tasks, such as paperwork for insurance claims, sick notes, and duplicate form requests from different organizations, consume approximately 18.5 million hours of physician time annually in Canada, equivalent to 55.6 million patient visits. Economic and cultural factors are also steering medical trainees towards specialties rather than general family practice. Without changes, the gap between the supply and demand for family physicians will only widen.

My recent C.D. Howe Institute analysis shows that under a normal retirement scenario – where 57 percent of family physicians aged 75 and over retire – the projected supply of family physicians in 2032 will meet 90 percent of the demand. If all family physicians aged 75 and over were to retire, only 78 percent of projected demand would be met, leaving us 13,845 family physicians short.

This means that about 9.6 million Canadians could be without a family physician in the next decade. The consequences of this shortage could be dire, leading to delayed or inadequate care, increased costs, and a strain on other parts of the healthcare system.

With only about 1,550 family physicians completing residency in 2022, the current pipeline of graduates is insufficient. What needs to be done?

Increasing numbers is essential, but will not suffice to meet the demands of a growing and aging population. We need a comprehensive strategy, and five well-established strategies can help.

First, we need to increase the number of training positions for prospective family doctors and accelerate pathways for international medical graduates to enter family medicine, whether direct-to-practice or through residency positions.

Second, administrative processes need to be streamlined to reduce family physicians’ unnecessary workload, freeing more time for direct patient care.

Another strategy is to introduce payment models such as capitation or bundled payments that better support family physicians, making family practice more attractive and encouraging more patient enrolment and after-hours care.

As well, allowing other primary-care providers, such as nurse practitioners and pharmacists, to take on a broader range of responsibilities could assist with sharing the workload and improving patient access.

Finally, developing and expanding team-based models of care that bring together health-care professionals to provide comprehensive and continuous patient care could also benefit Canadians.

The good news is that some of these steps are starting in some provinces.

Nova Scotia is advancing on all fronts; creating a new designated pathway to residency for international medical graduates; committed to reducing physician red tape by 80 percent by 2024; is a leader in paying family physicians with alternate payment; introduced pharmacist-delivered primary care for 31 minor ailments; and expanded team-based care at new and existing locations. Similarly, British Columbia and Ontario have made notable advancements in several of the five strategies.

Improving primary-care access is a nationwide challenge that requires concerted efforts and innovative solutions. By learning from the policies and experiences of different provinces, Canada can develop and implement effective strategies to ensure every Canadian has access to a family physician and the primary care they need. Canada’s health-care system – and the health of its people – depends on it.

For the Silo, Tingting Zhang -Junior Policy Analyst at the C.D. Howe Institute.

An increasing number of Canadians can’t afford a house or find a decent-paying job. Some can’t find a date or are fed up with the bitter politics, while others are in search of adventure, are sick of the cold winters, or simply miss the feeling of ‘being home’.

The solution they seek? Leave Canada.

The rising cost of living, record-high immigration, a stagnating economy, and political tensions are prompting rising numbers of Canadians—both native and naturalized—to leave the country.

Canada is increasingly becoming a country of emigrants, as well as a country of immigrants, experts say.

“We’re definitely seeing a lot more interest from people wanting to leave Canada,” Michael Rosmer, founder of Offshore Citizen, a Dubai-based company that offers relocation services to people around the globe. “This is disproportionate to their numbers overall.”

He said many of his clients are motivated by the increasing ability to work from anywhere, plus political tensions within Canada accompanied by a feeling of lost freedoms. Also a factor is the rising standard of living of many countries that were once far below Canada in terms of health care, education, and other services.

While Canada was once considered among the best places in the world to live, “it’s like the world has flipped,” Mr. Rosmer said. “The alternatives have gotten meaningfully better. Today if you go to Kuala Lumpur you’re going to find that it is arguably better than any Canadian city.”

Some 94,576 people emigrated from Canada from mid-2022 to mid-2023, an increase of 1.8 percent from 92,876 in the year-earlier period, and up sharply from 66,627 in the period from mid-2020 to mid-2021, which fell during the pandemic lockdowns, according to data from Statistics Canada.

A study released last year by the immigration advocacy group Institute for Canadian Citizenship (ICC) showed immigrants are also increasingly reluctant to stay, with the proportion who stick around to obtain full citizenship within 10 years of receiving permanent resident status plunging to 45.7 percent in 2021 from 60 percent in 2016 and 75.1 percent in 2001.

Cameron MacDonald, a 29-year-old from the Niagara Falls region of Ontario who left Canada in March for Japan, cited the high cost of living as the main reason for his move, which uprooted him from friends, family, and a job as an anti-fraud analyst with a major Canadian bank. He is now studying Japanese and looking for a job with a foreign firm, while living in Tokyo, which has a population density of 6,363 people per square kilometre compared to Toronto’s 4,427.8 per square kilometre.

“Here in Tokyo, the world’s biggest city, I pay $650 a month for a room that I would have had to pay $2,000 for in Toronto.” I had a routine and a cushy bank job and I was even living with my dad after a while but I still couldn’t get ahead financially.”

He said the high cost of housing in Toronto means that all of his friends of a similar age in Canada are still living with their parents and, as many of them consider starting families, they are watching his move with the thought of moving abroad themselves.

“My five-year goal includes a wife, a house, and kids and there’s no way I could afford that in Canada,” Mr. MacDonald said. “You can’t really date and find a wife when you’re living with your dad.”

“In Japan, I wake up with a smile on my face every day,” he said. “It’s like I have found a new passion—I can start a family here.

High Immigration

Like many people, Mr. MacDonald blames Canada’s rapid pace of immigration for driving up the cost of living and forcing him to move abroad.

As of Oct. 1, 2023, Canada’s population was estimated at 40,528,396, a record increase of 430,635 people in the previous three months alone, according to Statistics Canada. That growth rate, at 1.1 percent in a quarter, was the highest since 1957, amid Canada’s baby boom plus an immigration surge fueled by a refugee crisis in Hungary at the time.

In just the first nine months of last year, Canada’s population grew by 1,030,378 people, more than any other year dating back to confederation in 1867, the statistics show. And 96 percent of that growth came from immigration. Overall, the population grew 30 percent since it reached the 30 million figure in 1997.

Canada’s Plan to Welcome 500000 Immigrants by 2025. ascenda.com

Indeed, rapid population growth has outstripped economic growth in recent years, lowering the standard of living in Canada as more people compete for less housing space and place greater strains on health care, education, and other services, according to a study published in May by the Fraser Institute. The study shows Canada’s real gross domestic product per person dropped 3 percent between April 2019 and the end of last year, from $59,905 to $58,111. The only steeper drops in the 40 years covered by the study were from 1989 to 1994, with a decline of 5.3 percent, and the financial crisis of 2008 to 2009, when it dropped 5.2 percent.

Another factor propelling emigration may be the aging of the baby boomer generation. As more Canadians reach retirement age, emigration to the United States, particularly to sunny states such as Florida, is accelerating.

A study by Statistics Canada also shows that high immigration tends to push up emigration because some immigrants move back to their home country. The study showed that 15 percent of the people who immigrated to Canada between 1982 and 2017 returned within 20 years of admission.

Whatever the root cause, the interest in leaving Canada has caught the attention of the global industry of specialists offering services to wealthier emigrants around the world.

Videos created by people seeking to offer second-passport services and other relocation help are growing in popularity. “Nine Steps to Escape Canada,” a YouTube video watched 362,000 times, “5 Reasons to Leave Canada in 2024,“ watched by 261,000 and ”Canada is Dying!,” with 531,000 viewers are some of the most popular.

Jay Suresh, the founder of Goodlife Investor, which offers emigration services to people around the world looking to obtain second passports, foreign tax advantages, and other benefits, says the number of Canadians looking for dual citizenship jumped after the Canadian government banned unvaccinated people from flying or travelling by train in late 2021 until the summer of 2022.

“This was an eye-opener for a lot of people. They got frustrated with just that one citizenship and they wanted multiple citizenships,” he said in a video promoting his company. Now, he says, Canadians are nearly tied with U.S. citizens in searches for second passports, even though the United States has 10 times Canada’s population. For the Silo, Adam Brown.

Featured image: People line up to go through security screening at Pearson International Airport in Toronto on Aug. 5, 2022. (The Canadian Press/Nathan Denette)

As Canada’s aging population continues to grow, there are concerns about the financial and physical capacity to meet its growing care needs.

Seniors’ need for housing and care is a complex issue involving many government policies and, therefore, government has many avenues for the exertion of control and adjustment over the issue. Much room for improvement is evident in the quality of, capacity for, and financial support for meeting these needs. This analysis provides a summary of the challenges and gaps in the current state of senior support policies and provides insights to inform future policy.

This Commentary examines the household spending patterns of seniors, the availability of different housing and care options, the costs of providing care in different settings, and government policies that subsidize support services in homes, retirement communities, and long-term care. The results show that the availability and costs of different services and types of care vary significantly across the country. In particular, seniors with below-median incomes face affordability challenges related to shelter costs, with these costs becoming a potential barrier to access to retirement homes and other support services if not publicly available. Further, there is unmet need for home care across Canada, which invests less in home and community care than other OECD countries.

To ensure there is adequate capacity to provide care for high-needs seniors, provinces should invest in expanding home and community care and prevention.

Previous research has shown that about 30 percent of entries to long-term care homes (LTC) could be delayed or prevented (CIHI 2017). Investing in expanded home and community support services and providing financial supports for low-income seniors to access the care they need where it is most appropriate, can reduce the demand for more intensive (and expensive) LTC or hospital care. There are waitlists for LTC, and “alternate level care” seniors occupying hospital beds, which contributes to higher costs, lower hospital capacity for other treatment, and lower quality of life and declining health for the affected seniors. In addition, a significant proportion of below-median-income seniors face housing affordability challenges. Ensuring housing needs are appropriately met can improve the quality of life of seniors and prevent premature entry into higher levels of care. Differences in the availability of services and how they are funded across the country can inform strategies to improve accessibility and capacity. Notably, Quebec has more seniors’ care spaces, lower vacancy rates and lower rent charges than other provinces, while providing comparatively more support to senior households through tax credits.

