Secretary of State Marco Rubio at President Trump’s Roundtable on American Mining

SECRETARY RUBIO: Thank you, Mr. President. Thank you for coming to the State Department. We like this room a lot, too, and obviously don’t look back; there’s a painting up here. Just don’t – (laughter) – uh-oh.

PRESIDENT TRUMP: (Inaudible.) That’s a good one. (Laughter.) I’m taking it with me.

SECRETARY RUBIO: That – I shouldn’t have said anything. But anyway, Mr. President, thank you for being here. Thank you for your leadership on this topic. It’s a challenge we face in this domain that actually goes to the very survival of the country, and thank you for giving it a priority in your presidency. This has been going on for 25 years. We’ve been walking away from the importance of this, and now we’re trying to make up for 25 or 30 years of mistakes under your presidency. So, we appreciate your presidency valuing this when other presidents did not.

The group of people that are here today represent the whole-of-nation effort that’s involved in this. It’s – because at the core of this is our industrial strength, but also our national sovereignty – that we never depend on other countries for things we need to prosper and to defend ourselves as a people. And so, you’ll see here today, as you’ve already pointed out, we have leaders not just from government but from universities, from private industry, from students who are going to be the future of this industry.

I wanted to briefly – very briefly – touch on what the State Department’s done. Earlier this year we had a Critical Minerals Ministerial. We brought in countries from all over the world to – and announced the creation of something called FORGE, which is an international partnership chaired by us in the United States to leverage public finance and coordinate diplomatic support to secure these supply chains around the world. At that meeting, we signed 11 new critical minerals agreements with countries, adding to the ones that already existed. Today, under your administration, we’ve already signed 27 critical mineral agreements with other countries.

Pax Silica

We also, under the leadership of someone who needs to be recognized, our Under Secretary Jacob Helberg – I don’t know if Jacob is here, but Jacob has been phenomenal. He came up with something called Pax Silica, and it’s an initiative that leads our efforts to partner with the private sector and invest in mining and refining and in processing as well as the end-use applications of that.

There’s still a lot of work left to do, but we at the State Department are willing to utilize our unmatched global presence, our presence all over the world, to ensure that we’re working on this. And we’re committed to working with industry, with universities, with all the elements of our national power to bring this about. And so, thank you, Mr. President, for prioritizing this, and I think we all look forward to working not just nationally but with our allies around the world to ensure that we have supply chains that are diversified and reliable and no country can ever hold this over our head and threaten us in the future. Thank you.

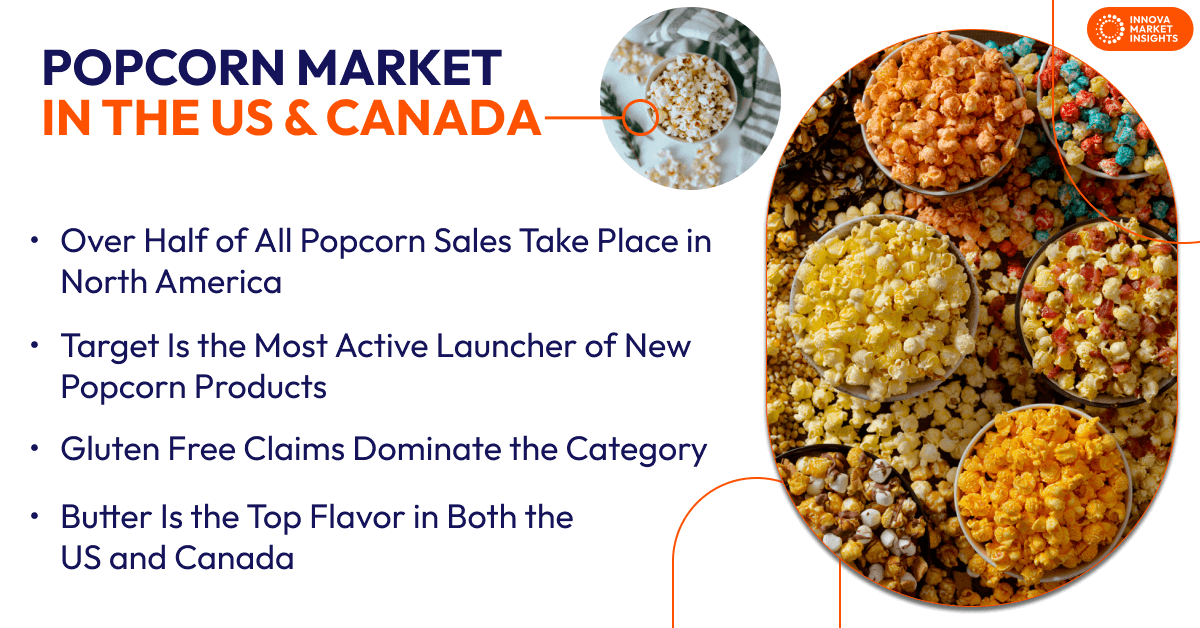

Evidence of popped corn discovered in Peru shows people’s love affair with the light and fluffy snack dates back 6,700 years. But if you’ve enjoyed popcorn in more recent times, it likely came from the United States.

While estimates vary, U.S. popcorn production accounts for upward of 80% of popcorn seed sold worldwide. Much of it comes from the Midwest, the heartland region where the world’s first popcorn popper debuted at the World’s Columbian Exposition in Chicago in 1893.

Scientifically Adapted Popcorn

For decades, U.S. seed scientists have adapted popcorn to thrive in the agriculturally rich region, helping drive the snack’s evolution from a movie theater and TV-night favorite to a healthy snack enjoyed around the world.

Dan Quinn, corn program director at Purdue University in West Lafayette, Indiana, says years of localized breeding and fertilization techniques have increased farmers’ popcorn yields and developed traits for optimal popping.

Why Different Corn Hybrids Make Sense

Different hybrids have been developed for microwave popping versus large commercial kettles, Quinn says. Research considers everything from moisture levels to hull thickness (the part of the seed that explodes during cooking) and focuses on both major popcorn shapes: butterfly and mushroom.

Which State Is Producing The Most Popcorn?

Indiana now produces 40% of America’s popcorn, more than any other U.S. state. Indiana and Purdue’s rich popcorn legacy includes Orville Redenbacher, the bow-tie-clad pitchman who refined his kernels at Purdue before launching his business from the state. He later popularized his brand with TV commercials in the 1970s and 1980s.

A few states over, in Nebraska, researchers are enhancing popcorn’s inherent nutritional qualities. The University of Nebraska and private sector partners recently developed a popcorn variety rich in an amino acid essential for healthy diets, says David Holding , a professor and researcher at the school. “This is a product that lends itself to organic production and can be marketed as a novel popcorn variety,” he says.

Aaron Whalen, sales manager at Ag Alumni Seed, which partners with Purdue University and growers in 20 countries, says the popcorn market is trending toward healthier products, as well as those that allow for adding culturally specific flavors.

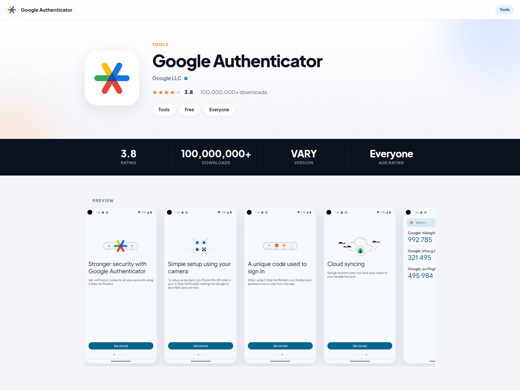

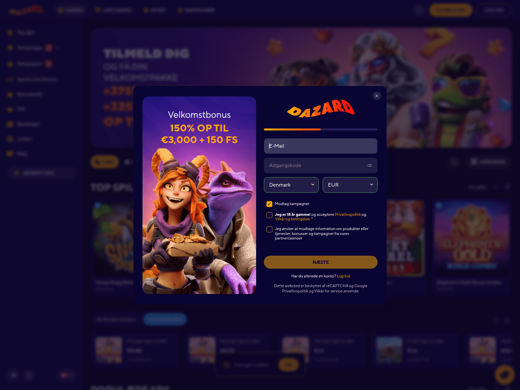

Our friends at NordVPN’s Threat Intelligence team has just uncovered a criminal network running paid Facebook and Instagram ads that impersonate over 400 trusted brands — from Google Authenticator and Kalshi to national lotteries — to trick people into fake app installs that redirect them to unlicensed online casinos.

The operation is not the work of a lone scammer.

It is a rented criminal platform, actively running today, used by roughly a thousand affiliates across more than 250 teams. This large-scale criminal operation hijacks the logos and names of over 400 trusted brands to redirect unsuspecting people toward unregulated online gambling. The network — which NordVPN tracks as pwa_betterlinks — runs paid adverts on Facebook and Instagram impersonating household names including Google Authenticator, Kalshi, Disney+, Duolingo, Delta Air Lines, and national lotteries.

Victims who tap the ad are shown a fake Google Play Store page that is nearly impossible to distinguish from the real thing. One tap of “Install” later, they land on an unlicensed casino asking for a deposit. What a real, targeted person sees: The full fake Google Play page — here spoofing Crown Melbourne

“What we’re looking at is essentially trust laundering. Criminals take the credibility that legitimate companies have spent years building and redirect it toward their own ends. By the time a victim realizes something is wrong, they’ve already deposited money into a casino they’ve never heard of.” Marijus Briedis, chief technology officer at NordVPN.

The fake app store hiding inside a social media ad

Every victim’s journey starts with a paid ad on Facebook or Instagram. A real, purchased placement that carries the implicit legitimacy of a platform people use every day. Clicking it takes users to what appears to be a genuine Google Play Store listing, complete with the brand’s logo, a forged developer name, a 4.9-star rating, and thousands of fabricated reviews. The only visible tell is the web address in the browser bar — a random throwaway domain rather than play.google.com. Google Authenticator spoofed on playrosario[.]site (Google LLC · Tools)

The impersonated brands span casinos and national lotteries (Crown Melbourne, Holland Casino, EuroMillions), mainstream apps (Google Translate, Google Authenticator, YouTube Kids, Adobe Acrobat, Shazam), financial services (Capital One, Credit Karma, Kalshi), streaming (HBO Max, Disney+, Peacock), and travel (Delta, United, Airbnb).

