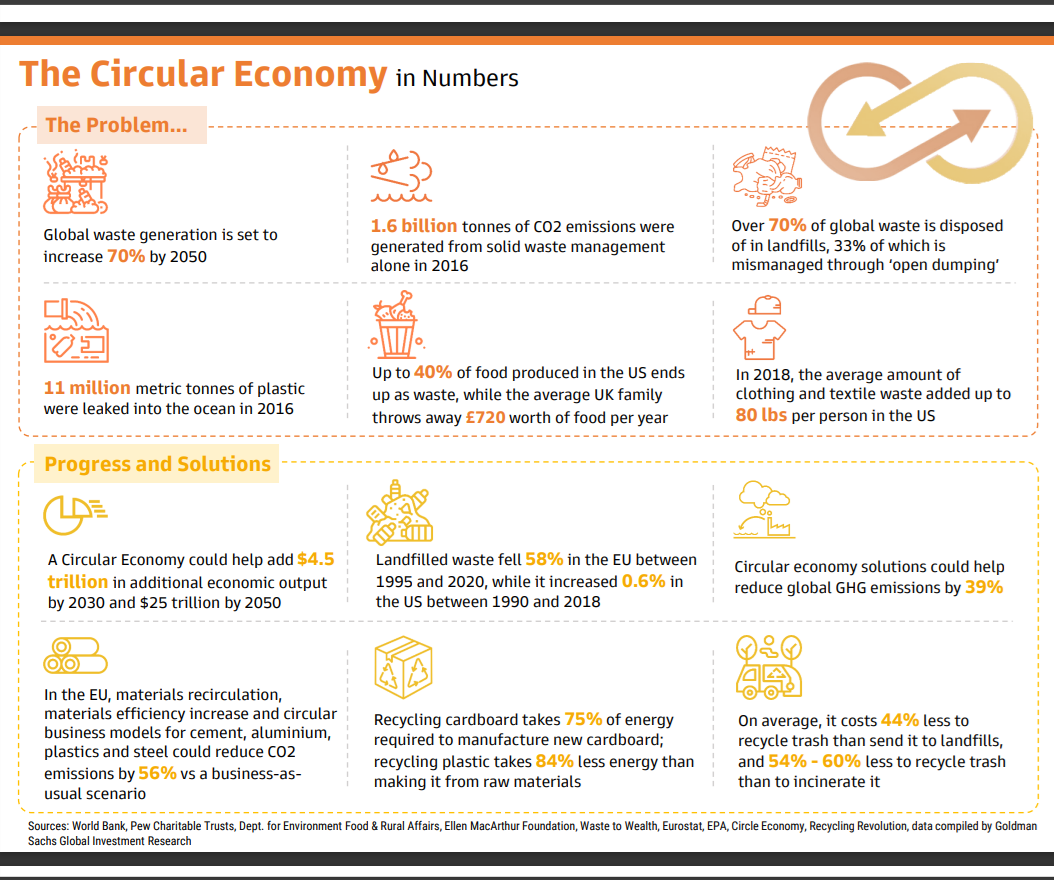

With the “circular economy” spurring a seismic shift toward sustainability and resource efficiency across sectors, industries are redefining themselves by transforming waste into lasting value. With projections of up to $4.5 trillion usd/ $6.4 trillion cad in economic benefits by 2030, companies are rethinking traditional models to protect the environment, cater to green consumerism mindsets and boost financial performance. At the forefront of this movement in the fine jewelry category is Sonalore, an innovative eTailer turning gold jewelry into a smart, sustainable investment amid its lifetime buyback guarantee. Sonalore not only ensures that every piece of 18-karat gold jewelry endures as a valuable asset, but also champions a closed-loop system that minimizes waste and preserves natural resources as detailed below.

Gold Into Green Investments

A seismic “circular economy” shift is happening across industries, as businesses rush to minimize waste and maximize resource value. This transformation isn’t just about sustainability—it’s about creating smarter business models that benefit both customers and the environment. So impactful this approach, Goldman Sachs projects the circular economy could deliver up to $4.5 trillion in economic benefits by 2030. Companies across sectors are citing how they’re “shaking things up” to waste less—and reap the financial benefits in the process. Geopolitics are also fostering this approach, as Goldman Sachs further asserts that “operating in this way could become ‘critical’ in the face of the rising cost of raw materials” among other drivers.

One innovative eTailer—Sonalore—is leading this change in fine jewelry, transforming how people buy, wear and sell their gold pieces. The company’s approach turns traditional gold jewelry from a depreciating purchase into a liquid investment, while naturally promoting sustainability. Its “lifetime buyback guarantee” program not only transforms its wares into bona fide commodity investments for consumers, but also ensures its products can be easily recycled and reborn.

“We sell 18-karat gold jewelry from the perspective of it being a sound investment—not an expense—that enduringly holds its value,” said Sonalore CEO Nidhi Singhvi. “Our buyback promise allows consumers to sell back their items at a fair current price valuation of gold, which has the potential to increase beyond the purchase price of the item. Gold is, after all, a heralded investment commodity amid its historically proven performance in various economic environments.”

In doing so, the company is also fostering circular economy principles. Here are three ways Sonalore is reshaping the industry:

1. Sustainability That Makes Business Sense –

Most sustainable initiatives ask you to pay more for less. Sonalore flips this on its head. When you’re done with a jewelry piece, they buy it back at market rates and recycle the gold into fresh designs. No more jewelry gathering dust, no unnecessary mining, and you get real value back. It’s sustainability that puts money in your pocket, not the other way around. This isn’t just good for the environment, it is plain smart business. The closed loop system reduces dependency on mining while preserving metal value. Sonalore’s market-rate buyback makes sustainability financially rewarding.

2. True Value, Finally Unlocked –

For a circular economy to work, you need a product with intrinsic value at the center. Fine jewelry should be a very good natural candidate for a circular economy. However, traditional retail markups of 3-5x have broken this cycle, trapping customers in a cycle of overpaying and undervaluing. Sonalore strips away artificial markups, showing customers exactly what they’re paying for – from metal content to craftsmanship. When gold prices rise, so does the value of your piece. This transparency extends beyond purchase – customers can track their jewelry’s value in real-time, treating each piece as the investment it should be.

3. Freedom to Change your Mind –

Life changes, and your jewelry should too. Most fine jewelry sits unworn, losing value in drawers or becoming a guilt-inducing reminder of money spent. Sonalore’s lifetime buyback guarantee transforms this dynamic. Want to switch styles? Trade up. Need liquidity? Convert to cash at market rates. Moving abroad? Downsize without loss. This flexibility turns jewelry from a static purchase into a dynamic asset that adapts to your life changes.

In today’s hugely competitive jewelry marketplace, Sonalore is reimagining not just how jewelry is sold, but also how it creates lasting value. By combining transparent pricing, investment potential and environmental responsibility, the company proves that luxury retail can evolve to meet modern demands for both sustainability and smart value.

As the circular economy gains momentum across industries, Sonalore’s innovative model shows how businesses can transform traditional products into dynamic assets that benefit customers, companies and the environment, alike. For the Silo, Karen Hayhurst.