Overall, limited fiscal capacity, growing demand due to demographic aging, and the growing costs and complexity of care needs for aging seniors all present a significant conundrum for policymakers. There is a daunting challenge in determining the appropriate level of support, ensuring it is well targeted, and allowing for seniors to choose what is best for them. Government policies should encourage seniors to remain independent as long as possible, but also ensure they have adequate financial resources and access to support services if they are required.

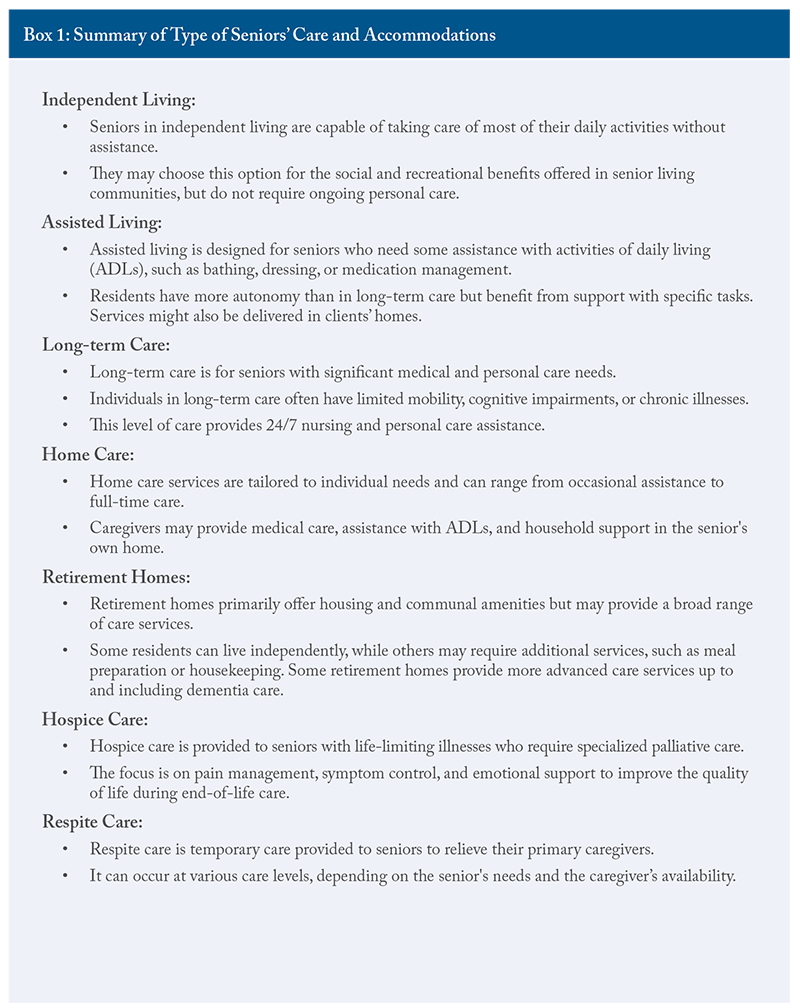

There are multiple options for housing accommodations as seniors age, and the choice will depend on their preferences, families, level of need, and the affordability and accessibility of the various options. This section discusses the different care needs that seniors might have as they age. It also illustrates the continuum of care: seniors choosing assisted/supportive living accommodations or receiving home care will have a range of needs, and care must be flexible enough to suit an individual’s needs.

Activities of Daily Living (ADLs) are a set of essential everyday tasks and activities that individuals typically need to perform to live independently and maintain their overall well-being. These activities are often used in healthcare and long-term care settings to assess an individual’s functional abilities and to determine their level of independence. When someone experiences limitations in one or more of these areas, they may require varying degrees of assistance or care, ranging from minimal support to full-time care. Health professionals use ADL assessments to develop care plans and tailor assistance to meet an individual’s specific needs and promote their overall quality of life. The specific ADLs may vary slightly in different contexts, but the core activities are as follows.

Personal hygiene and grooming: including bathing/showering, caring for teeth, medication management, etc.

Dressing: choosing appropriate clothing and putting it on independently.

Eating: feeding oneself and preparing simple meals.

Mobility and transferring: being able to walk, get in and out of bed, or independent transferring from one surface to another (such as from a bed to a wheelchair).

Toileting and continence: The ability to get on and off the toilet, maintain personal hygiene, and manage incontinence, if necessary.

Medication management: the ability to follow medical care plans without the need for assistance or reminders to take necessary medications.

Instrumental Activities of Daily Living: activities that are not essential to basic self-care, but are crucial to independent living in a community such as managing finances, planning and preparing meals, doing laundry, going shopping for essential items, etc.

Notably, most of the ADLs have little to do with direct healthcare needs. Instead, they are a set of daily activities that could be provided by different types of support services including meal delivery, housekeeping, laundry services, and social activities. Seniors requiring support with some ADLs could benefit from one or more support services, even if they do not have advanced healthcare needs. Healthcare is an important component of supporting seniors to remain independent, however, many of the activities that are required for independence fall outside the traditional scope of healthcare.

The options for support available to seniors are directly related to their care needs. Those who are able to live independently can choose their accommodations based on lifestyle and preferences. Those requiring occasional or minimal assistance can remain in their homes and receive help from family, other informal caregivers, and possibly publicly funded home and personal care services, or they could choose to privately pay for some services such as regular housekeeping or food delivery services. They might also choose to move to a retirement home or community where meals and other services are provided, as well as ongoing opportunities for socialization. As care needs become more intensive, seniors may require ongoing or live-in support from a combination of public or private home and nursing care services, family, or an informal caregiver at home. In the retirement home setting, there are many options to address increasing care needs. However, as care needs become greater, affordability plays a factor in how long a senior might stay in a retirement home before moving to LTC where care needs are generally fully subsidized by government, and room and board charges are limited by regulations.1

At home, those requiring hands-on or total assistance require significant and ongoing care. At this stage, a caregiver must be available at all hours to assist with many basic ADLs, and the options for care become more limited. Those without an available caregiver in the home will likely be best served by residing in long-term care homes that have health providers on site at all times of day. Depending on their health conditions, hospice and palliative care might also be appropriate for end-of-life care. Increasing numbers of retirement homes are offering heavy care and dementia care services, and publicly funded home care can be accessed to supplement some of the costs. This still, however, presents a significant financial burden to seniors. Often, even though a retirement home can safely and appropriately meet the care needs of a senior, LTC becomes the preferred option. Most often, this is because of the cost differential between what the government will subsidize in a LTC setting versus the limited home-care services available to offset privately paid retirement home care costs.2

The options for care and assistance with ADLs reflect progressive levels of need. As care needs become more intense, the options become more limited (and/or costly). Those requiring ongoing care can choose to live in a long-term care home, or might be able to remain in a residential setting – home, retirement home, assisted living facility – if they and their families have the resources to supplement publicly provided services, and if the appropriate services are available privately. Of course, those that are independent have a full range of choices for where they might want to live, except those places reserved for people with higher care needs. More than three-quarters (78 percent to 91 percent) of Canadians would prefer to receive care while continuing to live in their homes as they age, but only one-quarter (26 percent) expect that they will be able to do so (Sinha 2020, March of Dimes 2021). The different types of seniors’ accommodations and short-term respite care programs are described in Box 1. It is important to note that there is overlap between many care options and levels of need – two seniors with similar care needs might use different combinations of services. This is particularly the case for people with minimal to moderate needs for support. Similarly, the options will vary in terms of availability and costs depending on the location, the ownership and operation models of the different residences, and the level of public coverage and involvement in different levels of care. The next section provides a summary of the availability and costs of various seniors’ living arrangements across the country, focusing on provinces with larger populations (BC, Alberta, Ontario and Quebec).

There are 2,076 long-term care homes in Canada. At first glance, LTC in Canada appears to have a comparable amount of beds and financial resources in comparison to international peer countries. Canada has close to the average number of LTC beds relative to the size of the senior population, but still fewer than countries such as New Zealand, Finland, Germany, and Switzerland. It also has a comparable proportion of the senior population receiving LTC care and homecare, relative to international peers (Wyonch 2021). It spends more per capita than the OECD average on funding LTC but spends less than other OECD countries as a proportion of GDP. The GDP proportion of health spending for inpatient LTC is above average (Wyonch 2021).

Despite higher-than-average spending, there are long waitlists for LTC in many Canadian provinces. In Ontario, there were, as of Oct. 2022, almost 40,000 seniors waiting for LTC, and 76,000 receiving care; this means the waitlist currently exceeds 50 percent of care capacity (OLTCA).3

The median wait time was 130 days in 2021/22 (213 days for entrants from the community, and 80 days for hospital entrants) (HQO). In Quebec, the waitlist is much smaller (4,235 as of June 2023). However, seniors might still wait up to two years for a placement (Bonjour Résidences).