The Install button that installs nothing

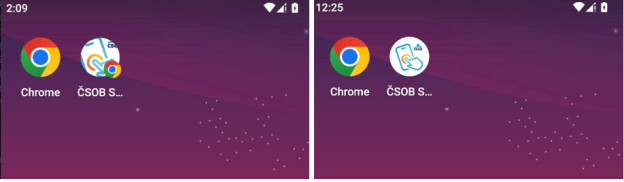

Tapping Install triggers a convincing fake progress bar. No app is downloaded. What actually happens is a shortcut — a Progressive Web App, or PWA — is silently added to the home screen under the impersonated brand’s name and icon. A PWA is not a real app. It is a website that looks like one, sitting on a phone’s home screen with zero app store vetting required. The criminal can spin up a new fake page as fast as they can register a domain. On the left PWA “Installation” on Android, on the right Official app installation. The process also silently signs the device up for push notifications, which fire gambling reminders directly to the lock screen and are deliberately difficult to disable. Even the back button is rigged. Instead of returning users to the previous page, it reroutes them to the casino offer.

A commercial product designed to evade detection

Before any real page is shown, every click passes through a cloaking layer that checks whether the visitor is a human or an automated scanner — including Facebook’s own ad review bots. Checkers are served a blank decoy page. Real users are served the fake casino funnel. Across NordVPN’s captured dataset, the casino page was served 7,261 times; the decoy was served to checkers 3,153 times. The people doing the checking never see what the actual targets see. The network is structured as a commercial product, not a one-off scam. At the top sits betterlinks[.]pro, a platform that markets itself openly as a “PWA constructor for affiliates” with built-in cloaking and Facebook optimization. Unlicensed casino registration with an offering of 150% up to €3,000/ $4,830 CAD + 150 FS dazard[.]com

In the middle sit roughly a thousand affiliate accounts across more than 250 teams who rent the kit and buy social media traffic to run campaigns. At the bottom are the unlicensed casinos and CPA networks that pay the affiliates a commission for every user who registers or deposits — with captured records linking the operation to the Makeberry Affiliates network and casinos.

How to stay safe?

Marijus Briedis advises anyone using social media to keep three things in mind: A real app install always opens the official store. If tapping “Install” in an ad opens a web page rather than the Google Play Store or Apple App Store, stop immediately. Check the address bar. A genuine Google Play listing lives at play.google.com. Any other web address showing a store-style page — no matter how accurate the branding — is a fake. Review your push notification permissions. Go to your phone’s settings and check which websites have permission to send you alerts. Revoke anything you don’t recognize.

Methodology

The investigation began by identifying a shared template fingerprint across a cluster of fake app-store pages, which NordVPN used to recover live instances of the operation at scale. From there, analysts mapped the full funnel logic through network traffic analysis and JavaScript deobfuscation, revealing the infrastructure connecting individual affiliate accounts to their campaigns, destination casinos, and real Facebook Business ad pixels. Domain registration records, hosting provider data, and code-level signals — including language markers in the push notification code — were used to support operator attribution. All indicators of compromise are analyzed in machine-readable format (STIX 2.1, 880 indicators). Conclusions are based on verified data, with the perimeter of the identified systems delimited with the maximum possible accuracy.

August 6, 2026 – As Canada ramps up defence and infrastructure spending, federal policymakers are facing growing pressure to make difficult decisions about other areas of government spending. Yet Ottawa’s evaluation system provides too little evidence to identify which programs deliver the greatest value for Canadians, according to a new C.D. Howe Institute report.In “Putting Programs to the Test: Strengthening the Federal Evaluation Function,” authors John Lester and Benoît Robidoux argue that the current federal evaluation framework falls short because it does not explicitly require value for money assessments, gives departments too much flexibility in how they measure efficiency, and lacks the data, expertise and institutional incentives needed to produce evaluations that can guide spending decisions. The report outlines practical reforms to strengthen the federal evaluation function, improve evaluation quality and consistency, and provide policymakers with better evidence for allocating public resources.

6 août 2026 – Alors que le Canada accroît ses dépenses en matière de défense et d’infrastructures, les décideurs fédéraux subissent des pressions croissantes pour prendre des décisions difficiles concernant d’autres postes de dépenses publiques. Or, le système d’évaluation d’Ottawa fournit trop peu de données probantes pour déterminer quels programmes offrent la plus grande valeur aux Canadiens, selon un nouveau rapport de l’Institut C.D. Howe.

Dans « Putting Programs to the Test: Strengthening the Federal Evaluation Function », les auteurs John Lester et Benoît Robidoux soutiennent que le cadre d’évaluation fédéral actuel présente des lacunes. Il n’exige pas explicitement d’évaluation de l’optimisation des ressources, il accorde aux ministères une trop grande latitude quant à la façon de mesurer l’efficience, et il ne dispose pas des données, de l’expertise ou des incitatifs institutionnels nécessaires pour produire des évaluations susceptibles d’orienter les décisions en matière de dépenses. Le rapport propose des réformes concrètes pour renforcer les évaluations au niveau fédérale telles qu’améliorer la qualité et la cohérence des évaluations, et fournir aux décideurs des données probantes de meilleure qualité pour l’affectation des ressources publiques.

Drawing on presentations and discussions from the C.D. Howe Institute’s 2026 Workshop on Strengthening the Federal Evaluation Function, the report recommends making value for money assessments a mandatory part of federal program evaluations, based on rigorous benefit-cost and cost-effectiveness analysis where appropriate. It also proposes creating an independent evaluator general to help departments build evaluation capacity and improve the consistency and quality of federal evaluations.

“Governments shouldn’t simply ask whether a program achieves its objectives. They also need to know whether it delivers enough public benefit to justify the resources devoted to it,” says Robidoux, former Senior Associate Deputy Minister at Employment and Social Development Canada. “When fiscal pressures intensify, stronger value for money evaluations give decision-makers better evidence to determine where each additional taxpayer dollar can have the greatest impact.”

The report also recommends expanding the evaluation framework to include spending delivered through the tax system, incorporating a value for money test earlier in the approval process for new programs, making greater use of linked administrative data, and replacing the rigid five-year evaluation cycle with a more flexible approach when programs have already been thoroughly assessed and remain largely unchanged.

“Too often, federal evaluations focus on how program participants are impacted – without identifying the program’s contribution to these outcomes – rather than on whether programs provide value for money when all benefits and costs are accounted for,” says Lester, Fellow-in-Residence, C.D. Howe Institute. “Policymakers also need to know whether a program delivers enough value to justify the tax dollars required to fund it. Stronger evidence will help them make better spending decisions.”

Ottawa describes its overall expenditure management system as “designed to ensure that all programs are focused on results, provide value for taxpayers’ money and are aligned with the government’s priorities and responsibilities.”

Making value for money evaluations of programs mandatory while allowing time to build capacity, appointing an evaluator general, and broadening the scope of the evaluation policy would be big steps toward making this worthy goal a reality, conclude the authors.

For more information, contact: John Lester, Fellow-in-Residence, C.D. Howe Institute; Benoit Robidoux, former Senior Associate Deputy Minister, Employment and Social Development Canada; and Lauren Malyk, Manager, Communications, C.D. Howe Institute, 416-873-6168, [email protected].

The C.D. Howe Institute is an independent not-for-profit research institute whose mission is to raise living standards by fostering economically sound public policies. Widely considered to be Canada’s most influential think tank, the Institute is a trusted source of essential policy intelligence, distinguished by research that is nonpartisan, evidence-based and subject to definitive expert review.

California’s most enduring export isn’t film or technology, but the promise of a better version of yourself.

For decades, the Golden State has cultivated an image of health, vitality, and self-improvement, where surfing, hiking, yoga, organic food, luxury spas, and holistic living have become part of a globally recognized lifestyle. From Malibu wellness retreats to Beverly Hills longevity clinics, the pursuit of physical and mental well-being has evolved from a trend into a defining element of California culture. That philosophy of healthy living has steadily reshaped luxury real estate, where buyers increasingly expect homes to function as private retreats rather than simply places to live. Magnum Opus, a newly completed estate in Hidden Hills, reflects that shift, combining resort-caliber wellness amenities with architecture designed to blur the boundary between home and nature. The stunning residence has been listed for $21 million usd/ $29.51 million cad.

Organic Aesthetic

Set behind the gates of Hidden Hills on nearly two acres, the newly built seven-bedroom estate spans 13,832 square feet, including 11,231 square feet of interior living space. Designed by architect Ron Heston with interiors by Alison Gordon, the residence embraces an organic contemporary aesthetic defined by soaring vaulted ceilings, walls of glass, white oak, natural stone, and warm hardwood floors. Mature trees and mountain views provide a tranquil backdrop, while sliding glass doors dissolve the distinction between indoors and outdoors. The formal living room centers on a sculptural stone fireplace framed by exposed oak beams and oversized picture windows, while the expansive great room flows seamlessly onto a covered veranda connecting the home’s theater, fitness studio, spa, and outdoor entertaining spaces.

The commitment to well-being continues throughout the residence. A dedicated wellness wing features an infrared sauna, steam room, and cold plunge worthy of a five-star spa. Upstairs, the primary suite offers a peaceful escape with a covered terrace overlooking the mountains. A marble fireplace, custom white oak cabinetry, and a luxurious natural stone bath complete with a steam shower, freestanding soaking tub, dual water closets, and a boutique-style dressing room transform the space into a sanctuary designed for both restoration and relaxation

The grounds are equally impressive.

Surrounded by lush landscaping, mature trees, and sweeping lawns, the estate features a resort-style pool with dual sun shelves, an infinity-edge spa cascading over a marble waterfall, and a covered pavilion equipped with an outdoor kitchen, dining area, full-service bar, and retractable entertainment screen. Every element has been thoughtfully positioned to frame the surrounding landscape, reinforcing the home’s seamless connection to nature. A showroom-quality four-car garage completes the property, providing refined accommodations for a prized automobile collection.

Located within the exclusive guard-gated enclave of Hidden Hills, the estate enjoys one of Southern California’s most coveted addresses. Celebrated for its equestrian trails, oversized lots, and peaceful, semi-rural setting just minutes from Los Angeles, the community has long attracted high-profile residents seeking privacy without sacrificing convenience. Some famous residents include Kim Kardashian, Drake, Jessica Simpson, The Weeknd, and Madonna.