The cost of long-term care varies across provinces, but charges payable by the resident to cover room and board are generally standardized by regulation within each province. For example, in Ontario the maximum monthly co-payment for LTC is $1,986.82 – $2,838.49 depending on whether the room is shared or private. In Quebec, room and board charges for public and contracted private long-term care homes (CHSLD or centre d’hébergement et de soins de longue durée) are $1,294.50 – $2,079.90, depending on the type of room. Quebec also has unsubsidized (uncontracted) private CHSLD, where the average monthly costs are between $5,000 and $8,000, depending on resident’s needs (Bonjour Résidences).4More than half of LTC homes (54.4 percent) and the majority of retirement homes are privately owned and operated. There is no consistent ownership pattern across the country: in five provinces, the majority of LTC homes are privately owned and operated, with the other provinces having majority public ownership. All LTC homes in the Territories are publicly owned. Both publicly and privately owned LTC homes provide ongoing care for some of the most vulnerable members of society. At both public and private LTC homes, healthcare is publicly funded and most support services will be included in room and board rents. Seniors must require significant care to qualify for LTC.5

Individuals requiring support who don’t have a caregiver in the home are much more likely to be admitted prematurely to LTC homes. Indeed, about one in nine new entrants could potentially have been cared for at home or in a retirement home setting. These new residents are more likely to have previously lived alone or in a rural area where formal and informal supports are less likely to be available (CIHI 2020b).

Retirement homes offer a wide variety of services and programs targeted at different client types. These include those who are fully independent and wish to live in a congregate setting for the lifestyle and social benefits, those with mild to moderate care needs, those with heavier care needs, and those who require specific dementia care programs and supports. In Ontario, for example,15 percent of homes provide dementia care, 34 percent provide assistance with feeding, and the majority provide services to assist with other ADLs (Roblin et al. 2019). Prices of retirement home care vary significantly by location, as well as by amenities and services offered as they are market driven (and are not generally directly government subsidized). Various provinces have senior rental accommodations that provide care needs: in Quebec the services are called “seniors’ residences”; in BC “assisted living”; in Ontario “retirement homes”; and in Alberta, “supportive living.”

Many retirement homes offer more extensive health and personal care services. These additional services increase costs for seniors since they are either charged as additional services or will be incorporated into higher room and board costs. In Ontario, if these additional services are provided by the retirement home, the additional services are not directly publicly subsidized. In some cases, residents in retirement homes might also receive home care or assisted living support that is provided by a separate agency, either publicly or privately. Most retirement homes are privately owned and operated. Their activities and levels of care provision are regulated by provinces, but prices will be determined by market factors and the amenities and services offered in each location.

In Ontario, retirement communities are regulated by the Retirement Homes Act, 2010 (RHA), and are licensed and inspected by the Retirement Homes Regulatory Authority (RHRA).6Each retirement community can offer up to 13 care designated services, for example, assistance with dressing and personal hygiene, medication management, and providing meals. Services might also be publicly provided through home care. About half of seniors currently living in retirement homes have care needs that would qualify them for publicly provided home and community care. Home care services supplement the care services in the retirement home at no cost to the resident and assist with affordability of the retirement living option for seniors with care needs.

In Quebec, private seniors’ residences are rental facilities that are mainly occupied by people over 65, and offer various services such as nursing care, meal services, housekeeping, and recreation. Private seniors’ residences must hold a certificate of compliance from the Government of Quebec ensuring they comply with health and safety rules. Similarly, in Alberta, the provincial government sets accommodation standards for supportive living facilities. Supportive living operators require a licence if they provide accommodation and support services to more than three people, provide meals or housekeeping services, and arrange for safety and security services. Alberta also has Designated Supportive Living where access is determined by an assessment by a health professional, room and board charges are determined by the Alberta government, and accommodations provide 24-hour publicly funded health and personal care services on site.

In British Columbia, retirement homes are divided into categories: independent living, and assisted living.7Assisted living is divided into three classes: i) seniors and persons with disabilities who have chronic or progressive conditions, ii) mental health care, and iii) substance use care. Assisted living residences provide housing, hospitality services and support services, and they may be privately paid, publicly subsidized, or a combination of both. Independent living seniors’ residences are essentially retirement homes targeted to seniors who need minimal assistance and are not generally publicly subsidized. For seniors requiring assistance, assisted living spaces are publicly subsidized based on income: a maximum of 70 percent of after-tax income goes to housing and support services in assisted living. However, there is a minimum fee of $1,093.50 per individual ($1,665.60 per couple) and maximum monthly rate for publicly subsidized assisted living is based on market rates for rent and hospitality services in the same geographic area.

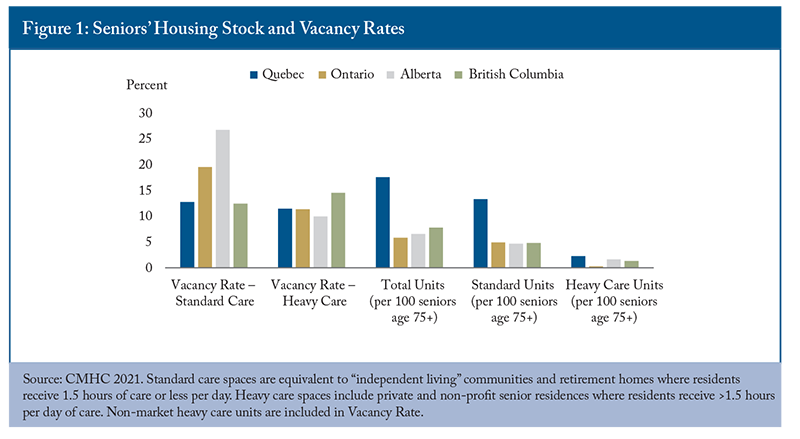

Though individual retirement homes and assisted living facilities might have waitlists, there are fewer concerns about overall capacity. Across provinces, both standard and heavy care spaces are at least 10 percent vacant (Figure 1).

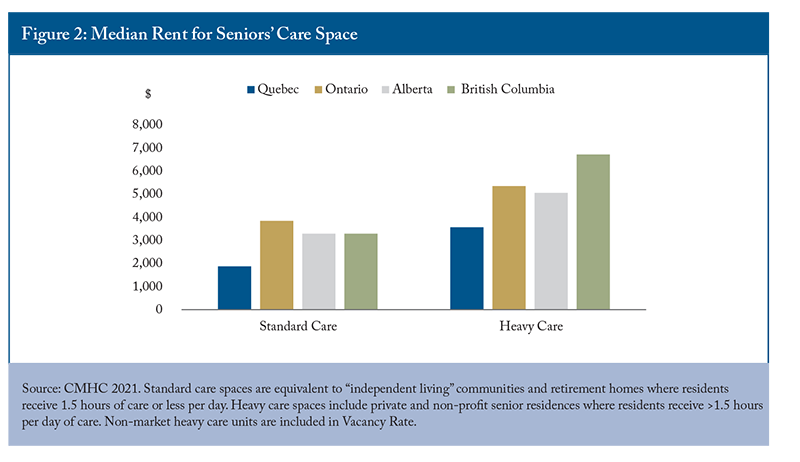

Alberta has the highest vacancy rate for standard care spaces (26.8 percent) and the lowest vacancy rate (10 percent) for heavy care spaces, suggesting a need to transition some standard spaces to heavy care spaces as the population continues to age and care needs intensify across the senior population. Ontario notably has the fewest seniors’ care spaces relative to the size of the senior population, particularly for heavy care units (3.0 spaces per 1,000 seniors over age 75). A long waitlist for LTC and few spaces for seniors with less intensive – but still significant – care needs suggest a need to expand the number of spaces available for seniors across the care continuum. Notably, British Columbia has the highest vacancy rate for heavy care spaces, despite having relatively few spaces (14.4 per 1,000 seniors over 75). It also has the highest rent among provinces for heavy care spaces ($6,726/month) and the largest increase in rent between standard care and heavy care spaces (Figure 2).

Quebec has more than three times the amount of seniors’ housing spaces in comparison to other provinces, relative to the size of the senior population. It also has the lowest median rent for both standard and heavy care spaces by a large margin. Median rent for a standard care space ($1,873/month) is about half the cost of other provinces, and a heavy care space in Quebec ($3,566/month) costs less than a standard care space in Ontario ($3,845/month).8Quebec having triple the supply but similar vacancy rates to other provinces suggests that lower prices are a result of a significantly higher supply of seniors’ care spaces.

Demand is also likely to be higher in Quebec due to policies that indirectly support private seniors’ residences and LTC through medical expense and home care tax credits.

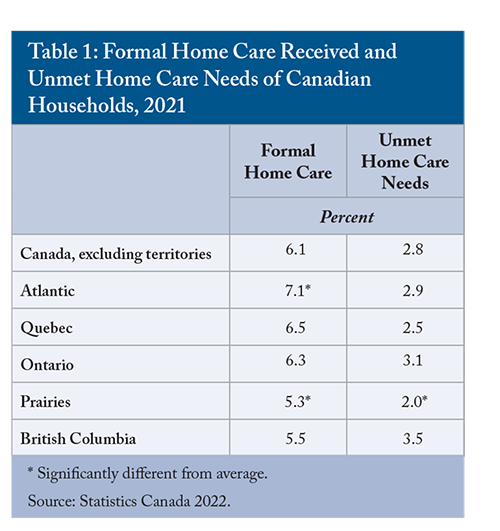

Home care covers a broad range of services, including personal support for ADLs, homemaking services such as housekeeping, laundry services and meal preparation, and can include professional services such as nursing, occupational therapy, or social work. Across Canada, about 6.1 percent of households receive home care services and 2.8 percent of households have unmet home care needs (Table 1). Unmet need is highest in British Columbia and Ontario, and lowest in Quebec and Atlantic Canada. Notably Quebec and Atlantic Canada also have the highest proportion of households receiving home care.

In Ontario, publicly covered services are generally tailored to an individual’s needs and delivered in their residence (a home in the community or retirement home), following an assessment by a case manager or health professional. Services are delivered by third-party agencies that can operate on a non-profit or for-profit basis. In Quebec, seniors can access discounted home help through the Financial Assistance Program for Domestic Health Services program. After approval, seniors receive a discounted hourly rate for various home care and support services provided by qualifying domestic help and social economy businesses.9 Many services provided by home care agencies and domestic help businesses can also be purchased directly through the private market. This option gives a completely free choice of services, without the need to qualify for government assistance, but must be paid for out-of-pocket. In BC, home support services can be purchased privately, or can be publicly subsidized, based on eligibility. If publicly subsidized, home care recipients are charged a daily rate for services, based on their income.1010 In Alberta, home care is narrowly defined as providing medical support for people so they can live in their homes. After an eligibility assessment, services are provided under Alberta Health Care Insurance meaning that if a service is not insured, it is not publicly funded.