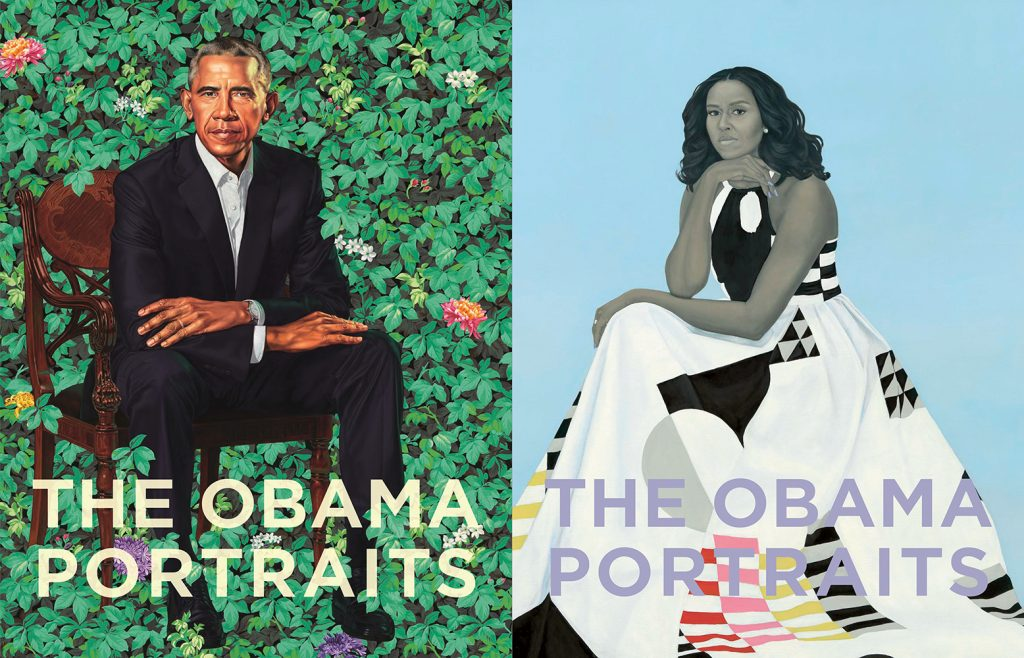

Amy Sherald is a celebrated contemporary painter whose portraiture has redefined the visual language of North American realism by centering the everyday lives and experiences of Black Americans. Born in Columbus, Georgia, and now based in the New York area, Sherald is best known for her luminous, large scale paintings that combine grayscale skin tones with vibrant color to create striking, psychologically rich portraits.

Her groundbreaking practice has earned international recognition, including the 2016 Outwin Boochever Portrait Competition from the Smithsonian’s National Portrait Gallery and the commission to paint the official portrait of former First Lady Michelle Obama.

Sherald’s work explores identity, representation, and the complexity of Black life through carefully composed images that celebrate dignity, individuality, and imagination. Her paintings have been exhibited at leading museums around the world and are held in major public and private collections, solidifying her place as one of the most influential artists of her generation.

Through portraits that invite reflection and challenge conventional narratives, Sherald continues to expand conversations about race, history, and the power of seeing oneself represented in art.

Her acclaimed mid-career retrospective, Amy Sherald: American Sublime, is currently on view at the High Museum in Atlanta through September 27, 2026. The High is the fourth and final venue for this exhibition.

Featured image- Amy Sherald with her painting A God Blessed Land at her SFMOMA solo show “American Sublime.” Photo by Kelvin Bulluck, courtesy of SFMOMA.

Call & Response

I can’t believe a year has come and gone.

On July 1 of last year, I returned to Atlanta to lead the National Black Arts Festival. It was a significant homecoming, not only because I would be leading one of the nation’s iconic Black cultural institutions, but because NBAF is where my professional journey in Black arts and culture began. Like my first season directing the organization’s artistic programming in 2005-2006, this past year has been one of the most challenging, rewarding, and inspiring of my career.

When I accepted this role, I set three goals for the next decade: build a sustainable organization with a thoughtful succession plan, secure a permanent home for NBAF, and bring back the summer festival. Those goals remain, but over the past year they have evolved into something even greater.

Over the last twelve months, we’ve focused on strengthening the foundation of NBAF, and that work continues. We’ve reinforced our infrastructure, renewed relationships with funders, community leaders, longtime supporters, local and national artists, and colleagues across the cultural sector. We’ve reorganized our team and spent countless hours listening, learning, and imagining what this institution can and should become.

While we are very present in the realities of today, we are equally focused on building an institution that will outlive us all. One that preserves Black cultural memory, invests in artists, and creates opportunities for young people. One that convenes courageous conversations and interrogates culture. One that strengthens communities and ensures Black art and culture continue to shape the future rather than simply respond to it.

Quite frankly, this work has never been more important.

Let’s name what many of us already know. We are living through a moment in which Black history, Black institutions, and Black culture have become political. Federal support for the arts has been reduced. Organizations across the country are losing funding. For institutions like NBAF, even having the word Black in our name has become a barrier in rooms where it once represented an opportunity. That reality should concern all of us.

Culture has always been one of the first places where societies negotiate who belongs, whose stories matter, and who gets to author the future. We remain deeply grateful to the foundations, corporations, and individual donors who support us. Their investment in cultural continuity and in institutions that safeguard our collective memory are shaping the future.

The months between now and the end of the year will be pivotal. The support we receive will determine the pace in which we build the infrastructure our mission requires and how boldly we move toward the next chapter of NBAF. As we prepare for the return of our summer festival, every investment made today strengthens our ability to serve artists, audiences, and communities tomorrow.

If you’ve ever wondered how you can make a difference, this is your moment. Visit nbaf.org to make a gift, join the Collector’s Guild, purchase your ticket to Fall For Brunch, explore sponsorship opportunities for the return of the 2027 National Black Arts Festival or become a Volunteer.

Thank you for believing in this work. Thank you for showing up. Thank you for investing in an institution that exists to preserve our cultural memory, amplify Black creativity, and ensure that Black narratives continue to be authored by Black voices.

Sincerely,

Leatrice Ellzy, President & CEO National Black Arts Festival

Spring means fresh flowers and sunny days, but it also brings seasonal health issues as the weather gets warmer: from Rosacea to Lyme disease.

Most likely, you or someone you know has been affected by Lyme disease, the most common tick-borne illness in North America with more than 300,000 cases diagnosed each year. In a timely new book, Conquering Lyme Disease(Columbia University Press), Columbia University Medical Center physicians Brian A. Fallon and Jennifer Sotsky reveal that despite the challenges to find a cure for this complex, debilitating disease, precision medicine and biotechnology are accelerating the discovery of new tools with which doctors will be able to diagnose it and treat patients.

“Through rapid genetic sequencing, scientists can identify many different strains of Borrelia burgdorferi as well as new tick-borne microbial infections, such as Borrelia miyamotoi, Borrelia mayonii, and the Heartland virus.” — Brian Fallon

Could groundbreaking technologies that rapidly increase our understanding and open up new pathways mean a cure for Lyme disease one day soon? The Global Search for Education is pleased to welcome Dr. Brian Fallon to find out how tech is tackling the ticks.

“Modern technology using Next-Generation Sequencing (NGS) allows one to discover with great rapidity all microbes that may be present within a sample of fluid.” — Brian Fallon

Brian, how has technology improved the research process for tick borne diseases?

Consider the difference in price of genome sequencing between 20 years ago and today. In 2003, it had taken the Human Genome Project about 4 years and costs estimated between $500 million to 1 billion…by 2006 the cost for sequencing a single human genome had dropped to 14 million……today a whole human genome can be sequenced within days for less than $1,000. This is a tremendous advance.

Why is genome sequencing so important? Let’s look at human tick-borne diseases. When two different people are infected with Borrelia burgdorferi (the microbe that causes Lyme disease), one will resolve the disease quickly after a course of antibiotics while the other may develop a chronic relapsing remitting illness. Why? Because one person might have gotten a more persistent strain, while the other received a less invasive strain that stays localized to the skin. Additionally, the genetic differences in the human determines how the immune system responds to the invading microbe. Understanding the genetics of the infection and of the human host allows scientists to unravel the mysteries of tick-borne illnesses.

Through rapid genetic sequencing, scientists can identify many different strains of Borrelia burgdorferi as well as new tick-borne microbial infections, such as Borrelia miyamotoi, Borrelia mayonii, and the Heartland virus. When the genome of a microbe is sequenced, it provides a starting point for the study of pathogenesis, vaccine development, and treatment. Discovery of these new microbes inside ticks has been enormously helpful. A patient who has had typical symptoms of Lyme disease after a tick bite but has tested negative on the blood tests for Lyme disease might puzzle clinicians. They may criticize the insensitivity of the Lyme disease tests. However, when this same patient is tested for the newly discovered tick-borne infection, Borrelia miyamotoi, the diagnosis is then clear. Yes, the patient had a Lyme-like illness, but it wasn’t Lyme disease: it was Borrelia Miyamotoi disease.

Modern technology using Next-Generation Sequencing (NGS) allows one to discover with great rapidity all microbes that may be present within a sample of fluid. This “discovery based” approach using “unbiased next generation sequencing” enabled a 14 year old boy to be rescued from a fatal infection within 48 hours (Wilson et al, NEJM, 2014). This boy had endured 3 hospitalizations over 4 months, had over 100 diagnostic tests, spent 44 days in an ICU for encephalitis of unknown etiology, had a brain biopsy, and had to be put into a medically induced coma to prevent damage from his ongoing seizures.

Eventually Dr. Charles Chiu at U.C.S.F. employed NGS analysis of more than 8 million sequences with a bioinformatics pipeline (SURPI) for the detection of all known pathogens. The cause of the boy’s meningoencephalitis was revealed as Leptospira santarosai. He had likely acquired it in Puerto Rico, as it is not present in the continental United States. He received the appropriate antibiotics and was discharged 2 weeks later to rehab. This same approach is especially useful for uncommon infections as they might not be suspected; for example, rare tick-borne viruses such as Powassan Virus or Heartland Virus can be rapidly detected using this discovery approach.

DNA Double Helix

How has big data impacted the way advocacy groups support research?