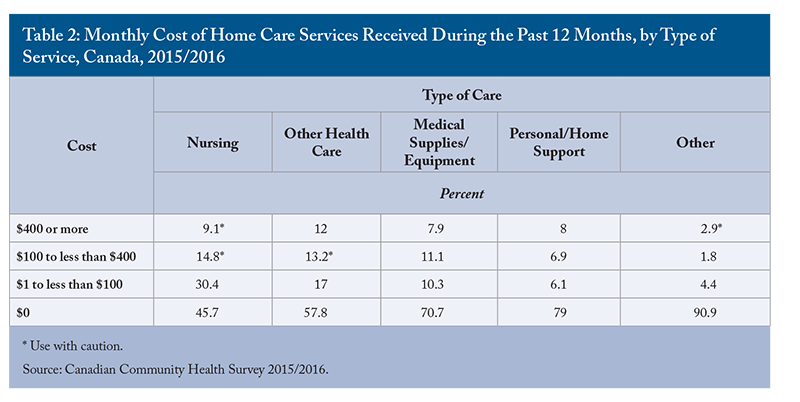

Over half of home care services are paid from government sources (52.2 percent), and 7.3 percent are covered by insurance. More than a quarter (27 percent) are paid for out of pocket (Gilmour 2018). Government sources are more likely to cover health home care services than support services. In 2015/2016, more than half of nursing care services (54.3 percent) and 42 percent of other healthcare services had a monthly cost (Table 2).

In many cases, seniors receiving home care will also receive help from informal caregivers (for example, family members, neighbors, and adult children). Informal care reduces the direct public costs of supporting a senior to maintain their independence in their home, but it can represent economic deadweight loss if informal caregivers reduce their hours of paid work.11In addition to formal in-home services, there are also seniors’ day-programs to provide care throughout the day, and respite care beds for when informal caregivers might need additional support or if the senior needs additional care for a short period of time.

Depending on the jurisdiction, “assisted living” services overlap somewhat with home care and retirement home services, but generally target those with higher care needs.

Assisted living programs are defined differently across the country. In Quebec, “Resources intermediaries” provide housing and access to support services for individuals with minor to moderate loss of autonomy. In British Columbia, Assisted Living provides housing, hospitality, and social and recreational services to adults requiring a supportive environment due to physical and functional health challenges. In Ontario, Assisted Living Services provide support for people with special needs who require services at a greater frequency or intensity than home care, but without the medical monitoring or 24/7 nursing supervision that is provided in long-term care. Services are provided by third-party agencies that operate on a not-for-profit basis. In Alberta, Designated Supportive Living is broken down by levels of service, ranging from 24/7 provision of health and personal care services for those living independently, to providing specialized residential dementia care (AGO 2021).

Assisted living services are generally publicly funded, with limited room and board co-payments when housing is included in services. They are targeted to cover gaps in the continuum of care between independent living options and long-term care, and the services provided can overlap with both to ensure appropriate levels of support are provided and seniors are not prematurely admitted to long-term care.

Alternate Level of Care patients are people occupying an inpatient bed, but whose needs no longer require acute level care. ALC patients occupy 12.7 to 27.5 percent of beds in acute-care centres across the provinces and represent 15.5 percent of all acute-care bed-days in Canada (excluding Quebec) in 2021-2022 (CIHI 2023). ALC patients are most often admitted to acute care as a result of an injury or illness, but subsequently cannot be discharged home as their clinical condition requires new additional support and/or care services such as home care, transfer to a long-term care facility, or another form of specialized care (rehabilitation, psychiatric or complex). In some cases, ALC patients might be admitted for predominantly social reasons: no acute or rapidly accelerating medical condition is present, but certain circumstances force patients and caregivers to turn to emergency departments (for example, real or perceived failing of social services or lack of adequate community supports) (Durante et al. 2023).

ALC patients represent a complex health system challenge with many contributing factors. Lack of access to preventative and primary care services, or to home care and other social services, can result in patients going to emergency rooms when an alternate level of care would be more appropriate. Similarly, a lack of capacity in home care or long-term care can result in ALC patients remaining in hospitals for extended periods of time. Both scenarios represent an inefficient use of limited (and expensive) hospital resources and constrain capacity to provide acute care. From a financial perspective, each ALC patients represent a cost of $730 to $1,200 per day to Canada’s healthcare systems (Whatley 2020).12

While inefficient spending is concerning, preserving limited acute care bed capacity is necessary to prevent bed shortages and ensure accessibility for Canadians. Canada has fewer hospital beds relative to the size of the population than most OECD countries, and high occupancy rates in acute care beds show that the system is strained. While there is no agreed upon “optimal” occupancy rate, 85 percent is often considered the maximum rate to reduce risks of bed shortages. The average across OECD countries was 69.8 percent in 2021. Canada was one of three countries to have a rate over 85 percent and had the fewest beds per capita in the high-occupancy group (OECD 2023).13If Canada reduced the number of ALC patients and the number of days an ALC patient spends in hospital, it could significantly reduce acute care capacity concerns. A 13 percent reduction in ALC days would be sufficient to bring acute care occupancy down to below the 85 percent occupancy threshold to prevent hospital bed shortages, since ALC patients currently occupy 15.5 percent of capacity.

There are opportunities to reduce ALC patient days, both from within the hospital setting and by improving and expanding community and support services. Increasing the number of seniors’ care spaces, increasing the scope and provision of home care, improving primary care access and ensuring that necessary support services are accessible and affordable for seniors would all alleviate the strain on hospitals by preventing admissions and allowing for more rapid discharge of ALC patients to alternate levels of care. Within hospitals, incentives for physicians, families, and the hospital generally encourage longer than optimal stays. Front-line clinical staff (especially physicians) have strong incentives to avoid conflict and risks resulting from acute-care discharges (Chidwick et al. 2017).14Hospitals in some provinces charge a daily fee to recoup the costs resulting from ALC hospitalizations. The fees are generally equivalent to the daily rates for room and board in LTC, not the full cost of an acute care bed. This means that there is little incentive for seniors or their families to prefer one care setting over the other if a patient is destined for long-term care. The hospital, however, cannot charge patients this fee unless they need continuing or chronic care – destined for more or less permanent institutional care.15Hospitals, therefore, have an incentive to designate ALC patients as chronic and in need of long-term care, so that they can recoup costs. In Quebec, hospitals do not charge fees related to ALC. In that case, seniors and their families have an incentive to prefer hospital care over home care, a retirement home or a long-term care home since these options do have financial costs. Provinces should examine their hospital fee policies related to alternate level care to ensure that clinicians, hospitals, and seniors are not incentivized to provide or receive more advanced healthcare services than are necessary to meet the needs of the patient. Hospitals should also evaluate policies and guidance for clinicians and front-line workers on making discharge decisions to reduce referral to long-term care when it can be avoided.

Addressing the unmet care and housing needs of seniors could significantly reduce the number of ALC patients and their lengths of stay in hospitals. Reducing ALC days and admissions would likely be sufficient to reduce the strain on acute care capacity to levels more comparable to international peers and reduce the risk of bed shortages.

Different settings and types of service provision, with different public programs and levels of subsidization, make comparison across provinces challenging. In this section, I compare public costs of seniors’ healthcare across the country and provide estimates of the public costs of care provision across different settings in Ontario and Quebec.16

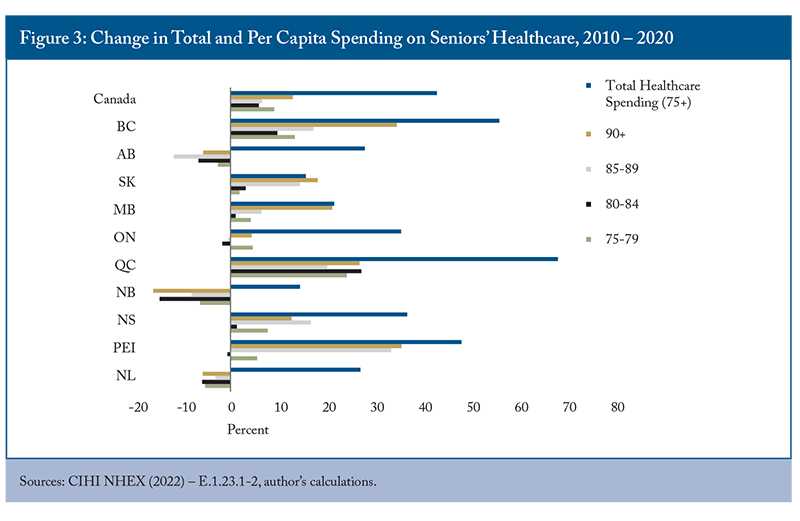

Rather unsurprisingly, per capita health expenditure increases with the age of the population, since older and frailer individuals have increasingly intensive healthcare needs. There is some variability between provinces, with New Brunswick and British Columbia having lower spending per capita on care for seniors. Across the country, more than $1 of every $4 of provincial government healthcare spending goes to caring for people over 75 years of age. From 2010-2020, total provincial and territorial government spending on healthcare for the population over 75 increased by 40.5 percent to $52.77 billion, while total government spending on healthcare increased by 56 percent. In some provinces, increases in seniors’ healthcare spending have been driven by growth of the senior population (ON, NS) (Figure 3). Some provinces have contained these increasing costs by reducing per capita spending on seniors’ healthcare (NB, AB, NFL). In others, both increasing senior populations and increased per capita spending contribute to spending growth (QC, PEI, MB, SK and BC). Only in PEI and BC has spending on seniors’ care kept pace with overall increases in healthcare spending.