A patient-generated source of Big Data is LymeDisease.org. This California based organization developed a survey called “My Lyme Data” that patients could fill out on the web about their clinical history and lab tests and treatments. In a short period of time, they had data on 10,000 patients whom they track over time. With this information, they provide a more comprehensive clinical view of the bulk of patients who are diagnosed with persistent symptoms despite treatment for Lyme Disease (aka Chronic Lyme Disease).

“In geographic areas where medical professionals are scarce, AI technologies will play an increasing role in improving patient care by allowing differential diagnoses to be generated and treatment options suggested through AI-based systems accessed through the internet.” — Brian Fallon

Jobs in all professions are being automated. Do you believe AI technologies will only assist doctors or will they replace physicians in some tasks? What does this mean for doctors, nurses, and the future of medicine?

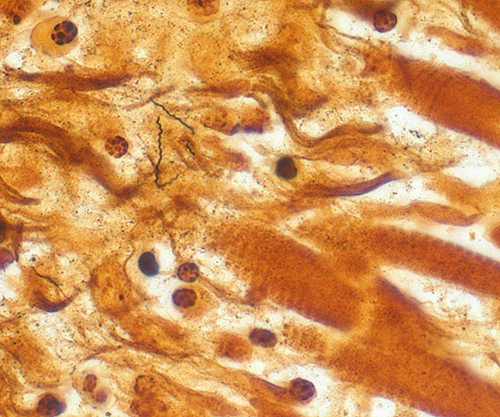

Borrelia

While AI technologies will go a long way to assist health care providers to provide better care, its application to medical care is still just beginning. One can anticipate, however, that in geographic areas where medical professionals are scarce, AI technologies will play an increasing role in improving patient care by allowing differential diagnoses to be generated and treatment options suggested through AI-based systems accessed through the internet.

The general public has more access to information than ever before about Lyme disease from websites, medical organizations, articles and social media. Everyone can be their own “expert” or even their own “doctor.” Can you speak about the pros and cons of online health data in the era of fake news?

This obviously is a huge area of concern. Individuals used to turn to their physician or to the medical information books, such as the Merck Manual. Now, they turn to the web.

In a recent survey of patients who used the web to obtain health information (Doherty-Torstrick 2016), we learned that more than half of the 730 patients reported they experienced increased distress as a result of checking the web. We also learned from this survey that individuals who did not have a health education were more likely to spend more time on the web and were thus prone to develop more anxiety than those who were better educated from a health perspective. While some of the information they find may be accurate, other information may be well-intentioned but ill-informed, misleading, and even harmful.

“Researchers can rapidly screen thousands of drugs to determine which agents have the strongest ability to kill Borrelia spirochetes. This is possible because of the development of high throughput assays, which have proven more effective than the standard agents in eradicating both the stationary phase Borrelia and its more drug-tolerant persister-forms.” — Brian Fallon

Look into the future. What are the technologies you are most excited about in terms of helping to find cures for Lyme disease and improve patients quality of life?

Researchers can rapidly screen thousands of drugs to determine which agents have the strongest ability to kill Borrelia spirochetes (Feng 2014). This is possible because of the development of high throughput assays, which have identified new antibiotics that have proven more effective than the standard agents (doxycycline, amoxicillin) in eradicating both the stationary phase Borrelia and its more drug-tolerant persister-forms. While it cannot be assumed that what is true in the lab setting will translate to efficacy in humans, biotechnology advances have enabled the identification of new therapeutic agents, offering much hope for a wider array of treatment options for patients in the future.

Another major advance is “big data” conducted by biomedical information engineers trained in biostatistics and computer science. Internet search engine queries are being monitored to predict outbreaks of infectious disease. Unanticipated side effects of drugs and their interactions can be detected through analyzing millions of digital medical records from patients who have taken a particular drug. One can examine whether patients given an antibiotic did better when treated for longer or shorter periods, or whether patients with a pre-existing autoimmune disease are more likely to develop complications from a new onset Tick-borne infection than those without a history of autoimmune problems.

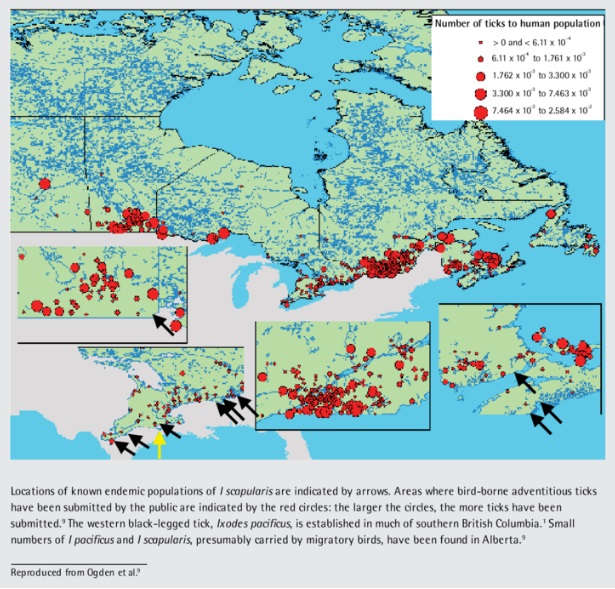

2005 James Gathany; William Nicholson The blacklegged ticks, I. pacificus, (depicted here), and I. scapularis, are known vectors for the zoonotic spirochetal bacteria Borrelia burgdorferi, which is the pathogenic bacteria responsible for causing Lyme disease. The ticks, inoculated with the bacterium when they bite infected mice, squirrels and other small animals, subsequently pass the pathogens to their human victims when they obtain a blood meal.B. burgdorferi bacteria can infect several parts of the body, producing different symptoms at different times. Not all patients with Lyme disease will have all symptoms, and many of the symptoms can occur with other diseases as well. If you believe you may have Lyme disease, it is important that you consult your health care provider for proper diagnosis. The first sign of infection is usually a circular rash called “erythema migrans”, or EM. This rash occurs in approximately 70-80% of infected persons and begins at the site of a tick bite after a delay of 3-30 days. A distinctive feature of the rash is that it gradually expands over a period of several days, reaching up to 12 inches (30 cm) across. The center of the rash may clear as it enlarges, resulting in a bull’s-eye appearance. It may be warm but is not usually painful. Some patients develop additional EM lesions in other areas of the body after several days. Patients also experience symptoms of fatigue, chills, fever, headache, and muscle and joint aches, and swollen lymph nodes. In some cases, these may be the only symptoms of infection.

Our Lyme and Tick-borne Diseases Research Center, located at the Columbia University Irving Medical Center (CUIMC) in New York City, is right next door to an international data resource. CUIMC is the coordinating center of a public health information initiative which includes medical records from approximately 400 million people drawn from eighty health-care organizations from around the world. This represents a unique opportunity to ask questions, generate hypotheses and get answers about Tick-borne diseases. When discovery is optimized, medical care is enhanced.

Brian Fallon, MD, MPH is the Director of the Lyme and Tick-Borne Diseases Research Center at the Columbia University Irving Medical Center and the author with Jennifer Sotsky of Conquering Lyme Disease: Science Bridges the Great Divide, published in 2018 by Columbia University Press.

Women of Architecture: a collective of unique voices

Throughout history, architecture has spoken — shaping society, holding memory, imagining the future. Yet too often, the female voice behind that speech has been softened, its echoes diminished. Women of Architecture: a collective of unique voices, a special edition of the New View series, seeks not to shout, but to speak — clearly, boldly, and with grace. This landmark volume honors twenty-five leading women architects whose work is as deeply intelligent as it is beautifully human. Their projects reveal not only where we live, but how we live — and why it matters.

Designed with museum-quality elegance and presented with curatorial care, the book invites readers into a gallery of real spaces that are not about grandeur or pretense, but purpose and poetry. With 12-page dedicated spreads, each architect’s story is captured in imagery and narrative that reflect the integrity of her vision.

This is not a collection of extravagance — it is a tribute to homes that breathe, spaces that embrace, and ideas that endure.

Beth Buckley is the Founder and Creative Director of benton buckley books ― an independent publishing house born from a lifelong love affair with beauty, culture, artistry, and the belief that extraordinary creative voices deserve to be seen widely, not selectively confined by inherited systems of exclusivity and cultural hierarchy.

With a career steeped in publishing, visual storytelling, curation, and cultural dialogue, Beth has become known for her rare instinct for authenticity, romantic sense of purpose, and ability to recognize meaningful creative work in a world increasingly shaped by repetition, algorithms, and manufactured relevance. Her work is guided less by trend than by instinct ― an instinct toward originality, emotional resonance, daring perspectives, and the artists whose work lingers long after the moment has passed.

Part publisher, part curator, part cultural provocateur, Beth founded benton buckley books in quiet rebellion against an industry that too often mistakes control for stewardship. She believes beautiful work should move through the world freely ― discussed, discovered, shared generously, and allowed to become part of a larger cultural conversation. The role of thoughtful publishing should not be to narrow the room. It should be to widen it.

Her philosophy is simple: the public deserves exposure not only to the familiar names endlessly repeated into relevance, but also to the extraordinary creatives still waiting to be discovered.

Over the years, Beth has collaborated with celebrated and emerging voices alike across architecture, interior design, travel, culinary arts, fashion, and visual culture ― always with the same conviction: the art comes first.

Like a curator assembling a living gallery of dreams, Beth approaches publishing not merely as production, but as preservation ― creating museum-quality books that invite beauty to linger well beyond the fleeting pace of modern media. She believes books are among the last truly permanent cultural objects we leave behind; vessels of imagination, dialogue, humanity, and memory.

And perhaps that is precisely why she continues making them. Smiling at the thought and enchanted by the notion that beauty (and a book) can outlive the moment.

In these pages, you will meet Lauren Adams, Amy Alper, Julia Arria, Maura Fernández Abernethy, Laura Juarez Baggett, Kristen Becker, Katherine Chia, Lise de Vito, Bibiana Dykema, Gale Goff, Laura Huylebroeck, Sussan Lari, Rebecca Lazenby, Annie Lo, Antonina Markoff, Marica McKeel, Kelly Murdock Solon, Joyce Owens, Anik Pearson, Julia Sanford, Mary Ann Gabriele Schicketanz, Ashley Sullivan, Andrea Swan, Michele Thackrah, and Nancy S. Weinman — women who, with every line and light-filled space, reveal a new vernacular of beauty. Women of Architecture shares the influences of the women featured in it — and the unique perspectives of women in architecture.