Meanwhile, seniors are spending more on their own healthcare and living expenses. In 2019, the average senior household (75+) spent $14,440 on housing and $3,260 on healthcare (Table 2). Healthcare costs have stayed relatively constant in real terms from 2010 to 2019, and increased less than total consumption, though private insurance premiums have increased by 117 percent. Food and shelter costs, however, have become more expensive. Seniors who rent their homes are facing challenges in addition to affordability, with more than half of those in unsubsidized rental units having inadequate, unsuitable, or unaffordable housing (Table 3). As needs increase with age, the cost and availability of options will factor into the lifestyle choices seniors make about where they live.

In Ontario, a senior with high care needs would likely qualify for long-term care or assisted living. If those services aren’t readily available, they might require a stay in hospital as they wait for an assisted living or long-term care bed to become available. Regardless of the care setting, the personal costs are similar.17

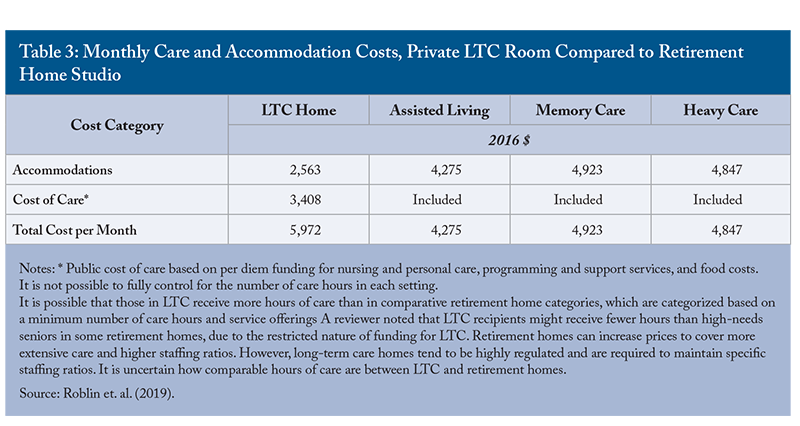

From a public finance perspective, however, there are different costs associated with different levels of care. A hospital stay for someone over 80 years of age ranges in cost from $4,306 to $11,361 per episode of care. Long-term care costs the province $5,870.70 per month per patient, and the average cost of assisted living is about $1,494 per month per patient.18Previous analysis has shown that the total cost of care is lower in heavy care retirement spaces than in LTC, and that public costs are significantly lower due to residents paying privately for services in retirement homes (Table 3). Public spending is lower if people receive advanced care services at home, or in retirement homes, than in long-term care. Hospitals are the worst option. They have the highest public cost and are also a limited resource. Every hospital bed occupied by an alternate level care patient (ALC) carries an opportunity cost and makes the bed unavailable for acute or critical care, or surgical rehabilitation and monitoring.

The picture for high needs patients in Quebec is similar to that in Ontario, but with notable distinctions. There are no private costs for a hospital stay in Quebec, and room and board charges for public LTC range from $1,294.50 per month to $2,079.90. Quebec has private LTC homes that cost residents $5,000 to $8,000 per month, depending on level of care need.19The public cost of a hospital stay for a patient over 80 years of age is higher in Quebec than in Ontario ($5,627-$14,488), as is the level of subsidization of public LTC ($5,837.73 – 9,379.60 per month per client, depending on type of room). There are similar public costs associated with a hospital stay or a month in LTC in Quebec, but the need to preserve scarce hospital resources remains, meaning that from a public cost perspective, the preference would be for high needs patients to be in LTC homes. If the senior can afford it, a heavy care bed in a private retirement home or private LTC home is most beneficial, from a public finance perspective. Research has shown that the government pays 79.7 percent of residential care costs and 81.7 percent of nursing home costs, or about $53,500 per user of a residential care facility and $82,400 per user of a long-term care facility. Comparatively, home care is estimated to cost $7,140 to $23,634 per client, depending on level of care need (Clavet et al. 2022).20

For mild to moderate needs, seniors can depend on informal caregivers, public or private homecare services, nursing services, or they can choose to live in retirement homes offering the services they need. In many cases, some combination of services is required. Home care services in Quebec can be heavily discounted depending on the level of assistance qualified for under the “Domestic Help” program. In Ontario, those qualifying for public homecare services don’t have out-of-pocket costs.21 In both provinces, homecare services can also be acquired privately, in which case there is no direct public cost.22 In both provinces, retirement homes are generally privately owned and operated and offer a variety of services across a spectrum of care needs. In Ontario, the average rent for a retirement home is $3,845 per month, representing a less affordable option when compared to average household costs.23 In Quebec, retirement homes represent a slight savings compared to the average senior household’s expenses.24Quebec has many more senior living spaces than Ontario, relative to the size of the population. It also has a much lower vacancy rate. As discussed in detail in the next section, different tax credits in each province provide different levels and types of support which likely affect both the accessibility of different types of support services and the distribution of seniors’ receiving care in each setting.

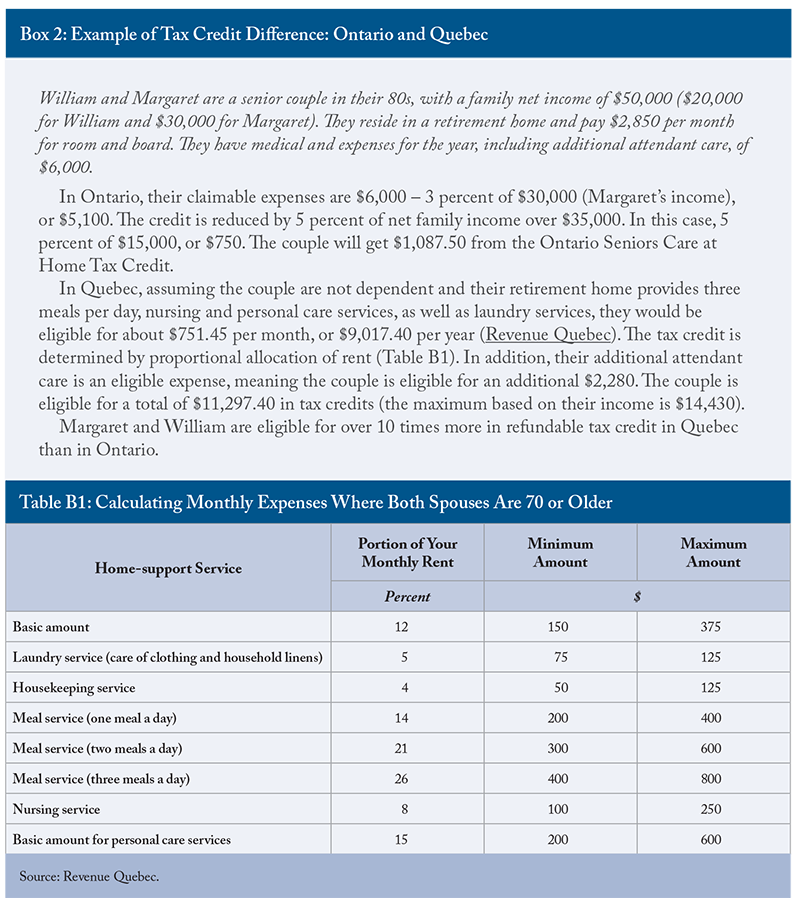

In addition to publicly provided services and subsidies on home and health care services, there are also tax credits that reduce the cost of support services and equipment for seniors. Quebec makes more expansive use of tax credits to support seniors remaining in their homes as they age than Ontario. People over 70 years of age in Quebec can claim up to 38 percent of eligible expenditures through the refundable tax credit for home support services.25 Services eligible for the tax credit include meal preparation or delivery services, nursing care services, home and personal care services (such as housekeepers, landscapers, or aides to assist with bathing, dressing, feeding etc.). For homeowners, only eligible services can be refunded. For tenants, however, a portion of rent can be considered if it includes eligible home support services. Similarly, retirement home residents can claim the portion of their rent that relates to meal preparation and home care services. The total amount that can be refunded takes into account total income, level of dependence, family structure, and the eligible expenses incurred throughout the year. An independent senior could qualify for a maximum of $7,020 in refundable credits based on the maximum service spending of $19,500. Dependent seniors can be eligible for up to $9,180 in refundable credits. The credit is reduced when family income exceeds $69,040.26

In Ontario, residents over 70 years of age can claim up to $1,500, or 25 percent of eligible expenses up to a maximum of $6,000, through the Ontario Seniors Home Care Tax Credit. Eligible expenses fall into several categories including walking aids, hearing devices, wheelchairs, hospital bed for home use, oxygen, vision, dental, or home nursing care. The maximum tax credit is reduced by five percent of family net income over $35,000, meaning about a quarter of households with a member over the age of 75 will qualify for the maximum credit. Claimable expenses are amounts over 3 percent of net income. The Ontario home care tax credit covers both services and equipment but does not allow for rent deductions, while the Quebec credit is for eligible service expenses only. Notably, the level of support provided by the Ontario tax credit is lower than that in Quebec. It covers a smaller proportion of the population and refunds a significantly lower amount. See Boxe 2 for examples of the difference in refundable tax credits for a senior couple in each province.

The federal government and Quebec also offer tax credits for improving home accessibility. The federal home accessibility tax credit is available to people 65 years of age or older, or those with a disability. Eligible recipients can claim up to $10,000 related to renovations or purchasing equipment that improves the accessibility and safety of the home. The renovations must be of an enduring nature and could include wheelchair ramps, walk-in bathing installations, and support bars. Quebec’s tax credit is similar to the federal credit. The Quebec Independent Living tax credit for seniors covers 20 percent of eligible expenses over $250.

There are also tax credits to support informal caregivers. At the federal level and in Ontario and Quebec, immediate family members can claim a tax credit for providing care for a disabled relative. Quebec also offers a refundable tax credit of 30 percent of total expenses for caregivers paying for respite services that provide a short-term replacement for care and supervision of a disabled relative.27

The tax credits available to help seniors stay in their homes are quite expansive, and generally consider age and household income levels. In some cases, the tax credits have restrictive criteria, such as requiring the person receiving care to have a disability, making them more targeted to the population requiring more intensive and ongoing care. In Quebec, the home support tax credits go a step further than in Ontario by including a portion of rent related to services, making retirement home care partially eligible, and by separating tax credits related to devices and services. The tax credits are also available to different age groups: tax credits for home equipment become available at age 65 under federal and Quebec subsidies and are available to those 70 and older in Ontario. Both Ontario and Quebec have reserved tax credit eligibility for home nursing care and other home care services to those age 70 and over. The timing of the availability of tax credits loosely follows the progression of care needs as people age and is targeted at the population in need of assistance – without requiring medical assessments and case managers to determine eligibility.28

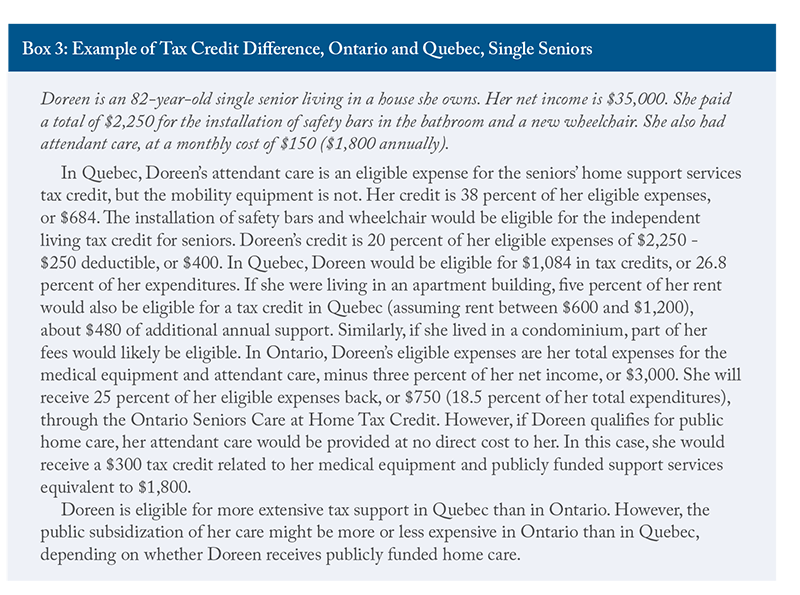

However, there is a significant difference in the level of support provided between Ontario and Quebec. As the examples in Boxes 2 and 3 show, the question of whether a senior lives in an owned home or rented accommodations (including retirement homes) significantly changes the level of tax subsidization received in Quebec, but not Ontario. In either case, seniors are likely to qualify for more refundable tax credits to support independent living in Quebec than in Ontario.

Developing public policies to support seniors as they age should be informed by seniors’ preferences and levels of need. Some senior households requiring lifestyle or healthcare services have the financial resources to invest in adapting their homes, or to pay for services.

Many seniors are homeowners and have the ability to downsize or transition to a retirement home or other rented accommodations using the unlocked equity to pay for their accommodations or supplement publicly provided healthcare and lifestyle support services. A significant number of senior households, however, face affordability challenges and are in inadequate or unsuitable housing. This section provides a brief overview of the household spending patterns of seniors and their housing needs, with the aim of informing policies that best provide targeted support to seniors most in need.

The Household Spending Survey from Statistics Canada provides insights into the number, composition, and spending patterns of households across the country. According to the 2019 survey data, there were about 1,991,750 households with at least one person over the age of 75, representing 13.5 percent of the total.29 Nova Scotia has the highest proportion of households with seniors (15.24 percent) and Alberta has the lowest (10.77 percent). The data show that while the majority of households with seniors are living within their means, senior households with below-median incomes, and those who rent, are more likely to face affordability challenges or have difficulty accessing adequate and suitable housing.

Most seniors live alone or as a couple (42 percent and 35 percent, respectively). The distribution of seniors among housing types is similar to the rest of the population; a majority live in single detached houses (54 percent) and about 3 in 10 live in apartments or condos. The majority of senior households own their home without a mortgage, and seniors are more likely to own a second property than the population average. The majority of households with seniors depend on government transfers as their main source of income (52 percent), followed by other forms of income (27 percent) and employment earnings (17 percent).30In general, 75+ households have lower spending and consumption than the average household and spend a lower proportion of their income.31 Senior households spend less than the average in all categories except healthcare and custodial services (though they still spend less on household operations overall). Examining average income and consumption patterns across provinces shows that the average household with at least one person over the age of 75 can meet its needs and still reserve about 30 percent of income as savings, a similar rate to households overall.

Averages, however, can mask more worrisome spending and consumption patterns at the lower end of the income distribution. Households with below-median income have consumption expenditures that exceed their incomes.32 Shelter and food costs represent about 46 percent of consumption expenditures across lower-income households in general, and 53 percent for lower-income households with seniors. Shelter costs exceed the 30 percent affordability threshold for below-median-income households with seniors.33 It is difficult to determine the level of need from these data alone, since many seniors have significant savings to support their consumption. Lower-income seniors who do not have significant savings would be more likely to face affordability challenges. Ontario has the lowest spending on shelter for lower-income households with seniors ($8,862), and those households have significantly lower shelter costs than the average across lower-income households in the province.34 In Quebec and Alberta, shelter costs exceed 35 percent of consumption expenditure for senior households. In British Columbia, seniors who rent spend 46.1 percent of their income on shelter.

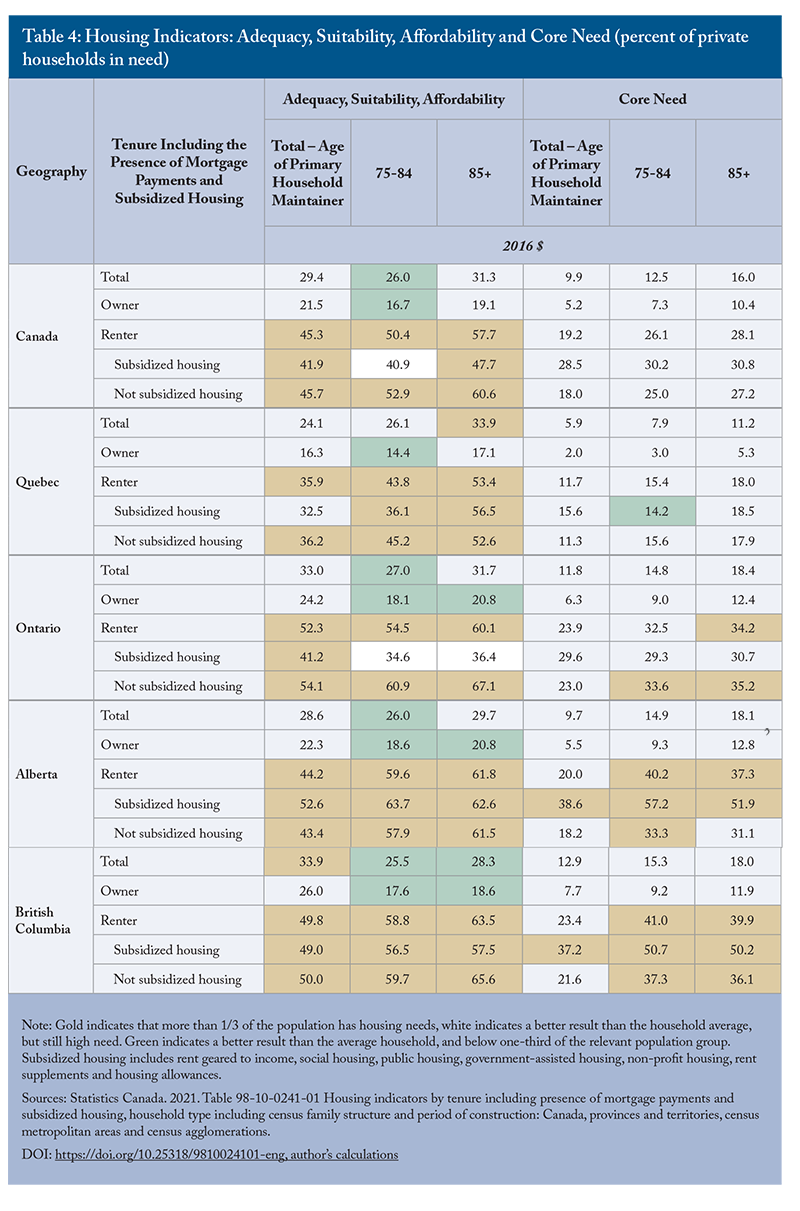

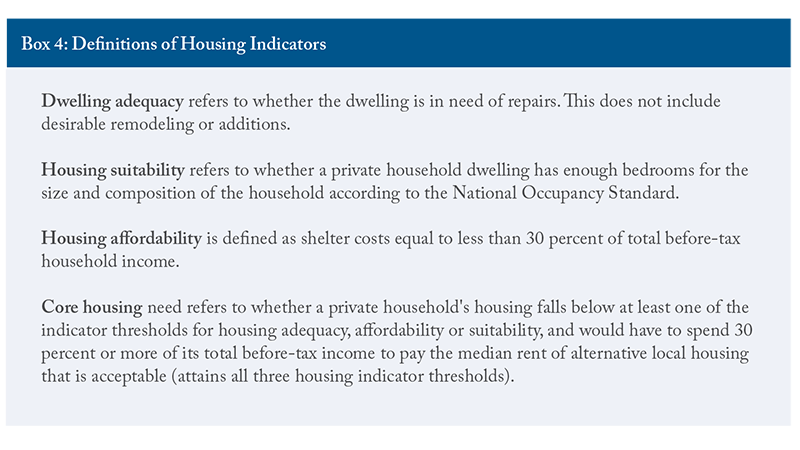

The importance of shelter costs to seniors’ expenditures, particularly below-median income households, warrants further investigation. Statistics Canada’s housing indicators provide further details. Households where the primary maintainer is over the age of 85 generally have higher rates of housing inadequacy, unaffordability, and unsuitability than the average across all households (Table 4). Seniors show higher rates of “core need” housing than the general population (see Box 4 for definitions of housing indicators).