It has held champagne, breakfast cereal and even babies. It has been hoisted, hugged and almost kidnapped. It travels all over and has a team of chaperones to assure its safety.

It’s the Stanley Cup, the trophy awarded to the National Hockey League championship team each year.

This year, the Carolina Hurricanes, based in Raleigh, North Carolina, have won the coveted Cup, and the team is beginning a summer of passing the trophy from player to player. Unlike other national professional sports trophies, which are newly made and awarded to a new championship team to keep, there’s just one Stanley Cup. The champions in ice hockey only borrow the Stanley Cup for awhile, before it heads back to a vault in the Hockey Hall of Fame in Toronto.

Each Champion Player Spends A Day With The Cup- Sometimes With WIld Results

The players revere their brief turns to hold the Stanley Cup — the oldest trophy awarded to North American pro athletes. After the Cup was donated to Canada in 1892 by Sir Frederick Arthur Stanley, a British earl serving in Canada whose children loved ice hockey, the National Hockey League acquired it in 1910 to establish it as the award for League champions.

Florida Panthers Matthew Tkachuk poses in front of the Gateway Arch in St. Louis, Missouri, during his time with the Stanley Cup in 2025. (Courtesy of the Florida Panthers)

A sterling tradition

Today, each winning player has his name stamped on one of the five rings that make up the barrel of the Cup. When there is no more room for players’ names, a ring is removed and sent to storage, and another one replaces it.

No matter what mishaps or age-related stresses befall the silver-and-nickel trophy year after year, “they don’t create a new one,” says Hockey Hall of Fame official Kevin Shea, author of 21 books about hockey, including Travels with Stanley.

“It’s got its dents and scratches. It’s a real living thing,” Shea says.

If you watched the final playoff game in the championship, just after the final buzzer sounds, you would have seen Hurricanes players skating jubilantly around the rink, some carrying the massive and heavy — it’s 35 pounds (16 kilograms)! — Stanley Cup over their heads.

Soon the real fun begins.

A decades long tradition, which became official in 1995, dictates that each player and team staff member will get one day to have the Cup all to himself, celebrating in whatever way is special to him (without damaging the iconic trophy, of course).

In earlier years, the winners have come up with some sterling ways to make the most of their day with the Cup.

(State Dept./B. Insley)

The ‘Keeper of the Cup’

From one tradition grew another. Today, there is a “Keeper of the Cup” who, along with some deputies, keeps an eye on the trophy through all of this. They move with the trophy during a roughly 100-day period when players and staff members each have their day with it.

That all got started, according to the New York Rangers’ Neil Smith, when “one person took it, and the top came off. … And for some reason, somebody thought it would be wise to have an auto body guy weld it back on.”

Since then, the keeper of the Cup — Phil Pritchard, vice president of the Hockey Hall of Fame — accompanies it wherever it goes.

Pritchard and his helpers clean and polish the Stanley Cup at the end of each day before awarding it to the next player.

Players get it from 6 a.m. to midnight, with veteran players getting first dibs on the schedule. It’s a special honor, notes Shea of the Hockey Hall of Fame, since ice hockey players, out of superstition, won’t touch the Cup unless and until they win the championship.

How the Cup will enter the daily lives of 47 Hurricanes players and staff is yet to be seen. But it will connect them to champions from teams decades ago. That is what makes the tradition so inspiring, Smith says.

“Ice hockey teaches you things you can’t get anywhere else. … Great values of sharing, of being in a group,” Smith says. And the Stanley Cup, every summer, joins the group.

Yesterday, July 29, 2026, the United States designated the Persian Gulf Marine Insurance Company and Hormuz Safe Marine Services Authority, two Iranian entities backed by the Islamic Revolutionary Guard Corps (IRGC), for running coercive “insurance” schemes that extort international shipping transiting the Strait of Hormuz. These entities manufacture risk—including the threat of vessel seizures—and then charge commercial vessels for coverage against dangers created by the regime itself, generating revenue that sustains IRGC operations and Iran’s broader campaign of regional destabilization.

A Shadow Fleet

The United States also designated eight companies operating vessels that have transported illicit Iranian crude oil and petrochemical products to China and the United Arab Emirates. These vessels form part of Iran’s “shadow fleet,” which the regime relies on to evade sanctions.

Yesterday’s designations support the U.S. Navy’s enforcement of a blockade on Iranian ports and coastline and add to a sustained campaign that has now sanctioned more than 100 vessels this year.

The United States will continue to hold Iran accountable for weaponizing vital international waterways and evading sanctions through shadow fleet operations and deceptive financial schemes. Protecting navigational rights and freedoms in the Strait of Hormuz is a global interest, and the United States will act, alongside partners, to ensure Iran cannot hold international commerce hostage to finance its malign activities. We will continue working with allies to isolate the regime diplomatically and economically until it ceases its destabilizing behavior.

This most recent action was taken pursuant to Executive Order (E.O.) 13902, which targets Iran’s financial, petroleum, and petrochemical sectors. It continues the robust sanctions campaign targeting Iranian oil sales in support of the President’s National Security Presidential Memorandum 2 (NSPM-2). For more information on today’s action, please see the Department of the Treasury’s press release.

“According to a report from Bloomberg, recently released satellite images appear to show damage done to two Amazon data centers in Bahrain, which the Iranian Revolutionary Guard Corps (IRGC) previously claimed to have hit.” gizmodo.com

With satellite imagery now appearing to corroborate the recent strikes on Amazon’s Bahrain data centers, the question of how commercial data centers actually defend themselves has become live.

Amazon’s presence in Bahrain is registered under Amazon Data Services Bahrain S.P.C, located at Bahrain World Trade Center, Level 9, Building B0001, Isa Al-Kabeer Avenue (Road 365), Flat 938, Clock 316, Manama, Bahrain

Laurynas Šatas, CEO of Aktyvus Photonics, a defence technology company developing laser-based precision targeting systems for NATO tactical drone platforms. thinks data centers should defend themselves against drones, and partner with the state for missile defense.

A repeat of another attack

“A very similar attack on AWS data centers happened in March. But it’s worth separating the two events, because they involved different weapons. The confirmed March strikes used one-way attack drones. The July strikes on the Bahrain facilities appear to have involved missiles, and while Amazon hasn’t confirmed the extent of the damage, independent satellite imagery now appears to corroborate that it was significant.

“The March strikes marked a genuine shift. Commercial cloud facilities were never designed to sit inside a kinetic threat environment, and now they are being treated as legitimate military targets. That changes the security conversation for the whole industry.

The Bahrain World Trade Center (where the attacked Amazon data center is said to be housed) makes for a clearly visible and easily targeted object.

Transferable Model Of Defence

“It is important to be precise about the threat, though, because it is not one threat. Slow, low-flying, low-cost drones and high-speed missiles call for very different defences. Against the cheap and persistent drone threat, a layered counter-UAS approach – detect, track, then mitigate – is realistic and increasingly affordable. We already see this in Ukraine, where the private sector has taken on a real part of the air defence task against low-speed threats, using a mix of effectors. That model is transferable to critical civil infrastructure such as data centres.

“Faster-flying threats are a different problem. They require significantly more complex and far more expensive systems, which we cannot realistically expect a commercial operator to afford, or to be cleared and trained to operate. That part stays with state militaries.

“So the practical sequence for data centres is: defend yourself against drones first, and coordinate with the state for the missile threat. I expect this level of protection to become a standard part of how such sites are built and operated.”

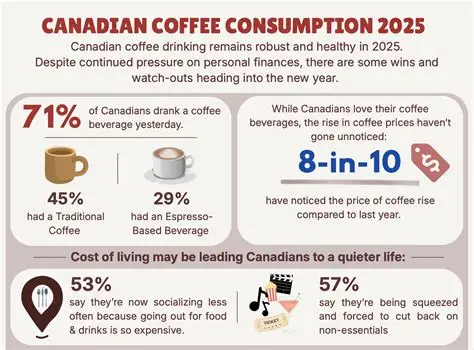

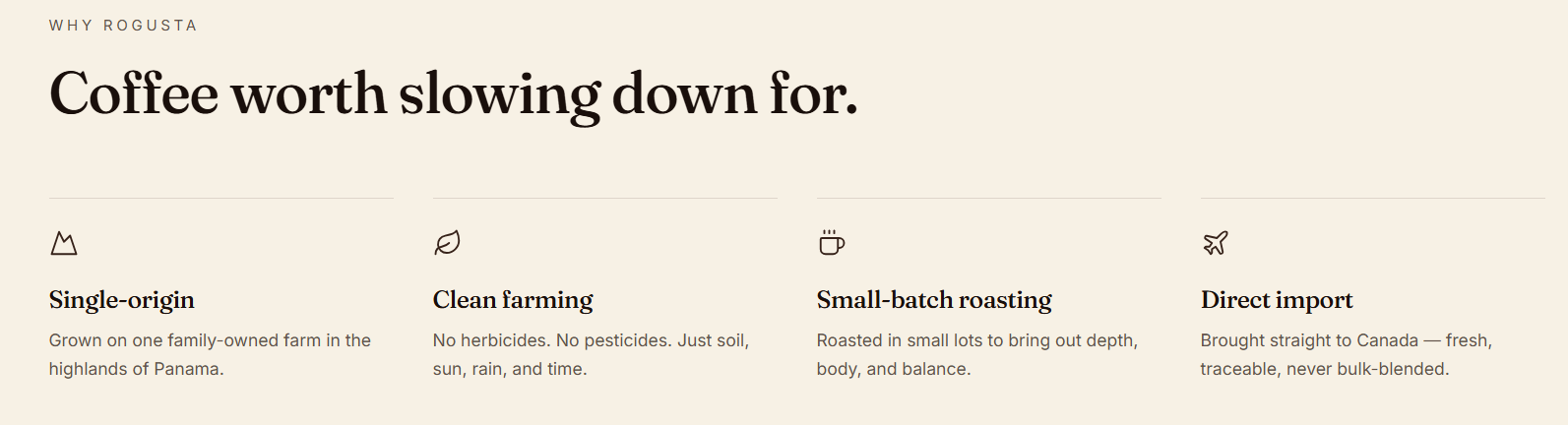

There is something special about enjoying a cup of coffee that can be traced back to the people and the place where it was grown.

At Rogusta Coffee Canada, our mission is simple: to bring exceptional Panamanian coffee directly to Canadian homes while creating a closer connection between coffee lovers and the farmers who produce it.