In all major provinces, more than a third of renters are in housing that is inadequate, unsuitable, or unaffordable. There are some challenges related to housing indicators for homeowners. Rates of inadequacy, unsuitability, or unaffordability are generally lower for seniors 75+ than for the overall household average. Those who rent are more likely to face difficulties. Notably, more than a third of senior renters in ON, BC and AB cannot afford to move into more suitable housing.35 Quebec, comparatively, has lower rates of core housing need than the other provinces, suggesting that a higher proportion of households could afford to move to adequate or suitable housing. This implies that Quebec has fewer affordability challenges relative to the other provinces, particularly for renters and seniors, despite similar levels of inadequate, unsuitable, or unaffordable housing.

As seniors age, it becomes more likely that they will downsize housing to unlock equity and/or move to more appropriate housing. Similarly, they might choose to transition to renting accommodations in seniors’ care spaces. Between 2016 and 2021, 36 percent of over-75 households sold their homes (CMHC 2023).36This rate has declined over time, showing that more and more seniors are remaining independent for longer and choosing to remain in their homes as they age. Older seniors are more likely to transition to rented accommodations (including private market rental units, retirement homes and LTC) and are also more likely to require supportive services. Declining rental rates and a higher proportion of seniors owning their homes shows a preference for aging-in-place and shows that many seniors can maintain their independence for longer than seniors in previous cohorts. Most seniors would prefer to age in their homes, but many are concerned that they won’t be able to afford to do so. Some seniors are pooling their resources and investing in shared accommodation and care services (Sylvestre-Williams 2024).

There are also “naturally occurring retirement communities” when the majority of inhabitants of a multi-unit dwelling are seniors, or seniors choose to purchase housing in close proximity to each other. These naturally occurring communities could provide opportunities to improve the efficiency of home and community care services. They also reveal the preferences for housing and support services of seniors with adequate financial resources to be strategic and plan for their desired retirement. This could provide insights for new models of seniors’ care that reduce costs by supporting the independence of lower-wealth seniors and encouraging seniors with means to contribute to the costs of their support services.

Overall, the data on household spending and income show that the average household is able to afford its needs, although spending patterns change with age and require higher healthcare expenditures. In general, 75+ households have lower spending and consumption than the average household.37 Seniors that have below-median incomes, however, are facing affordability challenges similar to other households in the category, particularly with regard to shelter. These insights suggest two important factors to consider in developing seniors’ care and support policies. First, many senior households have sufficient resources to fund some lifestyle support and healthcare services, meaning there could be opportunities to develop markets for seniors’ support services to supplement the under-provision of publicly provided home care. Second, some seniors are facing affordability challenges, meaning targeted support policies that holistically consider housing, support, and healthcare needs could reduce the likelihood that these seniors will prematurely enter long-term care or become ALC patients in hospitals. For the Silo, Rosalie Wynoch /C.D. Howe Institute.

Clavet, Nicholas-James, Réjean Hébert, Pierre-Carl Michaud, and Julien Navaux. 2022. “The Future of Long-Term Care in Quebec: What Are the Cost Savings from a Realistic Shift toward More Home Care?” Canadian Public Policy 48: 35-50.

Chidwick, Paula, Jill Oliver, Daniel Ball, Christopher Parkes, Terri Lynn Hansen, Francesca Fiumara, Kiki Ferrari et. al. 2017. “Six Change Ideas that Significantly Minimize Alternate Level of Care (ALC) Days in Acute Care Hospitals.” Healthcare Quarterly 20(2): 37-43.

Durante, Stephanie, Ken Fyie, Jennifer Zwicker, and Travis Carpenter. 2023. “Confronting the Alternate Level Care (ALC) Crisis with a Multifaceted Policy Lens.” Briefing Paper. University of Calgary School of Public Policy 16(1). Available at https://journalhosting.ucalgary.ca/index.php/sppp/article/view/76748

Nuernberger, Kim, Steve Atkinson, and Georgina MacDonald. 2018. “Seniors in Transition: Exploring Pathways Across the Care Continuum”. Healthcare Quarterly 21(1): 10-12.

Roblin, Blair, Raisa Deber, Kerry Kuluski, and Michelle Pannor Silver. 2019. “Ontario’s Retirement Homes and Long-term Care Homes: A Comparison of Care Services and Funding Regimes.” Canadian Journal on Aging / La Revue canadienne du vieillissement 38(2): 155–167.

With the retirement of Francesco Totti five years ago, fans had been wondering if his team, Roma, would retire his famous number 10 shirt. In the end, they did not.

That got us thinking, what are the most famous shirt retirements in Soccer – Football history? Let’s take a look.

Due to longer lifespans, governments and employers must reshape approaches to retirement to ensure ageing populations can live fulfilling, healthy lives

New survey indicates shifting views on retirement and stark differences in how younger and older people see their future

World Economic Forum report provides new approaches to retirement that governments, employers and individuals can consider

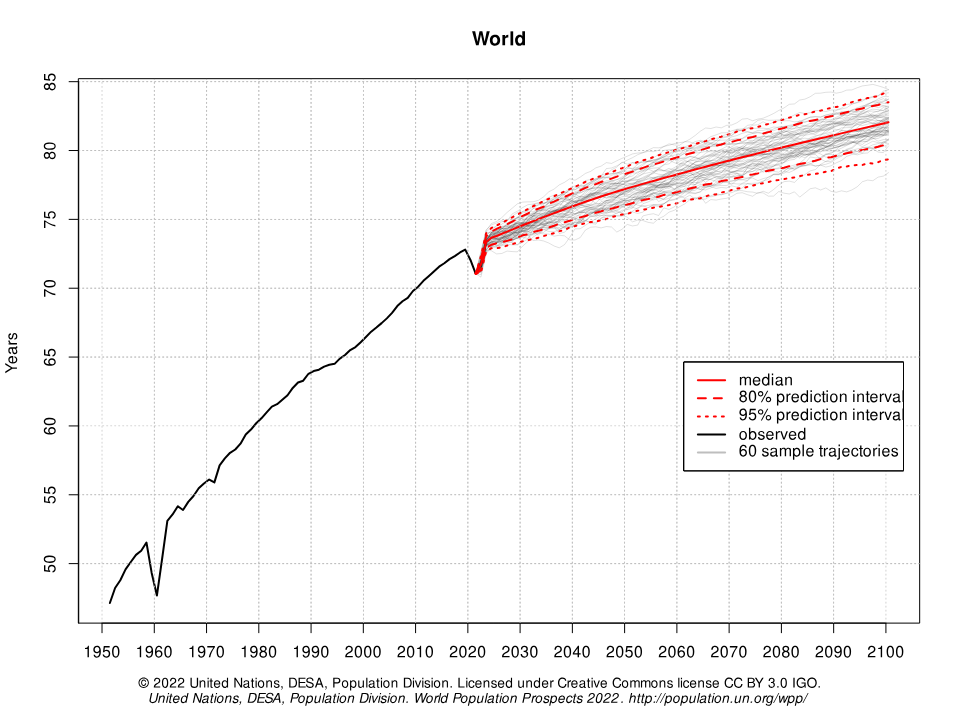

New York, USA, June 2023 – Life expectancy increased from an average of 46 to 73 years between 1950 and 2019 and the United Nations forecasts further increases, estimating that global average life expectancy will reach about 81 years by 2100. Longer lifespans are causing individuals, governments and business leaders to rethink their approach to work and retirement.

Living Longer, Better: Understanding Longevity Literacy, a new World Economic Forum report, in collaboration with Mercer, a business of Marsh McLennan, explores how lengthening lifespans are reshaping how individuals view their working lives and retirement. The report offers recommendations for government and employers to ensure they are adequately supporting people in multiple stages of work and retirement.

The report highlights purpose and quality of life in addition to financial health and resilience – themes that are traditionally associated with retirement planning. It offers options that individuals can consider to ensure they are approaching work, learning and retirement in ways that best meet their needs.

“When it comes to longevity and living longer, healthier lives, everyone has a role on this critical topic,” said Haleh Nazeri, Longevity Lead, World Economic Forum. “How will business support an older workforce and one with growing caregiving needs, what will policymakers do to help all citizens reach retirement equity, and finally, what can individuals do at every life stage to ensure they are able to stay financially resilient in a longer life.”

“Employers are thinking more about the current age distributions within the areas of talent needed to operate their organizations and how to influence the trajectory of these distributions,” said Rich Nuzum, Executive Director, Investments & Global Chief Investment Strategist, Mercer. “To leverage longevity and fight the war for talent effectively, moving from individual roles to team-based roles can help employers take full advantage of the diverse strengths of teams that comprise a combination of older and younger workers.”

Views on Retirement A new survey, Pulse Poll, of almost 400 professionals indicates that women and men view retirement differently. Women, for example, are 55% more likely to say they don’t know if they have saved enough for retirement.

The poll also reveals differences in how younger and older populations view their retirement futures. Both women and those under 40 are more willing to reskill but worry about associated costs. Both groups are also more likely to feel isolated.