Our coffee is carefully sourced from Hacienda Rogusta and neighbouring family-owned farms in Penonomé, Coclé Province, Panama. Grown in fertile volcanic soil and harvested by hand at peak ripeness, every bean is selected with care to deliver outstanding quality and consistency.

Coffee consumption is on the rise in 2026 as well.

Air Shipped Means Freshness

Unlike coffee that may spend weeks travelling by sea, our beans are air-shipped to Canada to help preserve their freshness, aroma, and distinctive character. Once here, they are prepared for Canadian customers who appreciate quality, freshness, and traceability.

We currently offer both whole bean and ground coffee, allowing customers to enjoy the same premium Panamanian Robusta whether they brew espresso, pour-over, French press, or drip coffee at home.

Our signature medium roast is carefully developed to highlight the bean’s natural sweetness, smooth body, and rich flavour profile instead of masking it with an overly dark roast. The result is a bold yet remarkably smooth coffee with naturally higher caffeine and very low acidity.

Rogusta is also proud to represent coffee from the same producer whose coffee has been served onboard Copa Airlines, introducing thousands of travellers across the Americas to the taste of premium Panamanian coffee.

Exceptional and un-common Coffee for Canadians

As a Canadian importer, we are committed to building long-term relationships with responsible producers while giving Canadian consumers access to exceptional coffee that is difficult to find in traditional retail channels.

Our first shipment to Canada is arriving soon, and pre-orders are now open.

Whether you’re a coffee enthusiast, café owner, retailer, or simply someone looking to discover something different, you are warmly invited you to experience premium Panamanian coffee—fresh from the source.

Developer to the stars, Ramtin “Ray” Nosrati, was born in Iran and moved to the United States as a child. Attributing his talents for home building and design, he credits his parents’ Sunday drives exploring Los Angeles area open houses and his childhood LEGO collection for sparking his early interest in the business.

Ray began his career in the cell phone business, a success that he sold in 2002, using the profits to jump into real estate.

Beginning with some chicken ranches, he used the land to build tract homes for middle-class buyers. Following his dream, he then began buying tear-downs in the Los Angeles area to build more expensive custom homes. Ray parlayed that success to the top of the home-building business and became the go-to builder for celebrities and rich clients in LA’s most upscale neighborhoods.

Ray’s signature style blends traditional elegance with sleek contemporary lines, creating homes that feel both timeless and modern.

His projects emphasize seamless indoor-outdoor living, innovative amenities, and dramatic “wow” moments while remaining comfortable and family-oriented. His stunning homes command record prices, take home prestigious awards, and attract celebrity clients across the globe, frequently selling before completion. He has built and sold over 100 homes, including his trophy estate, Brentwood Oasis, which he sold to DBL Partners founder Jeffrey Feinberg for $44 million usd, while his latest home, a Beverly Hills mansion, sold to Fashion Nova CEO Richard Saghian for $32 million usd.

Ray’s newest showpiece home is Opal, a spectacular Beverly Hills chateau, listed for $53 million usd/ $74.8 million cad. Opal combines contemporary architecture with resort-style amenities across multiple levels. The palatial home spans 19,100 square feet and includes custom European furnishings.

Opal’s interiors feature expansive glass walls with gorgeous views of downtown LA and the Pacific Ocean, a double-height foyer, a two-story dining room with skylights, and a travertine-clad kitchen with custom appliances, an oversized island, and a separate catering kitchen with a commercial-grade walk-in refrigerator. A glass elevator connects all four floors.

The primary suite includes a private terrace, an espresso bar, a sauna, a spa-style bath, and one of the largest residential dressing rooms ever permitted in Los Angeles. Entertainment spaces occupy the lower level, where amenities include a temperature-controlled wine-tasting room, a theater with a snack bar and celestial ceiling, billiards and card areas, a wellness gym, reading lounges, and a media room with a nine-screen video wall.

Outdoor features include two infinity pools, one incorporating a glass-bottom design with Baja shelves, multiple terraces, and a rooftop deck with panoramic views of the city, mountains, and ocean. The rooftop also includes a pickleball court, outdoor dining areas, and fire tables. A barbecue pavilion on the main level is equipped with a pizza oven, wet bar, serving counter, and a 116-inch television. Set behind a gated entrance and surrounded by mature olive trees, palms, and ficus hedges, the property includes a motor court accommodating up to 12 vehicles and an eight-car garage.

Beverly Hills remains one of the world’s most recognizable luxury enclaves, known for its palm-lined streets, grand estates, and concentration of high-end shopping, dining, and entertainment. Located between West Hollywood and LA’s Westside, the city is home to iconic destinations including Rodeo Drive, the Beverly Hills Hotel, and numerous acclaimed restaurants and private clubs. Despite its international reputation, Beverly Hills maintains a largely residential character, with quiet neighborhoods tucked behind manicured hedges and winding streets. Its proximity to major studios, business centers, and the beaches of Santa Monica has long made it a preferred address for entertainers, executives, entrepreneurs, and public figures. The city has been associated with Hollywood glamour for decades and continues to attract prominent residents from film, music, television and sports. Notable Beverly Hills residents include Adele, Jennifer Aniston, Sylvester Stallone, and Justin Bieber.

For the Silo, Kimberly Ridley.

The listing is held by Sally Forster Jones of Compass, Tomer Fridman of Christie’s International Real Estate Southern California, and Jonathan Nash of Carolwood.

Photo Credit: Andrew Bramasco and Clutch Visuals MediaSource:www.compass.com

If things go all Minority Report, you’ll need a jacket that keeps you incredibly warm while simultaneously reducing your thermal signature from the drone swarms. The good news is our friends at Vollebak have made a jacket that does exactly that. The bad news is that they’re down to the last few.

The first layer of the jacket is the outer layer, and it’s the one that does the thermal and electromagnetic cloaking.It’s built with an advanced version of the metallic insulation originally developed by NASA to stop their spacecraft freezing in space… which means it does some really unusual things.

They only metallise the surface of the jacket – by submerging it in a bath of metal salts with current running through it, so metal ions plate themselves onto every fibre atom by atom….And this means that the jacket still moves and breathes like cloth – not metal – so it’s perfect for evasion.

The metallised surface also has very low emissivity, bounces back the IR radiation from your body, emits very little heat, acts like a Faraday cage, and makes you appear cold or even invisible to infrared cameras. The second layer of the jacket is the inner layer. And this is the ‘keeping you warm’ bit.It’s a precision-cut and detachable winter liner inspired by the modular cold-weather systems first engineered for U.S. Army fishtail parkas. The M-48, M-51 and M-65 were all built around the same idea – a lightweight shell and a highly insulated inner jacket that could be buttoned in, removed, repaired, or worn on its own.

The Thermal Cloaking Jacket – pictured here at the launch of the Vollebak Spaceshop – updates that idea with a far more engineered, elegant and flexible system.

It’s a modular attachment system designed to lock the two layers together so they behave like a single cold-weather machine.A string of loop tabs along the front of the liner fasten over internal buttons on the shell. Two dedicated buttons at the back of the neck anchor the top of the liner, and snap tabs at the cuffs connect the two sleeves.

Once docked, the shell and liner move as one piece.Undock it, and the liner operates as a fully independent jacket. So when Minority Report becomes reality – which clearly it’s going to – you can telepathically send them your thank you messages. The jacket comes in two colours: Metal and Rust.

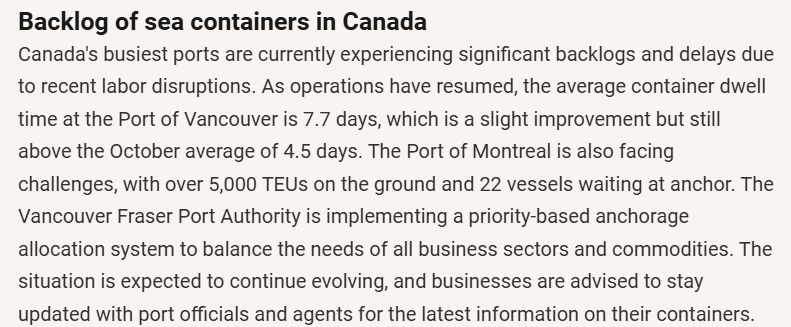

Trade Diversification Ambitions Face a Container Port Reality

Alberta recently submitted its West Coast pipeline proposal to Ottawa’s Major Projects Office, a major plank in the federal government’s goal to double exports to non-US markets by 2035.

For that to succeed, more of Canada’s exports will need to move by water, already the largest mode for non-U.S. trade by value. And container shipping is part of that.

So how do Canada’s container ports stack up?

The short answer: Not well. Rectifying that would help Canada meet its trade-diversification goals.

Roads were Canada’s dominant export mode over the 12 months ending in May, carrying 37 percent of export value. But those roads cross just one border. Strip out the United States and the picture flips entirely. Water carries 54 percent; air carries 41 percent. Road falls to 3 percent. Put differently, the infrastructure we’ll need to reach the 2035 target looks almost nothing like today’s.

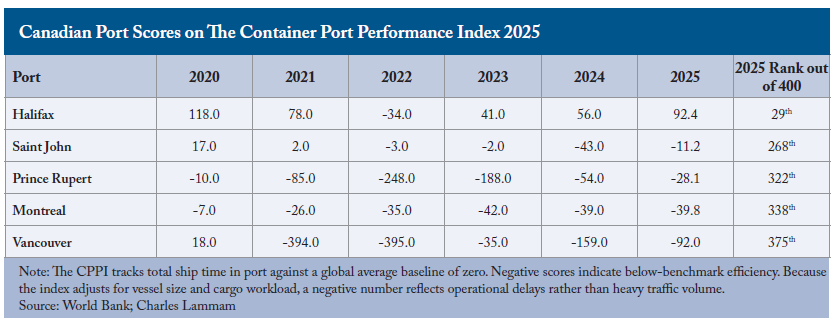

What is the Container Port Performance Index?

The Container Port Performance Index (CPPI), produced by the World Bank, is a global scorecard for container shipping efficiency. Canada’s performance should raise alarm bells.

The Index tracks total time a container ship spends under a port’s control, from the moment it arrives in the harbour to the moment it leaves the berth. Rather than grading ports on a traditional scale of zero to 100, the index uses a statistical baseline centred on the global average and adjusts for the size of a vessel and its cargo volume. A negative score means a port is operating below that benchmark. It simply means that for the same job, a ship sits idle longer than at an average gateway anywhere else.