Further results from the Pulse Poll can be found below and in the report:

Health is a top concern with two thirds of respondents indicating they expect to have caring responsibilities

Days of “Bank of Mum and Dad” may be reversing; many younger people are likely to have to financially support older family members

Pulse Poll respondents over 40 target lower income replacement levels in retirement

People are generally unaware of how to achieve their target levels of retirement income

More men looking forward to retirement, while more women need to understand their financial situation

Women are 55% more likely to say they don’t know if they have saved enough

Younger people are eight times more likely to use social media for financial advice

44% of under-40s want to retire by 60

Women and younger people are more willing to reskill but are also worried about associated costs

The respondent profiles to the Pulse Poll were homogeneous and predominantly included those who had undertaken higher education, were in more senior positions, were likely to be in employment at major global organizations and with a high level of individual agency and financial literacy.

While there are some sample limitations, the survey suggests how the findings can help start a conversation about the challenges faced and can contribute to the development of solutions for the population this group of respondents represents.

Recommendations for Governments and Employers As people are living longer lives, business and government need to restructure their approach to later life planning. Failing to adopt a multi-stakeholder approach towards longevity will inevitably result in a significant portion of people retiring into poverty. Recommendations are cover three key areas of work and retirement including quality of life, purpose and financial resilience.

Government

Facilitate upskilling of older workers and clamp down on ageism

Provide incentives for employers to offer more robust leave policies for caregiving needs

Explore the wider use of default auto-enrollment and default investment strategies to increase and maximize savings

Establish safety nets such as minimum pension levels provided by government

Enact enabling legislation to make all jobs flexible for longer-life working if desired and to accommodate all life-stage needs

Offer digital skills training and equipment to ensure equitable access to opportunities for all

Employers

Implement programmes offering support such as carers’ leave, information and advice for those who have caregiver responsibilities

Understand what impact the company’s retirement plan design has on the trajectory of retirement-readiness and labour flow – check if people can actually afford to retire

Provide flex-work programmes for caregivers, such as job-shares; allow part-time workers to contribute to defined contribution plans; provide training programmes for workforce re-entry, similar to those for early-career employees

Implement and review financial wellness programmes to:

Cover specific life-stage needs that account for gender, cultural and ethnicity differences

Consider personalized models to show the impact of different working arrangements and retirement ages on pay and pension

Cater to low-income earners who are likely to need the most support saving and planning for retirement

Individuals can also reimagine what their longer lives might look like as the three-stage life of school, work and retirement makes way for a multi-stage life that could include lifelong learning, career breaks and new occupations in later life. This includes pursuing upskilling and reskilling opportunities, as well as prioritizing retirement and pension planning if possible.

Increasing longevity globally will require new innovations and solutions to address how people can stay financially resilient in a retirement that may be 20 years longer than their grandparents. With supportive actions from government and employers, individuals will have a chance to try new approaches to longer lives and reassess how they want to study, live, work, save and retire in ways that are different from what has been done in the past century. For the Silo, Madeleine Hillyer/World Economic Forum.

We work our asses off to buy stuff that we can’t enjoy because we are working our asses off to pay for the stuff we buy while diligently saving (or attempting to save) for our retirement which we keep pushing back because we keep working our asses off to buy yet more stuff to enjoy that we have to work our asses off to pay for, and there is always something else that we want or need or think we need (but really want) that we have to work our asses off to pay for and…

A generation ago somebody coined the phrase “rat race” to describe this phenomenon of modern consumerism, and the term stuck.

It’s wrong.

It ain’t a race.

You can win a race.

Modern consumerist life is a strictly no-win proposition, friends…

… and none of us gets out of here alive.

I began to think about this a few years ago, when I received a matched set of stainless steel rechargeable electric salt and pepper grinders as a gift.

Think about that: Electric salt and pepper grinders.

I am pretty sure this is an answer to a question nobody asked.

This gift made me ponder, and I came to some conclusions:

I must be one of those “hard-to-shop-for” people.

I’d rather have an LCBO gift card.

Grinding pepper over your mashed potatoes is apparently much more strenuous than I ever thought., that somebody decided the world needed this.

A gadget that doesn’t really save any appreciable time or effort and provides little entertainment required somebody to work to earn the money to purchase it.

Enough is enough.

Is mortal- consumerism (yep we just coined that CP) keeping society asleep?

At the time, I was working a gig that required me to work 12 hour days 6-7 days a week, put in 40 000 km a year behind the wheel of a car traveling to meet prospects, 75% of whom either don’t want or can’t afford what I am selling, so that I can afford the next toy/vacation/orthodontist payment/thing with the 50% of my income that the tax man has allowed me to keep. I was alienated from, and alienating, my kids, my wife, because of my absence from home life, and I became an overcompensating asshole for the same reason which increased the tension and…

…any of you out there who have climbed out of the wreckage of a crashed marriage know exactly where I’m coming from.

Actually, scratch that vacation part. At the time I hadn’t taken more than a long weekend off in over a decade.

And I thought I was successful.

I began to question where I was going, what I was doing, and why.

Frankly, I figured enjoying retirement is a myth.

That whole “Freedom 55” thing? Bullshit.

First, you gotta get there. With my diet, hours, stress level and number of miles driven every year, the odds were good I wasn’t gonna make it.

Second, you gotta pay for it. You need to keep squirreling away the cash, tending your investments, watching your nest egg grow, deferring and sacrificing today for the dream of a better tomorrow…

….As long as the market doesn’t tank, your health holds up, property values don’t plummet, or your kids don’t move back in, with their kids.

Money may not buy happiness, but always feeling like you don’t have enough will make you bitchy as hell.

I was sitting in the cockpit of our old, small, paid-for sailboat one morning, enjoying a cup of coffee when it hit me:

As a society we are conditioned to approach life like a big twin-engine cabin cruiser- heavy consumption, lots of noise, lots of flash, throwing a big wake. Unless you are getting noticed, you’re not succeeding.

I finally figured out that there is a lot to be said for living a NO wake lifestyle.

But how?

With a bit of soul searching we realized we had to quit confusing our wants with our needs.

My wife and I realized that we were perfectly content spending time on our old, small, paid-off boat in our low-cost slip on our no-frills dock. We didn’t need a bigger boat on a fancier dock.

And we didn’t need new cars. As long as the old cars keep running , it is always gonna be cheaper to fix ‘em than replace ‘em. If I need a new whip to impress you, you’re likely not worth impressing.

Besides, there’s something real liberating about parking wherever you damn well please, because dings and scratches just don’t matter.

And we didn’t need a $20 000 kitchen reno or a $10 000 bathroom makeover. Or a bigger house. Or a bigger garage.

Or a bigger mortgage.

For a longer time.

With fatter payments.

We didn’t need to stand in line to be grilled by a soul-patch sporting “barista” first thing in the morning just to get a simple cup of coffee which costs as much as a Happy Meal, when we had a perfectly good underused coffee maker on the kitchen counter.

We needed to live life NOW, on OUR terms.

A funny thing happened. By deciding what we could live without, we could now afford to live.

With less financial stress, I didn’t need to be on the road, living out of a car and fueling up on fast food three meals a day. My wife and I discovered that cooking dinner together was a great way to re-connect at the end of the workday. Chopping, sautéing, stirring with a glass of wine while recapping our respective days beats the hell out of eating a Whopper an hour from home.

We didn’t have to save dining at restaurants with tablecloths for a special occasion to fit the budget.

We could afford to drink the bottles of wine we could only read about before.

We could take vacation days without figuring out what we had to sacrifice to make up for the lost wages.

Hell, we could take whole damn vacations, for that matter!

The sunsets look just as pretty from a small, paid-off sailboat as it does from the bridge of a six-figure cabin cruiser.

The rum goes down just as well.

And I can enjoy it instead of working to afford it.

Life insurance is commonly regarded as an investment that should be considered much later in life, when you are older. Young investors frequently favor high-risk, high-reward investments such as equities and commodities. Even the most conservative millennials prefer investments such as fixed deposits or debt mutual funds. Insurance is being replaced by investment options that promise greater monetary returns sooner.

However, the fact remains that investing in life insurance early has numerous benefits.

You’ll understand why investing in life insurance plans early in your career should be an important part of your retirement planning once you’ve learned the benefits. So, here are 3 of the many benefits of purchasing a life insurance policy at a young age.

You will pay lower premiums

Purchasing life insurance at a young age can save you money in the long run. The insurer frequently considers factors such as the applicant’s age and general health condition when determining the premium payable. People in their twenties and thirties are generally in better health.

As a result, premium charges are less expensive than those charged to older investors. Another reason why buying life insurance at a young age is less expensive is that your risk of dying is much lower. To take advantage of this provision, it is best to purchase life insurance early in life.

Your money has enough time to grow

When you purchase a life insurance policy at a young age, your money has more time to grow. As a result, investing in your twenties increases the death or maturity benefits payable at the end of the policy’s term.

For example, if you purchase a life insurance policy at the age of 25 and continue to pay premiums until you are 60, your money will have 35 years to accumulate into a retirement corpus. If you buy the same life insurance at 40, you only have 20 years to make your money grow. Investing early can thus increase your investment’s cash value in the long run.

The future of your family is secure

Most people, by the time they reach retirement age, will have amassed a sizable corpus to help keep their family financially secure. Most people’s children would have graduated from high school or have a job by the age of 50 or 60. When you’re younger and just starting out in your career, your family may be in a more vulnerable position.

In the unfortunate event that you die, your spouse and young children will struggle to cope without a financial safety net. Investing in a life insurance policy at a young age can provide your dependents with this benefit.

As you can see, investing in life insurance at a young age can be a really big deal if you want to save money in the long run. It will also protect you and your dependents no matter what if you had to die unexpectedly. If you need any advice, you should contact a professional that will help you choose the right life insurance according to your needs.