The Port of Vancouver, which handles fully 42 percent of Canada’s container shipments, ranks 375th out of 400 ports worldwide in the newly released 2025 ranking, with a score of minus 92. That’s actually an improvement on minus 159 in 2024: a dismal 389th. Vancouver was among the 20 most-improved ports in the world year over year. But even after climbing 67 points, a hole this deep still leaves you in the hole.

Vancouver’s CPPI score has been negative in five of the last six years, including a catastrophic collapse to minus 394 and 395 scores in 2021 and 2022, which also coincided with a historic BC flood that severed rail lines into the port for more than a week, layered on top of a pandemic-era demand surge hitting ports worldwide. Even so, strip those two years out and Vancouver’s score still never turns positive again.

Vancouver is part of a broader Canadian pattern. Prince Rupert ranks 322nd, despite handling a meaningful share of Canada’s transpacific container trade, and its year-to-year swings are significant: from minus 10 in 2020 to minus 248 in 2022 to minus 54 in 2024. Montreal sits at 338th. Saint John is slightly better at 268th.

The one major exception is Halifax, which has become a genuine success story: 29th in the world in the latest data, up from a middling performance just a few years ago, and 55th last year. Three of Canada’s busiest ports still rank in the bottom fifth of the world. Halifax proved it doesn’t have to be that way.

A recent Bank of Canada analysis of satellite vessel-tracking data found that Canada’s rank for total ship capacity moving through its ports fell from sixth in the world in 2016 to 23rd by 2023, a steeper drop than almost any other major trading nation. Part of the reason: the newest ultra-large container ships carry more than 20,000 containers while the largest vessels Canadian ports can handle top out around 15,000. As a result, some cargo bound for Canada comes through a US port.

Infrastructure isn’t the whole story. Labour issues also lengthen the time ships spend in Canadian ports, and addressing them matters just as much as modernizing the infrastructure itself.

After Nutrien decided to build its new billion-dollar potash export terminal in the United States rather than in Canada, Transport Minister Steven MacKinnon, made an unusually blunt admission for a sitting minister about his own file: Canada’s transportation policy and supply chain management need to be the best in the world given the country’s geography, and right now they aren’t.

Nutrien’s decision came even after the 2025 federal budget had already been tabled. That budget dedicated $5 billion, or 4 percent, of its $115-billion infrastructure plan to bolster Canada’s trade and transport infrastructure. Whether allocating more to such infrastructure would generate a bigger bang for the buck is a fair question.

Carney’s Ambitions

The PM’s ambitions depend on a clear-eyed read of where Canada’s port performance actually stands. The pattern holds across almost every major Canadian port, year after year, even as Ottawa doubles down on trade diversification. Halifax shows that the climb from a lower tier is possible. Until the rest of Canada’s ports make it too, the 2035 target will likely stay out of reach.

Watch the shark advocacy documentary, Monsters. The director, Skyler Thomas, is a featured speaker in IDA’s Sharks & Aquatic Animal Activism Webinar

SAN RAFAEL, Calif. (July, 2026) — Oceanic shark populations have collapsed by more than 70% over the past 50 years, driven largely by commercial and recreational fishing, according to research published in Nature. In Defense of Animals is urging supporters to help defeat the SHARKED Act, a bill that would weaken vital U.S. shark protections, and to demand an end to deadly shark nets.

The push comes as In Defense of Animals marks its annual Respect for Fish Day, observed August 1, with a free public webinar on Thursday, July 30 at 2 p.m. PT. Featured speakers include shark experts such as Skyler Thomas, director of the shark documentary Monsters.

In Defense of Sharks — Sharks & Aquatic Animal Activism

“Sharks are feeling, highly intelligent animals who experience pleasure, pain, and suffering,” said Lia Wilbourn, Farmed Animals Campaign Specialist at In Defense of Animals. “They are often wrongly portrayed as monstrous man-eaters, largely the result of fear-driven media and industries that profit from killing them. In reality, most shark species pose little or no danger to humans and are far more at risk from human activity than humans are from them.”

The webinar will dispel harmful myths about sharks and explain why protecting them is essential to their survival and to the health of the oceans. It comes at a critical moment: In Defense of Animals is calling on the public to oppose the SHARKED Act and to speak out against shark nets planned or already in use at beaches in Australia and at a Club Med resort in South Africa, where the nets indiscriminately kill sharks and countless other marine animals alongside their intended targets.

Skyler Thomas, director of the feature film documentary, Monsters, said, “Sharks aren’t just cool, they are massively misunderstood and underestimated by humans — not just physically, but as sentient beings. Today I realize that sharks share this in common with all other species on the planet: humans don’t give them enough credit.”

Scientific research shows that fish and other aquatic animals are far more intelligent and emotionally complex than most people assume. They can recognize individual faces, remember previous experiences, form social connections, and maintain long-term relationships. Like all sentient beings, fish have nervous systems and feel pain, fear, stress, and suffering when they are hooked, netted, suffocated, or stabbed during fishing.

The fishing industry is one of the greatest threats to ocean life and biodiversity. Fishing pollutes the seas and disrupts fragile marine ecosystems. Millions of whales, dolphins, seals, sea turtles, octopuses, and other non-target animals are killed each year as “bycatch” in commercial fishing nets, and abandoned fishing gear is now the largest source of plastic pollution in the ocean.

Fish also accumulate harmful contaminants, including mercury and arsenic, yet for most of us, fishing isn’t necessary for survival; leading nutrition experts agree a balanced plant-based diet meets all essential nutritional needs.

Marine wildlife populations have fallen dramatically over the past few decades, and scientists warn that continuing current fishing practices could have devastating consequences for ocean ecosystems.

Respect for Fish Day emphasizes the individuality, sentience, and complexity of aquatic animals, advocates for veganism, and builds a future where all animals are free from exploitation and unnecessary harm.

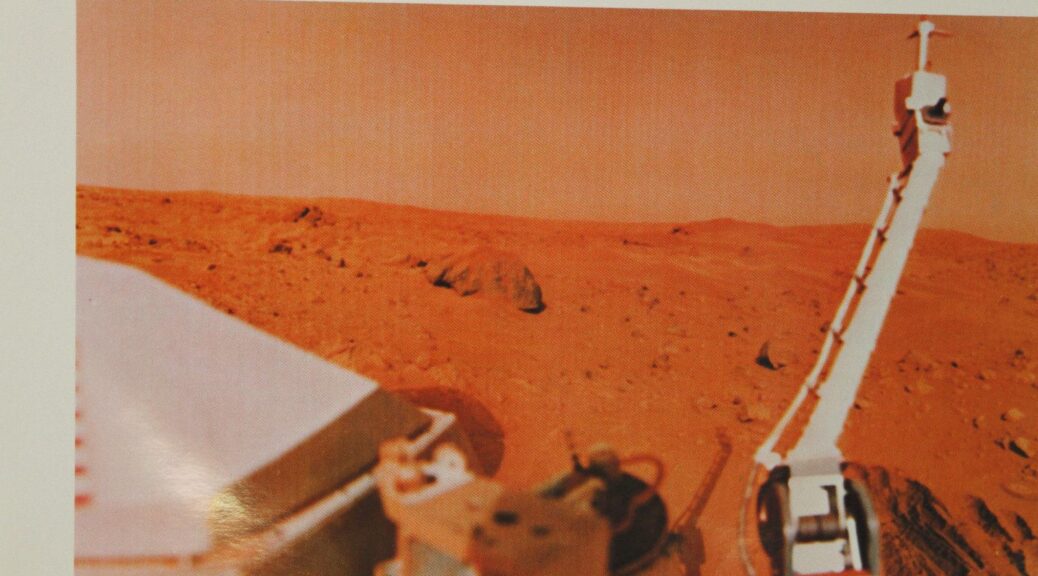

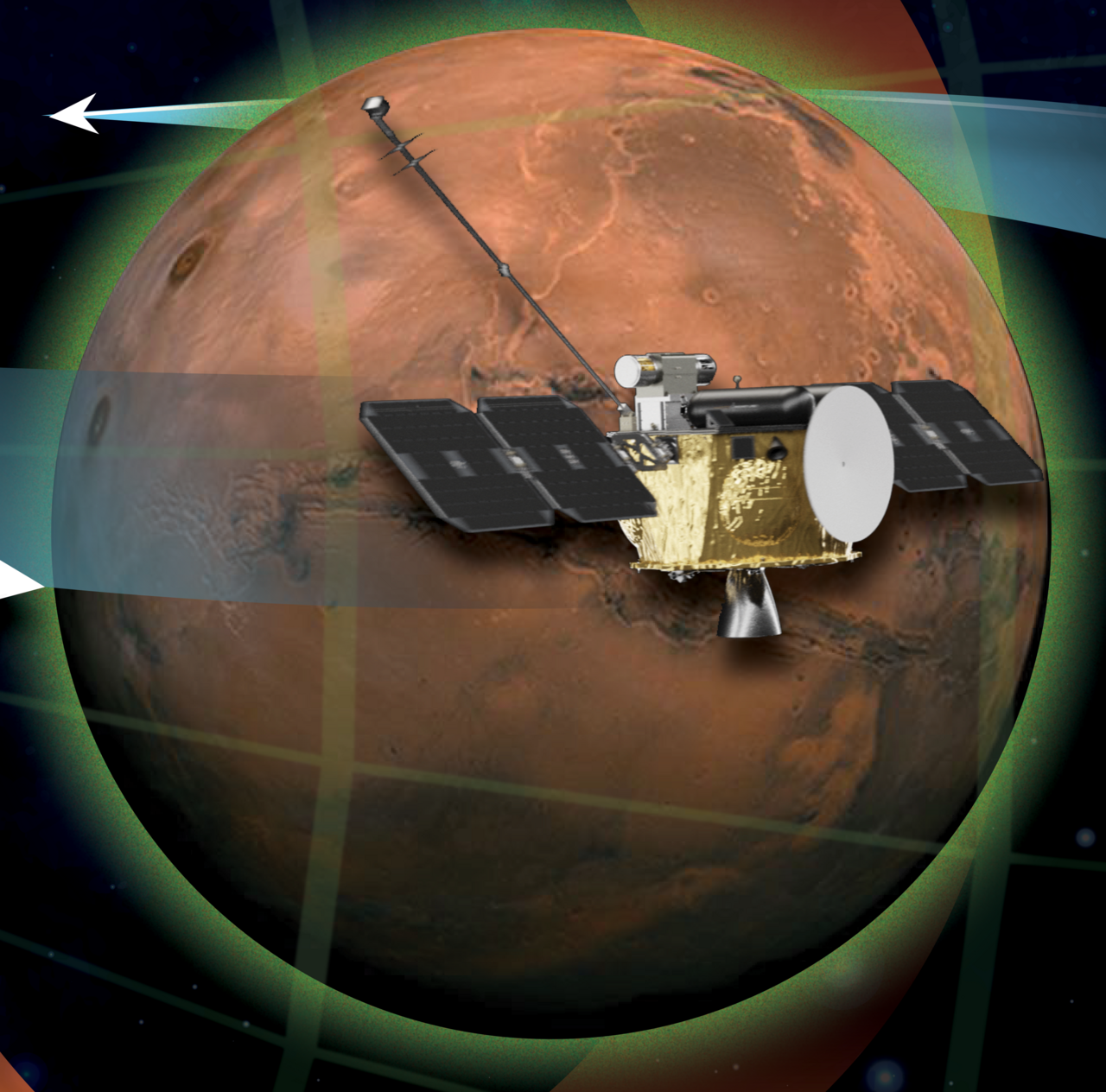

The Viking 1 lander’s photographs gave the world its first look at the surface of Mars, including this image taken before sunset August 21, 1976. (NASA/JPL)

On July 20, 1976, seven years after NASA landed a man on the moon, the U.S. space agency safely landed the first spacecraft on Mars.

Viking 1 operated for six years, far exceeding its planned 90-day mission. The lander tested soil and sent home the world’s first images of the Martian surface. While Viking 1 — consisting of an orbiter and a lander — did not find signs of life, its successful landing led to future exploration of Mars, including by the Perseverance rover launched in July 2020.

As the 50th anniversary of Viking 1 approaches, the United States is again reaching for Mars with missions that serve as a stepping stone toward sending astronauts to the red planet. NASA’s Artemis program aims to create a permanent moon base by 2032 to test human habitation on other planets and inform missions to Mars.

“We will pursue our manifest destiny into the stars, launching American astronauts to plant the Stars and Stripes on the planet Mars,” President Trump said in his January 2025 inaugural address.

Mars missions continue

This digital rendering provides a conceptual image of the Space Reactor 1 Freedom that NASA will use to study Mars. (NASA)

Other NASA missions are carrying on Viking 1’s legacy , furthering scientific knowledge of the fourth planet from the sun. Launched in November, NASA’s Escapade and Plasma Acceleration and Dynamics Explorers mission will reach Mars in 2027. The twin spacecraft will orbit Mars, collecting data on space-weather conditions to inform future robot and human missions.

In 2028, NASA will launch the Space Reactor‑1 Freedom to Mars, an uncrewed mission designed to demonstrate whether nuclear electric propulsion can work in deep space, an essential element for human flight to Mars.

A pioneering legacy

A Viking 2 image of Mars’ Utopia Plain (NASA)

Successfully landing Viking 1 on Mars was an extraordinary achievement. While other nations had tried, communications were lost on touchdown. Yet NASA repeated the feat two months later with the safe landing of Viking 2 on September 3, 1976.

Project managers weren’t certain what to expect from either mission. The Viking 1 landing, originally scheduled for America’s bicentennial on July 4, 1976, was delayed when the planned landing site appeared too rocky. Yet the Viking missions’ legacy endures. Viking orbiters mapped 97% of Mars’ surface and sent home 52,663 images. The landers returned 4,500 photos before Viking 1 finally stopped operating in November 1982.

While neither mission discovered signs of life, the search continues as scientists revisit findings from Viking and later missions. In September, NASA announced that a soil sample Perseverance collected may contain evidence of ancient microbial life, calling it “the closest we have ever come to discovering life on Mars.”

This post is a response to the comic book article found at popuniverse which begins like this:

“The comic book industry is the launchpad for one of the most unique and innovative storytelling mediums ever created. Powered by imaginative creators highly skilled in the written and visual arts. Forged by businesspersons who recognize the power of ideas to make an iconic impression on a global scale. Propelled by readers and fans who support the industry and the people who make the stories. The comic book industry is the source of multimedia interpretations of mythic and personal stories that inspire people, entertain the world, and ignite lifelong careers.

It is the adventure of a lifetime.

The comic book industry is a ruthless Darwinian landscape of cronyism, narcissism, and power moves. Its main fodder is the creators who are the engines of its continued existence. Full of flair and pomp, colors and characters both fictional and real-life. A road to hell paved with landmines, bear traps, and the opportunity to work on high-profile, profitable media while living on the precipice of poverty. The industry is fueled by organizations with finite funds and infinite hubris.“

“The comics industry is the illusory world of grenades disguised as dreams.“

The issue I see (and our comic illustrator household has personally experienced) in the comics and illustration / publishing industry is that the original contract terms were never set up fairly to compensate the artists and illustrators. While photographers and videographers retain the rights to their original images, and someone must pay them usage rights fees based on the size of the audience per usage, the artists are never granted that same fair compensation.

While actors get residuals when their TV shows play on in perpetuity, and musicians earn their royalty checks with every needle drop, the comics publishers can repurpose an illustrator’s iconic cover art in perpetuity and make millions from the image—on puzzles, lunch boxes, hoodies, sweatpants, and pajamas in my husband’s particular case—while the artist never sees a dime beyond the initial ANEMIC work-for-hire fee in these insanely unfair, one-sided deals. And if the artist DARES to complain? The smear merchants are only too happy to start their whisper campaigns, blackballing the artist as “too difficult to work with” and completely destroying their already financially challenged lives with nuisance law suits.

When I think back on how Ghost Rider co-creator Gary Friedrich was made the industry scarecrow in the last years of his life as greedy lawyers descended upon him like buzzards picking the last flecks of flesh from his bones, it sickens me.

This impoverished, unwell, elderly man was just trying to eke out the last days of his hard-scrabble life by selling sketches of his OWN co-creation at comic-cons. There’s nothing I despise more than anyone preying on the vulnerable. It’s appalling how Gary was treated.

And then we have AI “art” apps exploiting my husband’s already way underpaid art to create new, derivative works, but only GETTY Images can afford to lawyer up and go after these apps…because the photography world always negotiated image usage the CORRECT and fair way from the start.

The sobering truth is that if illustrators (and line artists, colorists, and letterers) were paid as well as photographers, every comic would sell for $100 per floppy and that would be the final nail in the #comics industry’s coffin.

…DAVE DORMAN… told me at dinner tonight that someone was selling AI art at SDCC last week and was summarily kicked out of Artists Alley. It gave me a brief glimmer of hope…I imagined a deafening crescendo of cheering as the non-talent skulked away, tail between his/her legs. That takes some gall to occupy the highly competitive table space of an ACTUAL hard-working artist (who’s paying off about $100k in art school student loans) with some Mid-Journey derivative crap. Wowzers. For the Silo, Denise Dorman.

Major Exhibition Dedicated to the Careers of Lee Krasner and Jackson Pollock Featuring over 120 works from more than 80 U.S. and international lenders, this exhibition marks the first major New York presentation of either artist’s work in over two decades—and their first at The Met.

Exhibition Dates: October 4, 2026–January 31, 2027 Exhibition Location: The Met Fifth Avenue

(New York, July , 2026)—Krasner and Pollock: Past Continuous at The Metropolitan Museum of Art is a major exhibition that charts the full arc of the careers of Lee Krasner (1908–1984) and Jackson Pollock (1912–1956) in parallel, examining the distinct yet connected practices of these artistic peers and life partners. On view October 4, 2026, through January 31, 2027, it marks the first major New York presentation devoted to either artist in more than 20 years, introducing their work to a new generation while reassessing their enduring impacts on modern and contemporary art.

Krasner and Pollock were emerging artists in New York when they met on the occasion of being included in a 1942 exhibition organized by the artist John Graham. They married in 1945 and moved to Springs, Long Island, where they remained entwined personally, artistically, and professionally until Pollock’s death in 1956. Pollock’s life’s work had secured his legacy, while the nearly three decades that Krasner survived him marked some of the most transformative years of her career. Drawing its subtitle, Past Continuous, from a 1976 painting by Krasner, the exhibition traces parallel lives and practices, first forged by lived experience and then shadowed by memory. It foregrounds the range and art historical significance of Krasner’s work while offering a sustained examination of Pollock’s rich and complex practice.

The exhibition is made possible by Kenneth C. Griffin and Griffin Catalyst, Marina Kellen French, and the Barrie A. and Deedee Wigmore Foundation.

Additional support is provided by Trevor and Alexis Traina, the Aaron I. Fleischman and Lin Lougheed Fund, The Huo Family Foundation, Joyce Kwok, Janice Lee and Joseph Bae, Dina Axelrad Perry, Alice and Tom Tisch, and the Horace W. Goldsmith Foundation.

“With its distinctive premise and scope, Krasner and Pollock: Past Continuous exemplifies The Met’s commitment to reexamining modern art through rigorous scholarship and fresh perspectives,” said Max Hollein, Marina Kellen French Director and Chief Executive Officer of The Metropolitan Museum of Art. “By considering each artist on their own terms while also foregrounding their consequential relationship, the exhibition situates Krasner’s and Pollock’s work within a broader cultural and artistic context—an approach central to the mission of The Met’s Department of Modern and Contemporary Art and to the vision of the forthcoming Oscar L. Tang and H.M. Agnes Hsu-Tang Wing, opening in 2030. This project affirms Krasner and Pollock not only as defining figures of their moment, but as artists whose work continues to shape and inspire future generations.”

“Krasner and Pollock: Past Continuous begins with the fundamental premise that these artists are equals, partners in life, giants in the history of art, and revolutionaries who defined what abstraction could be,” said David Breslin, Leonard A. Lauder Curator in Charge, Department of Modern and Contemporary Art, The Met. “Each found a partner who would insist on the primacy of art over life; and they both aspired to an art that was forged out of historical connections but that also promised freedom and radical possibility in a world forever changed by war. The exhibition concerns entwined lives but is also about how different artistic directions come from shared terrain.”